Legal Utah Promissory Note Form

Legal Utah Promissory Note Form

In Utah, individuals and businesses often turn to promissory notes as a formal agreement to detail the repayment of a loan. This binding document serves to protect the interests of both the lender and the borrower by clearly outlining the loan amount, interest rate, repayment schedule, and what happens if the borrower fails to repay the loan. The use of a Utah Promissory Note form is crucial in these situations as it provides a legal framework that ensures the agreement is enforceable under state laws. It highlights the necessity of adhering to the specific regulations and statutes of Utah to avoid potential legal disputes. Whether the loan is between friends, family members, or involves a more formal relationship between a borrower and a financial institution, the promissory note stands as a testament to the terms agreed upon by the involved parties. Its comprehensive nature allows for a smoother transaction process, preventing misunderstandings and defining clear expectations for repayment, which is essential for maintaining positive relationships and financial stability.

Utah Promissory Note

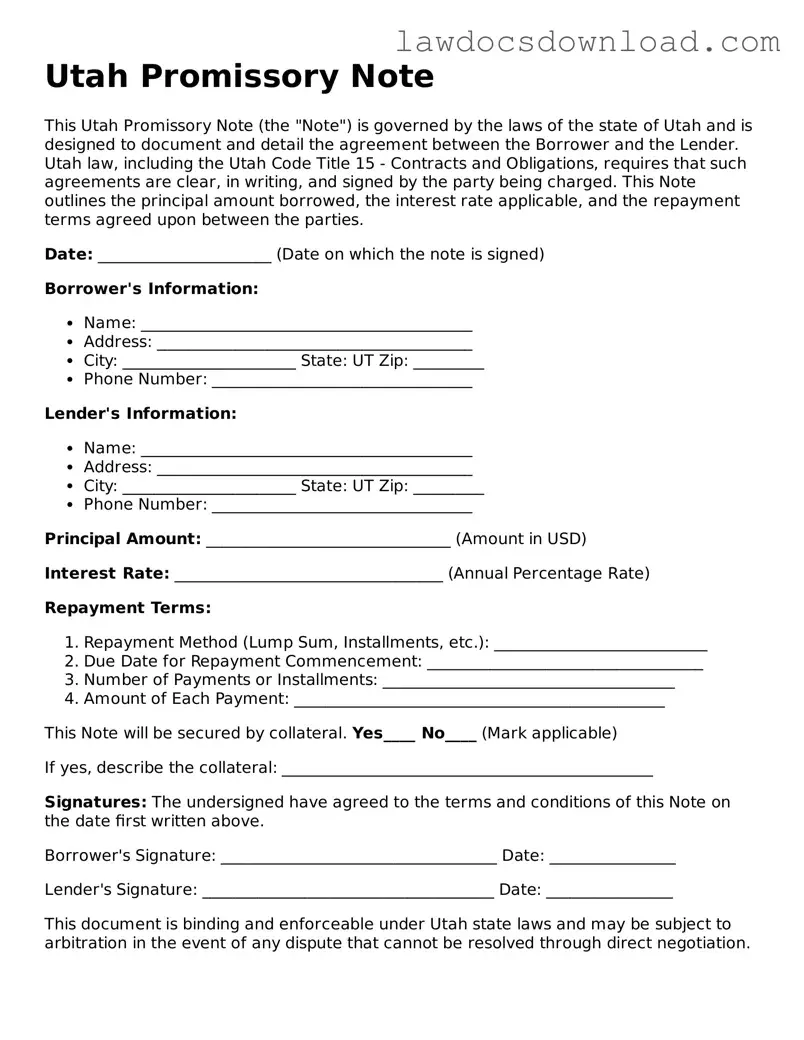

This Utah Promissory Note (the "Note") is governed by the laws of the state of Utah and is designed to document and detail the agreement between the Borrower and the Lender. Utah law, including the Utah Code Title 15 - Contracts and Obligations, requires that such agreements are clear, in writing, and signed by the party being charged. This Note outlines the principal amount borrowed, the interest rate applicable, and the repayment terms agreed upon between the parties.

Date: ______________________ (Date on which the note is signed)

Borrower's Information:

Lender's Information:

Principal Amount: _______________________________ (Amount in USD)

Interest Rate: __________________________________ (Annual Percentage Rate)

Repayment Terms:

This Note will be secured by collateral. Yes____ No____ (Mark applicable)

If yes, describe the collateral: _______________________________________________

Signatures: The undersigned have agreed to the terms and conditions of this Note on the date first written above.

Borrower's Signature: ___________________________________ Date: ________________

Lender's Signature: _____________________________________ Date: ________________

This document is binding and enforceable under Utah state laws and may be subject to arbitration in the event of any dispute that cannot be resolved through direct negotiation.

| Fact Number | Detail |

|---|---|

| 1 | The Utah Promissory Note form is a legal document used for the agreement of a loan repayment between two parties. |

| 2 | It can be secured or unsecured, with a secured note requiring collateral to guarantee the loan. |

| 3 | Interest rates on these notes must comply with Utah's legal limits. |

| 4 | The Utah Code Title 15 governs promissory notes within the state. |

| 5 | For a promissory note to be valid in Utah, it must include the amount borrowed, interest rate, repayment schedule, and signatures of both the borrower and lender. |

| 6 | Upon default, Utah law allows lenders certain rights, which may include taking possession of the collateral in secured loans. |

| 7 | Electronic signatures are considered valid for promissory notes in Utah as per the Uniform Electronic Transactions Act. |

| 8 | A promissory note can be transferred to another party unless expressly prohibited by its terms. |

| 9 | Failure to follow the specific legal requirements for promissory notes in Utah can result in the note being declared invalid or unenforceable. |

Completing a promissory note in Utah is a straightforward process, positioning both the borrower and lender clearly in regard to the repayment terms of a loan. This document serves as a binding agreement, ensuring the borrower agrees to pay back the borrowed amount under defined conditions. The steps to fill it out include providing detailed information about the loan, borrower, lender, and the repayment plan. By following these steps carefully, parties can ensure clarity and accountability throughout the duration of the loan.

Following these steps helps in creating a legally binding and clear promissory note. It’s essential for both parties to review the document carefully before signing it to ensure that all the information is accurate and understood by everyone involved. Keeping a copy of the signed document is important for future reference and helps protect the interests of both the lender and borrower.

What is a Utah Promissory Note?

A Utah Promissory Note is a legal document used for the purpose of recording a loan transaction between two parties in Utah. It outlines the amount of money borrowed, the interest rate, repayment schedule, and the obligations of both the borrower and the lender. This document serves as a formal agreement to ensure repayment under the terms specified.

Who should use a Promissory Note in Utah?

Individuals or entities in Utah involved in loan transactions should use a Promissory Note. It applies to both personal and business loans. Whether lending or borrowing money, having this document helps define the terms and conditions of the loan, making the agreement clear and legally binding.

Is a Promissory Note legally binding in Utah?

Yes, in Utah, a Promissory Note is considered a legally binding agreement once it is signed by both the borrower and the lender. It should meet Utah's legal requirements, including consideration (value being exchanged), mutual consent, competent parties, and a legal purpose. In the event of a dispute, the document can be used in court to enforce the loan terms.

What are the essential elements of a Promissory Note?

Do I need a lawyer to create a Promissory Note in Utah?

While it is not a legal requirement to have a lawyer to create a Promissory Note in Utah, it is highly recommended to consult with one. A lawyer can ensure that all the terms of the note comply with local laws and are in the best interest of both parties. Legal advice can prevent future disputes and misunderstandings.

Can a Promissory Note include collateral in Utah?

Yes, parties can agree to secure a Promissory Note with collateral in Utah. This means that if the borrower fails to repay the loan, the lender has the right to seize the collateral as repayment. Including collateral should be clearly stated in the note, including a description of the collateral.

What happens if a Promissory Note is not repaid in Utah?

If a Promissory Note is not repaid according to the agreed terms, the lender has the right to seek legal action to enforce repayment in Utah. The lender may also be able to take possession of any collateral if the note is secured. The specific course of action depends on the termsoutlined in the note and relevant Utah laws.

How can a Promissory Note be enforced in Utah?

To enforce a Promissory Note in Utah, the lender may need to file a lawsuit against the borrower for breach of contract. It's essential to have documented evidence of the loan, the terms of repayment, and any communication stating the borrower's failure to meet the terms. A court can then order repayment, possibly including legal costs and interest.

Does a Promissory Note need to be notarized in Utah?

While notarization is not a requirement for a Promissory Note to be legally binding in Utah, it is advisable. Notarization can add a layer of verification, confirming the identities of the parties involved and possibly preventing disputes over authenticity in the future.

Can the terms of a Promissory Note be modified?

Yes, the terms of a Promissory Note can be modified, but any changes must be agreed upon by both the borrower and the lender. It's best to document any amendments in writing and, ideally, to have the modifications signed or initialed by both parties. This ensures that the changes are recognized and enforceable.

Filling out a Utah Promissory Note form involves detailed attention to avoid common errors that can potentially complicate or invalidate the agreement. One common mistake is overlooking the requirement to clearly identify both the borrower and the lender including their full names, addresses, and contact information. This kind of incomplete information can lead to confusion and difficulties in enforcing the note if disputes arise.

Another frequent error is failing to specify the loan amount in clear, unambiguous terms. It's crucial to state the principal amount being loaned in numerals and words to prevent any misunderstanding. Without this clarity, the enforceability of the promissory note could be jeopardized, making it harder for the lender to claim the owed amount.

Not specifying the interest rate is a critical oversight that many make when filling out a promissory note in Utah. State laws can vary greatly regarding allowable interest rates and usury limits. Neglecting to include this information or setting an illegal rate can render the entire agreement void or subject it to legal scrutiny. Additionally, clear terms on how and when the interest is calculated should be provided to avoid any future disputes.

Terms of repayment are often inadequately detailed, which is another significant error. A comprehensive promissory note should include the schedule for repayment, whether in lump sum, installments, or on demand, and specify due dates or conditions that trigger payment obligations. Without a clear repayment schedule, managing and enforcing the terms of the note becomes challenging.

Last but not least, failing to account for the legal requirements and provisions specific to Utah can invalidate a promissory note or part of it. This may include not having the note witnessed or notarized if required, or not adhering to state-specific disclosures that might be necessary. It's essential to understand and comply with these local nuances to ensure the note's legality and enforceability.

When handling financial agreements, particularly around loans or credits in Utah, the Promissory Note is a key document. However, it’s often just one piece of the puzzle. Several other forms and documents usually work in tandem with a Promissory Note to ensure a comprehensive and legally binding agreement. Understanding these additional documents can provide both lenders and borrowers with a clearer, more secure financial arrangement. Below is an overview of some common forms and documents that are often used alongside the Utah Promissory Note.

Each of these documents plays a vital role in the lending process, offering protection and clarity for both the lender and the borrower. Whether you’re issuing or receiving a loan, understanding and properly utilizing these forms can significantly enhance the security and efficiency of the transaction. It’s always recommended to review these documents with a legal professional to ensure compliance with Utah laws and to address any specific concerns or needs related to the financial agreement.

The Promissory Note in Utah shares similarities with a Loan Agreement. Both serve as binding legal documents between a lender and a borrower, outlining the terms of a loan. The Loan Agreement, much like the Promissory Note, details the loan amount, interest rate, repayment schedule, and the consequences of non-payment. However, Loan Agreements tend to be more comprehensive, often including clauses on dispute resolution, collateral, and guarantors, making them more detailed in guiding the terms of the lending relationship.

The Mortgage Agreement is another document closely related to the Utah Promissory Note. While the Promissory Note documents the promise to repay a loan, the Mortgage Agreement secures the loan by using the borrower's property as collateral. This means if the borrower fails to repay the loan according to the Promissory Note, the lender has the right to foreclose on the property outlined in the Mortgage Agreement. Essentially, the Mortgage Agreement provides a safety net for the lender, reinforcing the borrower's obligation under the Promissory Note.

Similarly, a Deed of Trust is often paired with a Promissory Note, especially in states where this practice is common. Like a Mortgage Agreement, a Deed of Trust serves as a means to secure repayment of a loan through the borrower's property. However, it involves an additional party, a trustee, who holds the legal title to the property until the borrower repays the loan. The coupling of a Deed of Trust with a Promissory Note ensures the lender's interests are protected by granting them the power to initiate foreclosure through the trustee if the borrower defaults.

An IOU (I Owe You) is a simpler relative of the Promissory Note. It acknowledges that a debt exists, and one party owes another a certain sum of money. While both documents signify an obligation to repay, the Promissory Note is far more formal and includes detailed repayment terms, interest, and potential legal steps in case of default. An IOU, by contrast, is typically less formal and lacks comprehensive terms of repayment, making it less enforceable than a Promissory Note.

The Personal Guarantee is another document related to the realm of Promissory Notes, especially when securing loans for businesses. When a business entity takes a loan, a Personal Guarantee may be required, in which an individual (usually a business owner or executive) promises to repay the loan personally if the business cannot. This guarantee is a testament to the lender of the individual's commitment to the loan's terms outlined in the Promissory Note, significantly reducing the lender's risk.

The Installment Agreement bears similarity to the Promissory Note as well, particularly regarding repayment scheduling. It outlines a plan for repaying a debt in regular installments over a set period. While both documents set terms for repayment of a debt, the Promissory Note typically includes a broader range of details, such as interest rates and consequences of default, and it applies more universally to various types of loans beyond just installment-based repayments.

Last but not least, the Credit Agreement shares traits with the Promissory Note in that it also details the terms under which credit is extended to a borrower. Credit Agreements are often more complex and can cover revolving credit lines, term loans, and other financial arrangements. Although both documents govern the lending process, Promissory Notes are generally used for simpler, more straightforward loans, whereas Credit Agreements can manage a broader array of credit structures and terms.

Filling out the Utah Promissory Note form is a critical process that requires attention to detail and accuracy. This document serves as a legal agreement between a borrower and a lender regarding the money borrowed and the promise to pay it back under specified terms. Here are some essential dos and don'ts to guide you through this process:

Do:

Don't:

By following these guidelines, you can ensure that your Utah Promissory Note is correctly filled out, minimizing future disputes and protecting the interests of all parties involved.

When it comes to understanding legal documents, it's easy to be misled by common misconceptions, especially regarding documents like the Utah Promissory Note form. This document is pivotal in many financial transactions within the state, but misunderstandings can lead to complications. Here's a clarification of some prevalent misconceptions:

Understanding these misconceptions can prevent potential missteps in the drafting, execution, and enforcement of a promissory note in Utah. Both borrowers and lenders are encouraged to seek legal advice to ensure their interests are adequately protected and the note complies with state-specific legal requirements.

When dealing with a Utah Promissory Note, individuals are entering into a binding financial agreement. This legal document serves as a promise to pay back borrowed money, often between lenders and borrowers. Understanding the key elements and implications is crucial for both parties involved. Below are several important takeaways to consider when filling out and using the Utah Promissory Note form:

Creating and signing a promissory note is a significant financial commitment. Both lenders and borrowers should thoroughly understand the terms and legal obligations they are agreeing to. When in doubt, consulting with a legal professional who is knowledgeable about Utah law and the specifics of promissory notes can provide invaluable guidance and peace of mind.

Texas Promissory Note Template - For smaller, personal loans, a promissory note can formalize the agreement without the need for more complex loan documents.

Blank Promissory Note - In the case of default, the Promissory Note outlines the agreed-upon steps for resolution, whether through restructuring the loan or pursuing legal action.

Promissory Note Template Oregon - For non-traditional lending arrangements, this document provides a structured and legally compliant framework for repayment.

Promissory Note Template New York - Essential for setting out the conditions under which the loan can be prepaid or renegotiated.