Legal Texas Promissory Note Form

Legal Texas Promissory Note Form

In the vast expanse of Texas, financial transactions between individuals and entities often require a written agreement to ensure clarity and enforceability. A crucial tool in these engagements is the Texas Promissory Note form. This document serves as a formal commitment by a borrower to repay a specified amount of money to a lender within an agreed-upon timeframe. The beauty of this form lies in its simplicity and versatility, accommodating both secured and unsecured loans. The secured version provides lenders with added security, allowing them to claim collateral if the borrower fails to meet the repayment terms, while the unsecured version relies solely on the borrower's promise to pay. Interest rates, repayment schedules, and the consequences of defaulting on the loan are clearly outlined, making the Texas Promissory Note a foundation of trust between parties. Its straightforward structure means it can be adapted for a wide range of financial dealings, from personal loans between family members to more complex transactions between businesses. Understanding the key components and legal implications of this document can significantly reduce potential misunderstandings or disputes, ensuring a smoother financial exchange for everyone involved.

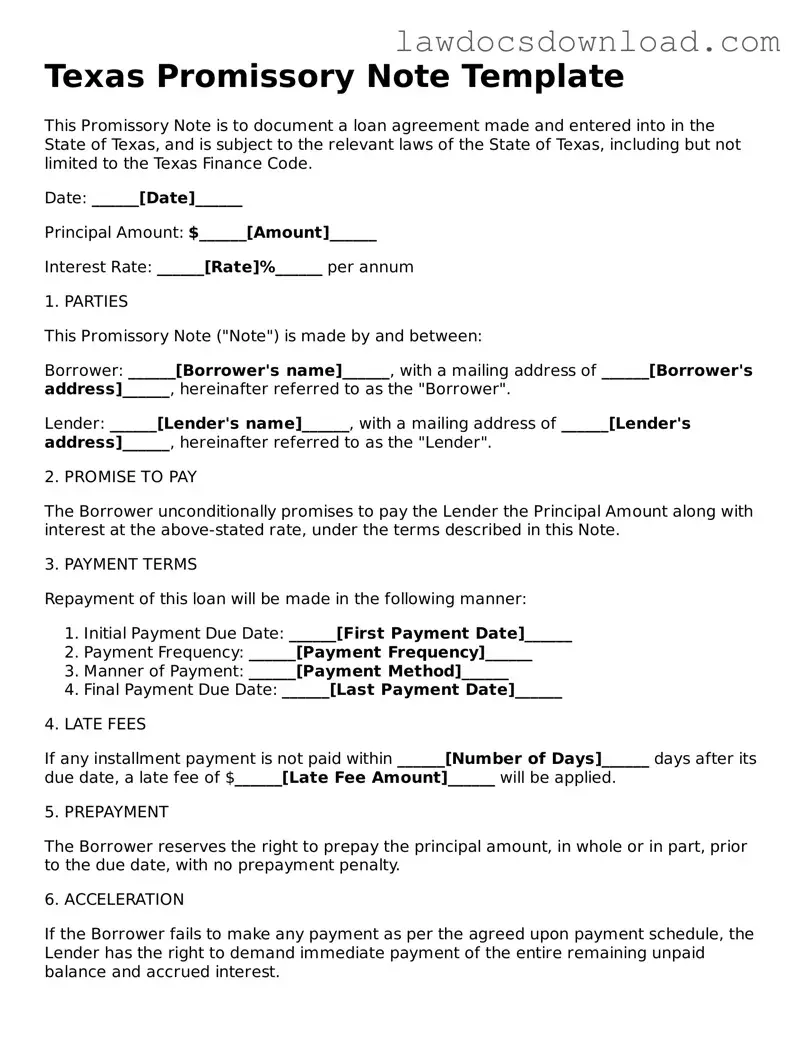

Texas Promissory Note Template

This Promissory Note is to document a loan agreement made and entered into in the State of Texas, and is subject to the relevant laws of the State of Texas, including but not limited to the Texas Finance Code.

Date: ______[Date]______

Principal Amount: $______[Amount]______

Interest Rate: ______[Rate]%______ per annum

1. PARTIES

This Promissory Note ("Note") is made by and between:

Borrower: ______[Borrower's name]______, with a mailing address of ______[Borrower's address]______, hereinafter referred to as the "Borrower".

Lender: ______[Lender's name]______, with a mailing address of ______[Lender's address]______, hereinafter referred to as the "Lender".

2. PROMISE TO PAY

The Borrower unconditionally promises to pay the Lender the Principal Amount along with interest at the above-stated rate, under the terms described in this Note.

3. PAYMENT TERMS

Repayment of this loan will be made in the following manner:

4. LATE FEES

If any installment payment is not paid within ______[Number of Days]______ days after its due date, a late fee of $______[Late Fee Amount]______ will be applied.

5. PREPAYMENT

The Borrower reserves the right to prepay the principal amount, in whole or in part, prior to the due date, with no prepayment penalty.

6. ACCELERATION

If the Borrower fails to make any payment as per the agreed upon payment schedule, the Lender has the right to demand immediate payment of the entire remaining unpaid balance and accrued interest.

7. GOVERNING LAW

This Note shall be governed under the laws of the State of Texas without regard to its conflict of law provisions.

8. SIGNATURES

This Note must be signed by both parties to be effective.

Borrower's Signature: ______[Borrower's Signature]______

Date: ______[Date of Borrower's Signature]______

Lender's Signature: ______[Lender's Signature]______

Date: ______[Date of Lender's Signature]______

| Fact Number | Detail |

|---|---|

| 1 | The Texas Promissory Note is a legal document that outlines the repayment terms of a loan between two parties in the state of Texas. |

| 2 | This form is governed by the laws of the State of Texas, including the Texas Finance Code. |

| 3 | It can be secured, meaning collateral is offered for loan assurance, or unsecured, meaning no collateral is involved. |

| 4 | Interest rates on promissory notes in Texas must comply with the state’s usury laws to avoid being considered illegal. |

| 5 | The maximum interest rate unless otherwise legally specified is 10% per annum. |

| 6 | Both parties, the borrower and the lender, must sign the note, and it’s advisable to have the signatures notarized for legal fortification. |

| 7 | The note should include the full names and addresses of both the borrower and the lender. |

| 8 | Details about the loan amount, interest rate, repayment schedule, and maturity date should be clearly stated in the note. |

| 9 | If the borrower defaults, the note will specify the options available to the lender, including demanding full payment. |

| 10 | Amendments to the note, once signed, require agreement from both the borrower and the lender to be valid. |

Filling out a Texas Promissory Note form is a straightforward process, but it requires attention to detail. This form is instrumental in formalizing the terms of a loan between two parties, specifying the amount borrowed, the interest rate, repayment schedule, and other critical terms. It serves as a legally binding agreement, ensuring that the borrower is committed to repaying the loan under the prescribed conditions. Completing this form accurately is crucial for both the lender and the borrower to protect their interests and lay down the foundation for a clear financial transaction. Below are the steps to fill out the Texas Promissory Note form efficiently.

Once completed, a copy of the promissory note should be kept by both the lender and the borrower. It's advisable to review the note carefully before signing to ensure that all the terms are correct and fully understood. This form is not just a record of a financial transaction but also serves as a legal commitment between two parties with enforceable terms and conditions. Taking the time to fill out the form meticulously will help in avoiding potential misunderstandings or disputes in the future.

What is a Texas Promissory Note?

A Texas Promissory Note is a legal document that acts as a written promise from one party (the borrower) to repay a certain amount of money to another party (the lender). This document outlines the amount of money borrowed, the interest rate, repayment schedule, and other terms related to the repayment of the loan.

Is a Texas Promissory Note legally binding?

Yes, in Texas, a promissory note is considered a legally binding agreement once it is signed by both the borrower and lender. It must contain essential elements like the loan amount, interest rate, repayment terms, and the signatures of both parties to be considered valid.

What types of Promissory Notes are available in Texas?

In Texas, there are generally two types of promissory notes:

What information needs to be included in a Texas Promissory Note?

A comprehensive Texas Promissory Note should include:

How is the interest rate determined for a Texas Promissory Note?

The interest rate on a promissory note in Texas should comply with state regulations. Texas has a maximum allowable interest rate, and any rate charged above this may be considered usurious unless specific exceptions apply. It's crucial for both parties to agree upon an interest rate within legal limits and to clearly state this rate in the promissory note.

What are the consequences of non-payment according to Texas law?

Under Texas law, if a borrower fails to pay according to the terms of the promissory note, the lender may pursue legal action to collect the debt. For a secured promissory note, the lender may also have the right to seize the collateral. Additionally, late fees and interest rates may continue to accumulate on the unpaid balance.

Can a Texas Promissory Note be modified?

Yes, a Texas Promissory Note can be modified if both the borrower and the lender agree to the changes. Any modifications should be made in writing, and both parties must sign the amended agreement for the changes to be legally binding.

Is it necessary to have a Texas Promissory Note notarized?

While notarization is not a legal requirement for promissory notes in Texas, having the document notarized can add an extra layer of authenticity. This can be helpful if the agreement ever needs to be enforced in court.

How can a Texas Promissory Note be enforced if the borrower fails to repay the loan?

If a borrower fails to repay according to the terms of the promissory note, the lender has the right to file a lawsuit to enforce the agreement and recover the owed amount. For secured loans, the lender may also proceed with seizing the collateral. Legal advice should be sought to navigate this process effectively.

Where can I obtain a Texas Promissory Note template?

Templates for Texas Promissory Notes can be found online through legal services websites, at local libraries, or from attorneys who specialize in finance and contracts. Ensure that any template used complies with Texas law and meets the specific needs of your agreement.

When navigating the legal terrain of promissory notes in Texas, individuals often stumble over a handful of common pitfalls. These documents, crucial for outlining the repayment terms of a loan, must be handled with precision and understanding. Without sufficient caution, one might inadvertently set the stage for misunderstandings or legal complications down the line.

One frequently encountered error is neglecting to specify the interest rate distinctly. Texas law mandates clear communication of interest rates in such agreements to prevent usury, the act of charging excessively high interest. An undefined interest rate can not only render the agreement legally unenforceable but also trigger financial penalties against the lender.

Another mistake is failing to include a detailed repayment schedule. It’s crucial to outline the timing, amount, and method of payments to avoid any ambiguity. A lack of such specifics can lead to disputes over expected payment dates and amounts, complicating the borrower-lender relationship unnecessarily.

The omission of collateral details, if the loan is secured, is a significant oversight. In Texas, a secured promissory note must describe the collateral that backs the loan. This omission can weaken the lender's position, making it harder to claim the collateral if the borrower defaults on the loan.

Moreover, some individuals mistakenly believe that a witness or notarization is not required for their promissory note to be valid. While it's true that Texas law does not universally mandate these for the enforceability of the document, including them can add an extra layer of legal protection and authenticity, especially in disputes.

Another common pitfall is ignoring the need for a co-signer when the borrower's creditworthiness is in question. Failure to secure a co-signer can leave the lender vulnerably exposed to unnecessary risk.

Failure to assert a clear course of action in the event of a default is another overlooked aspect. Specifying the repercussions for missed or late payments, including potential acceleration of the debt, ensures both parties are aware of the consequences and can prevent borrowers from exploiting loopholes.

Additionally, the exclusion of a governing law clause is a subtle yet impactful misstep. In the absence of such a clause, confusion can arise over which state’s laws apply to the note, especially if the parties reside in or move to different states. This clarity is pivotal in resolving disputes.

Lastly, many neglect to update the promissory note to reflect any agreed-upon changes over the life of the loan. Amendments made verbally or without documentation can significantly complicate enforcement efforts.

Understanding and avoiding these common mistakes can ensure that the crafting of a Texas Promissory Note is not only compliant with state laws but also serves as a robust agreement that protects the interests of both lender and borrower.

When dealing with financial transactions, particularly those involving loans in Texas, the Promissory Note becomes a fundamental document. However, to ensure that the lending process is properly documented and legally compliant, other forms and documents often accompany the Promissory Note. Each of these documents serves a distinct purpose, adding layers of legal protection and clarity for both the borrower and the lender. Below is a list of additional forms and documents that are commonly used in conjunction with the Texas Promissory Note form.

Together, these documents form a comprehensive legal framework that governs the lending process. Each plays a vital role in detailing expectations, rights, and responsibilities of all parties involved, ensuring that the transaction remains transparent, secure, and within the confines of Texas law. Proper utilization and understanding of these forms can help prevent legal issues and misunderstandings throughout the duration of the loan.

The Texas Promissory Note form shares similarities with the Mortgage Agreement in that both are legal documents involving a promise to pay. In a Mortgage Agreement, this promise is secured by real property, whereas a promissory note may not necessarily involve collateral. However, both lay out terms for repayment and are legally binding, establishing an obligation to pay under specified conditions.

Similarly, the Loan Agreement is akin to the Texas Promissory Note, as both formalize a borrowing arrangement between two parties. The Loan Agreement, however, often details more comprehensive terms and conditions, such as the rights and responsibilities of both the borrower and lender, and may encompass a broader scope of clauses pertaining to breach of agreement and remedies. Both documents signify an enforceable promise to repay a sum of money.

The IOU (I Owe You) document, while less formal, is another similar document. It acknowledges that a debt exists, much like a promissory note. However, an IOU is not as detailed and lacks the legal formalities and structured repayment plan that a promissory note includes. It’s more of an informal acknowledgment of debt without the comprehensive terms of repayment and interest that a promissory note stipulates.

Debt Settlement Agreements also relate to the Texas Promissory Note in their concern with the repayment of debts. These agreements are used when modifying the original terms of a debt repayment, often reducing the owed amount or altering the repayment schedule. Like promissory notes, they are legally binding but are used post facto, once the original terms of repayment need adjustment, unlike promissory notes which set the terms from the outset.

A Personal Guarantee is comparable because it also involves a promise to pay, specifically ensuring the debt of another is paid. Personal Guarantees add another layer of security for the lender, similarly to secured promissory notes which are backed by collateral. While a promissory note directly involves the parties in the loan, a personal guarantee usually involves a third party as a guarantor, adding an extra commitment to the obligation to repay.

The Installment Agreement shares traits with the Texas Promissory Note form through its structure of repayment in segments over time. While a Promissory Note may specify a lump sum or a structured schedule of payments, an Installment Agreement specifically breaks down the debt into periodic, often equally-sized, payments. Both legally bind the borrower to a schedule of repayment, yet the installment plan focuses more vehemently on the timing and size of each payment.

The Credit Agreement is another document related to the Texas Promissory Note, as it is used to outline the terms of credit extended by one party to another. Like promissory notes, credit agreements specify repayment terms, interest rates, and the obligations of each party. The key difference is that credit agreements are often more complex, may involve revolving credit lines, and typically cover broader relationships than the single-debt focus of a promissory note.

Lastly, the Security Agreement, while distinct, is connected to the essence of a secured promissory note by detailing collateral for a loan. It outlines the property or assets pledged as security, making it similar to secured promissory notes which may require collateral to guarantee repayment. Both documents protect the lender's interests by providing a means to recoup the loaned funds in the event of default, though the Security Agreement specifically focuses on the collateral details.

Do clearly identify the parties involved. Make sure to provide the full legal names of both the borrower and the lender to avoid any ambiguity regarding the parties to the agreement.

Do specify the loan amount in clear terms. It is essential to write out the loan amount in words and then repeat it in numbers to ensure there's no confusion about the sum being borrowed.

Do define the repayment terms explicitly. Whether it's a lump sum payment or an installment plan, detailing the frequency and size of payments can prevent misunderstandings later on.

Do include the interest rate. In specifying the interest rate, ensure that it complies with Texas state laws to prevent the agreement from being considered usurious.

Do outline the consequences of default. Clearly stating what constitutes a default and the consequent actions can protect both parties if disputes arise.

Don't omit the date. The agreement should have a date indicating when the promissory note comes into effect, which could also impact the statute of limitations.

Don't neglect to specify security or collateral, if applicable. If the loan is secured, describe the collateral in detail to ensure it is clear what is at risk should the borrower fail to fulfill the repayment terms.

Don't forget to have the promissory note signed. Both the borrower and the lender (or their authorized representatives) should sign the note for it to be legally enforceable.

Don't overlook the need for an impartial witness or notarization, depending on the amount or complexity of the loan. Though not always mandatory, having a witness or notarization can add an extra layer of legal protection.

When it comes to financial agreements, confusion often arises, especially with instruments like the Texas Promissory Note form. Several misconceptions exist, which can lead to misunderstandings or mismanagement of these documents. Below are eight common misconceptions people have about the Texas Promissory Note form, clarified to provide a better understanding.

Clarifying these misconceptions ensures that parties entering into a promissory note agreement in Texas do so with a clear understanding of their rights and obligations. It is always recommended to seek legal guidance when drafting or signing any legal document to ensure compliance with state laws and regulations.

The Texas Promissory Note form is a legal document that outlines the terms under which money has been loaned and the repayment agreement. Whether you're the borrower or lender, understanding the key components of this document can help ensure the process goes smoothly. Below are eight essential takeaways about filling out and using the Texas Promissory Note form:

By paying attention to these essential aspects of the Texas Promissory Note form, both lenders and borrowers can help protect their interests and ensure that the loan process is conducted fairly and legally.

Blank Promissory Note - The inclusion of a co-signer or guarantor can be stipulated, offering additional security for the lender by holding another party responsible should the primary borrower default.

Does Promissory Note Need to Be Notarized - This document helps in creating a clear financial agreement, reducing misunderstandings between the parties involved.

Blank Promissory Note - Promissory notes are essential for setting clear expectations and responsibilities for both lender and borrower.