Legal Texas Loan Agreement Form

Legal Texas Loan Agreement Form

Embarking on a financial agreement in the Lone Star State, especially when it involves lending money, is no small feat. The Texas Loan Agreement form serves as the cornerstone of such transactions, ensuring clarity, legality, and the peace of mind for both the lender and the borrower. This document meticulously outlines the loan's terms and conditions, including the principal amount, interest rates, repayment schedule, and any collateral involved. Its comprehensive nature addresses state-specific legal requirements, safeguarding all parties' interests and providing a solid foundation for enforceability. Beyond its function as a binding contract, the form also educates and guides participants through the financial and legal intricacies of the loan process. The significance of this document cannot be overstated, as it not only prevents potential misunderstandings and disputes but also reinforces the mutual commitment to fulfill the agreed-upon obligations.

Texas Loan Agreement Template

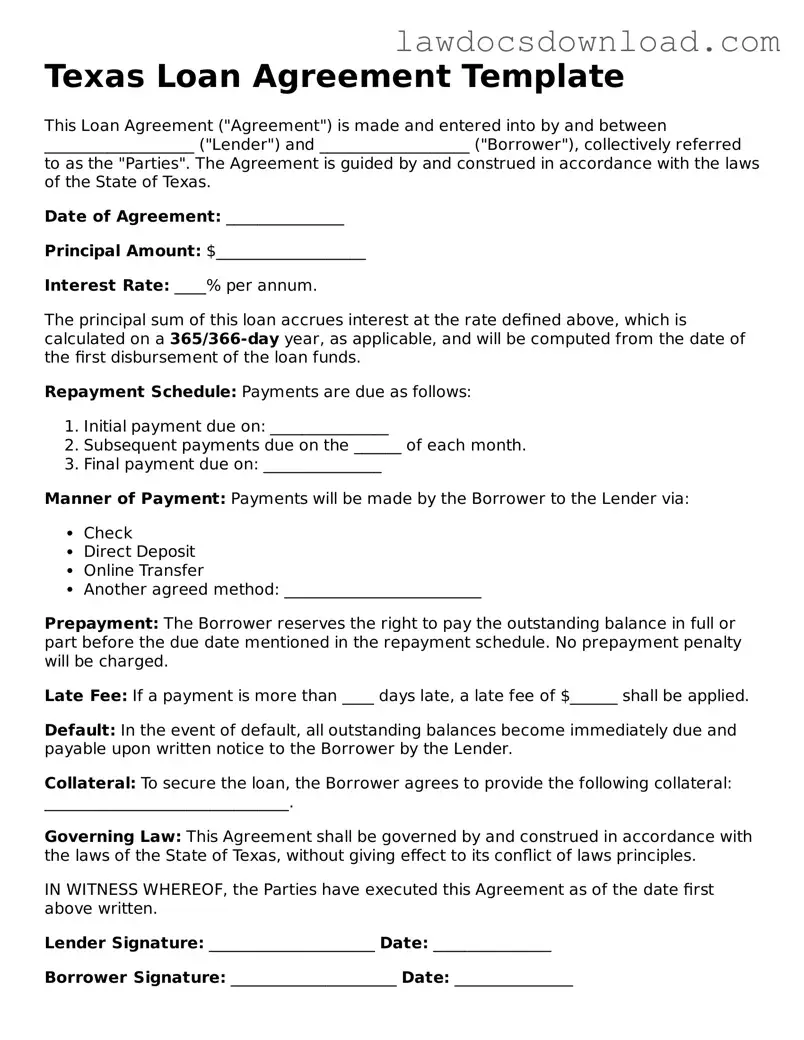

This Loan Agreement ("Agreement") is made and entered into by and between ___________________ ("Lender") and ___________________ ("Borrower"), collectively referred to as the "Parties". The Agreement is guided by and construed in accordance with the laws of the State of Texas.

Date of Agreement: _______________

Principal Amount: $___________________

Interest Rate: ____% per annum.

The principal sum of this loan accrues interest at the rate defined above, which is calculated on a 365/366-day year, as applicable, and will be computed from the date of the first disbursement of the loan funds.

Repayment Schedule: Payments are due as follows:

Manner of Payment: Payments will be made by the Borrower to the Lender via:

Prepayment: The Borrower reserves the right to pay the outstanding balance in full or part before the due date mentioned in the repayment schedule. No prepayment penalty will be charged.

Late Fee: If a payment is more than ____ days late, a late fee of $______ shall be applied.

Default: In the event of default, all outstanding balances become immediately due and payable upon written notice to the Borrower by the Lender.

Collateral: To secure the loan, the Borrower agrees to provide the following collateral: _______________________________.

Governing Law: This Agreement shall be governed by and construed in accordance with the laws of the State of Texas, without giving effect to its conflict of laws principles.

IN WITNESS WHEREOF, the Parties have executed this Agreement as of the date first above written.

Lender Signature: _____________________ Date: _______________

Borrower Signature: _____________________ Date: _______________

| Fact Name | Description |

|---|---|

| Governing Law | The Texas Loan Agreement form is governed by the laws of the state of Texas. |

| Use | This form is used when one party (the lender) agrees to lend a specific amount of money to another party (the borrower). |

| Components | It typically includes sections on the loan amount, interest rate, repayment schedule, and consequences of default. |

| Interest Rate | The interest rate must be specified and comply with Texas usury laws to avoid being considered predatory. |

| Repayment Schedule | Details when and how the borrower is to repay the loan, including any installments. |

| Default Consequences | Outlines what happens if the borrower fails to make payments as agreed, including any penalties or legal actions. |

| Signature Requirement | Both parties must sign the agreement, making it a legally binding document. |

| Notarization | While not always required, notarization can add an extra layer of legal protection and validity to the agreement. |

| Modification | Any changes to the agreement must be done in writing and signed by both parties to be valid. |

| Prepayment | The agreement can include terms for prepayment, which may or may not include penalties for the borrower. |

Entering into a Loan Agreement in Texas is a formal process that establishes the terms and conditions under which money is borrowed and should be repaid. It's a legally binding document between the borrower and the lender that outlines how much is being borrowed, the interest rate, repayment schedule, and the consequences of defaulting on the loan. Before jumping into filling out the form, it's important to gather all necessary information including personal identification, financial data, and specifics about the loan terms. Accuracy and attention to detail are key to ensure that the agreement is executed correctly and legally binding.

Upon completing these steps, the Loan Agreement becomes a binding contract that holds both parties to their responsibilities and terms outlined. It's important for both the lender and the borrower to keep a copy of the agreement for future reference. If questions or disputes arise later, the agreement serves as a legal reference point that can help in finding a resolution. Always remember, when in doubt, consulting with a legal professional can provide clarity and ensure that all aspects of the agreement are in compliance with state laws.

What is a Texas Loan Agreement form?

A Texas Loan Agreement form is a legal document that outlines the terms and conditions under which money is lent. It details the loan amount, interest rate, repayment schedule, and the obligations of both the borrower and the lender. This agreement is essential in Texas to ensure both parties are clear on the terms and to provide legal protection should any disputes arise.

Who needs to use a Texas Loan Agreement form?

Anyone lending or borrowing money in Texas should use a Loan Agreement form. This includes individuals, businesses, and entities engaging in loan transactions. Utilizing this form ensures that the loan process is transparent and legally binding, which helps protect the interests of both the lender and the borrower.

What key elements should be included in this form?

Is a witness or notarization required for a Texas Loan Agreement form?

While not always legally required, having a witness or notarization can add an additional layer of validity and protection for both parties involved. It can be particularly useful for enforcing the agreement or in case of disputes. It's recommended to consider notarization or having witnesses at signing.

Can I modify a Texas Loan Agreement form after it's been signed?

Yes, but any modifications to the agreement must be made in writing and signed by both the lender and the borrower. Oral agreements or understandings are generally not recognized. It’s crucial to document and mutually agree upon any changes to ensure they are legally binding.

What happens if the borrower defaults on the loan?

If a borrower defaults on the loan, the lender has the right to take legal action to recover the loaned amount. The specific recourse available to the lender, such as seizing collateral or pursuing a judgment for the balance owed, depends on the terms outlined in the Loan Agreement and Texas law.

How does a Texas Loan Agreement protect the borrower?

It clearly outlines the lender's expectations and any applicable legal protections for the borrower, such as limits on interest rates and fees as dictated by Texas law. Additionally, it provides a structured repayment plan, helping the borrower to understand and meet their obligations.

Are electronic signatures valid on a Texas Loan Agreement form?

Yes, electronic signatures are generally recognized as valid and legally binding in Texas, just like traditional handwritten signatures. However, it's important to ensure that the electronic signing process conforms to relevant laws and that both parties agree to use electronic signatures.

Where can I find a Texas Loan Agreement form?

Texas Loan Agreement forms can be found through legal document providers, attorneys specializing in financial agreements, or online resources that offer standardized forms. Ensure any form used is up-to-date with current Texas laws to provide proper legal protection.

In the state of Texas, and indeed throughout much of the United States, the process of completing a loan agreement form can be fraught with potential for error. Particularly for those not well-versed in the field of law or finance, certain common missteps can significantly impact the validity and enforceability of the contract. One of the foremost mistakes encountered involves a failure to clearly define the terms of the loan. Without the explicit stipulation of loan amounts, interest rates, repayment schedules, and the obligations of each party, the agreement can become a source of disputes and misunderstandings, potentially leading to litigation or financial loss.

Another prevalent mistake lies in overlooking the necessity of detailing the collateral, if any, secured against the loan. This oversight can result in ambiguity concerning the rights to assets in the event of default. Ensuring that all collateral is accurately described and legally associated with the loan agreement is crucial for both the lender's security and the borrower's understanding of their responsibilities.

A further error often made is neglecting to include provisions for late payments or defaults. A comprehensive loan agreement should outline the consequences of late payments, such as additional fees or higher interest rates, as well as the remedies available to the lender if the borrower fails to fulfill their repayment obligations. Without these provisions, enforcing the terms of the loan or recouping potential losses becomes a more complicated matter.

Individuals also frequently err by omitting a choice of law clause. This clause determines which state's laws will govern the interpretation and enforcement of the agreement. The absence of such a clause can lead to uncertainty and extensive legal debate, particularly if the parties to the loan are from different jurisdictions.

Improper or incomplete documentation of the agreement is a critical mistake. Both parties should ensure that the loan agreement is documented in writing, fully signed, and witnessed if required by state law. Reliance on oral agreements or handshake deals can lead to significant legal vulnerabilities and misinterpretations of the terms agreed upon.

Sometimes, individuals mistakenly believe that a notary's signature is always required on a loan agreement in Texas. While having a notarized document can add a layer of formality and credibility, it is not a legal necessity for all types of loan agreements. However, understanding when such a requirement applies is essential for the legality and enforceability of the document.

Another error made during the drafting of loan agreements is the failure to conduct a thorough verification of the identities and legal standing of the parties involved. Ensuring that each party has the legal capacity to enter into a loan agreement and verifying their identities can prevent fraud and misunderstandings.

Lastly, parties occasionally proceed without considering the requirement for witness signatures or specific filing procedures relevant to certain types of loan agreements. While not always mandatory, understanding and adhering to these requirements can enhance the enforceability of the agreement and protect the interests of both the lender and the borrower.

In conclusion, when filling out a loan agreement form in Texas, attention to detail, and a comprehensive understanding of the legal and financial obligations entailed are paramount. Avoidance of the aforementioned mistakes can help ensure that the agreement serves its intended purpose without leading to unnecessary conflicts or legal challenges.

When entering into a Loan Agreement in Texas, it's essential to understand that this is often just the start. Various other documents and forms may be necessary to support, clarify, or enforce the terms of the agreement. From ensuring the security of the lender to providing the borrower with certain protections, these additional documents are vital for a comprehensive legal framework around the loan. Let's explore some of the key documents often used alongside the Texas Loan Agreement form.

Creating a complete and legally binding loan package requires attention to detail and an understanding of the specific needs and risks involved in the loan arrangement. These documents, when used alongside a Texas Loan Agreement, form a robust legal foundation that protects both the lender's and borrower's interests. Legal professionals can provide invaluable assistance in drafting and reviewing these documents to ensure they meet all legal requirements and serve the intended purpose effectively.

The Promissory Note is one document similar to the Texas Loan Agreement form because it serves as a written promise to pay a specific amount of money to someone within a set time frame. Like loan agreements, promissory notes outline repayment terms, including interest rates and due dates, offering a clear financial obligation and understanding between the involved parties.

A Mortgage Agreement shares similarities with the Texas Loan Agreement in that both involve a borrower agreeing to specific terms under which they are lent money, with the premise that the loan will be repaid over time. The key difference is that a Mortgage Agreement is secured against a piece of real estate, which acts as collateral for the loan. This ensures that if the borrower fails to meet the repayment terms, the lender may take possession of the collateral.

The Personal Loan Agreement, much like the Texas Loan Agreement, details the terms under which an individual borrows money from another individual or a business entity. These documents typically include information on repayment schedules, interest rates, and the consequences of non-payment, facilitating a clear agreement to be followed by both parties.

Lines of Credit Contracts are akin to the Texas Loan Agreement form where they outline the terms under which a lender provides access to funds that a borrower can draw upon as needed, up to a specified limit. The repayment terms, including interest rates and how the interest is calculated, are detailed in both types of agreements, making them crucial for managing financial transactions.

The Business Loan Agreement is another document that bears resemblance to the Texas Loan Agreement form by specifying the terms under which one party lends money to a business entity. These documents are crafted to include details such as the loan amount, interest rate, repayment schedule, and collateral involved, ensuring both parties have a clear understanding of the obligations and rights.

Peer-to-Peer Loan Agreements resemble the Texas Loan Agreement, as they formalize the process of one individual lending money to another with specific repayment terms. These agreements include details about repayment periods, interest rates, and the consequences of failing to meet the agreed-upon terms, mirroring the purpose and structure of traditional loan agreements.

A Debt Settlement Agreement is somewhat like the Texas Loan Agreement, focusing on the terms under which the borrower will pay back a portion of the owed money while the rest is forgiven by the lender. This type of agreement comes into play when the borrower can't repay the full amount, highlighting negotiated new terms for the repayment, similar to how loan modifications might be documented.

Finally, Equipment Financing Agreements are related to Texas Loan Agreements as they specifically pertain to the lending of money for the purpose of purchasing equipment. Like other loan agreements, these contracts detail the loan amount, repayment schedule, interest rates, and the equipment itself acting as collateral. This specificity towards equipment purchase distinguishes it from more general loan agreements.

Filling out a Texas Loan Agreement form is an essential step in formalizing a loan either between individuals or between an individual and an establishment. The process requires attention to detail and an understanding of what is legally binding. Below are guidelines on what you should and shouldn't do to ensure the agreement is effective and protects all parties involved.

By following these dos and don'ts, individuals can fill out the Texas Loan Agreement form more confidently and securely. Remember, this document is not just a formality but a binding contract that outlines the responsibilities and expectations of all parties. It's imperative to approach this document with the seriousness it demands.

When dealing with the Texas Loan Agreement form, various misconceptions often arise. Addressing these misunderstandings can help borrowers and lenders navigate their agreements with more confidence and clarity. Here are nine common misconceptions explained:

It only applies to commercial loans. Many assume that the Texas Loan Agreement form is exclusively for commercial transactions. However, it can also be used for personal loans between individuals. The form is versatile and can accommodate different types of loan agreements.

The form is too complicated for non-lawyers. While legal documents can be daunting, the Texas Loan Agreement form is designed to be understandable. With clear instructions and sections, individuals can fill it out without requiring a legal background. Assistance from a legal consultant can help clarify any complex clauses.

All loan agreements in Texas must use this form. This is not accurate. The Texas Loan Agreement form is a useful tool, but parties are free to craft their own agreements or use other formats as long as they comply with Texas laws.

The terms are non-negotiable. Every part of the Texas Loan Agreement form can be tailored to the specifics of the loan. Both lenders and borrowers should review and negotiate terms until they reach an agreement that suits both parties.

Interest rates are fixed by the form. The form allows for flexibility regarding interest rates. Parties can agree on fixed or variable rates as long as they do not exceed the legal maximum in Texas.

No legal consultation is necessary. While it's possible to complete the form without legal help, consulting with a legal professional can provide valuable insights, especially for complex loans or large amounts. They can ensure that the agreement complies with state laws and advise on potential risks.

It only covers the principal amount and interest. The form can include various other terms, such as repayment schedules, collateral, late fees, and consequences of default. It's important to address these aspects comprehensively in the agreement.

Electronic signatures are not valid. Texas law recognizes electronic signatures, making it convenient for parties to sign the loan agreement digitally. This ensures that the process is legally binding and can be completed more efficiently.

A witness or notary is always required. While having a witness or notarizing the document can add a layer of verification, it is not always a mandatory requirement for the Texas Loan Agreement to be valid. However, in certain cases, it might be advisable for added legal protection.

Understanding these common misconceptions can help parties involved in a loan to make informed decisions. It’s always advisable to approach loan agreements with due diligence and, when needed, the guidance of a professional.

Entering into a loan agreement in Texas is an important process that requires attention to detail and a clear understanding of the terms involved. Whether you're lending or borrowing, a well-drafted Texas Loan Agreement form safeguards the interests of both parties. Here are 5 key takeaways to consider when filling out and using this form:

By keeping these key points in mind, both lenders and borrowers can navigate the process of entering into a loan agreement with greater ease and confidence. It's about ensuring clarity, legal protection, and mutual understanding from the get-go.

Promissory Note Template Georgia - This legally binding document can help prevent misunderstandings and disagreements between the lender and borrower.

Promissory Note New York - Describes the terms under which a lender provides funds to a borrower, including how those funds must be paid back, with interest, over time.

Sample Promissory Note Florida - The form may specify the obligation of the borrower to pay all legal fees should a dispute arise.

Maryland Promissory Note Download - Borrowers are often required to maintain good standing with certain financial practices as outlined in the agreement.