Blank Promissory Note for a Car Template

Blank Promissory Note for a Car Template

When buying or selling a car, a critical document to understand is the Promissory Note for a Car. This form plays a pivotal role in the transaction, offering a structured and legally binding agreement between the buyer and the seller. It outlines the terms of the loan, if the purchase is not being made outright, ensuring that both parties are clear on the amount borrowed, the interest rate, repayment schedule, and any consequences of failing to meet these terms. The significance of this document cannot be overstated, as it protects the interests of both parties, provides a clear record of the agreement, and can serve as evidence in case of any disputes. Understanding the intricacies of this form is essential for a smooth transaction and can help prevent potential legal complications down the line.

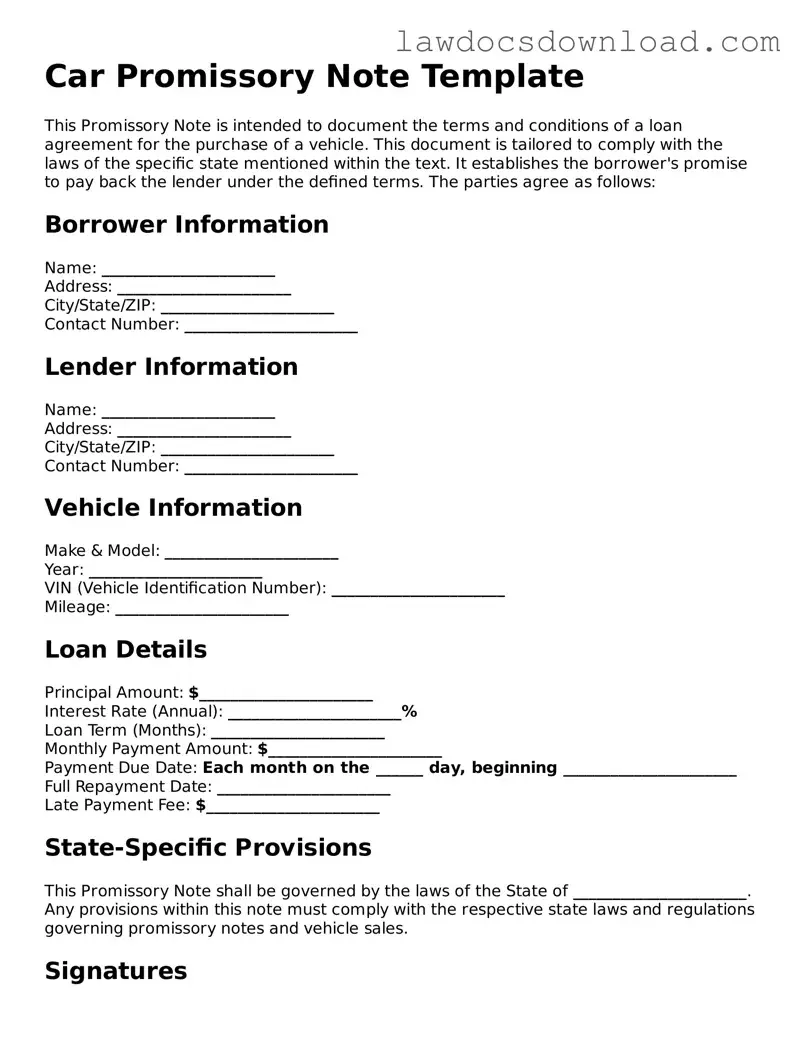

Car Promissory Note Template

This Promissory Note is intended to document the terms and conditions of a loan agreement for the purchase of a vehicle. This document is tailored to comply with the laws of the specific state mentioned within the text. It establishes the borrower's promise to pay back the lender under the defined terms. The parties agree as follows:

Borrower Information

Name: ______________________

Address: ______________________

City/State/ZIP: ______________________

Contact Number: ______________________

Lender Information

Name: ______________________

Address: ______________________

City/State/ZIP: ______________________

Contact Number: ______________________

Vehicle Information

Make & Model: ______________________

Year: ______________________

VIN (Vehicle Identification Number): ______________________

Mileage: ______________________

Loan Details

Principal Amount: $______________________

Interest Rate (Annual): ______________________%

Loan Term (Months): ______________________

Monthly Payment Amount: $______________________

Payment Due Date: Each month on the ______ day, beginning ______________________

Full Repayment Date: ______________________

Late Payment Fee: $______________________

State-Specific Provisions

This Promissory Note shall be governed by the laws of the State of ______________________. Any provisions within this note must comply with the respective state laws and regulations governing promissory notes and vehicle sales.

Signatures

Both the Borrower and the Lender acknowledge and agree to the terms set forth in this Promissory Note by their signatures below:

Borrower's Signature: ______________________Date: ______________________

Lender's Signature: ______________________Date: ______________________

Witness Information (If Applicable)

Name: ______________________

Signature: ______________________Date: ______________________

| Fact Name | Description |

|---|---|

| Definition | A Promissory Note for a Car is a form of agreement where the borrower promises to pay back the lender the amount borrowed to purchase the vehicle, often with interest, over a specified period. |

| Components | Typically includes the loan amount, interest rate, repayment schedule, collateral details (the car), and any other terms agreed upon by the parties. |

| Governing Law | These notes are governed by state laws, which can vary significantly. It's crucial to refer to your specific state's laws for precise regulations and requirements. |

| Importance of Accuracy | Accuracy in the Promissory Note is vital to ensure both parties understand their obligations, preventing future conflicts and potential legal issues. |

| Use in Private Sales | Especially useful in private car sales where the buyer does not have the full amount to pay upfront. It facilitates payment over time, under agreed conditions. |

When embarking on the purchase of a car through a private sale, it's crucial to document the financial arrangement between the buyer and the seller in a structured manner. A Promissory Note serves this purpose by providing a binding agreement that outlines the repayment terms for the amount borrowed to purchase the car. The following steps are designed to guide individuals through the process of filling out a Promissory Note for a Car, ensuring clarity and understanding for both parties involved. This document, once completed, brings a level of formality and security to the transaction, allowing peace of mind as the parties move forward.

Following these steps meticulously when filling out a Promissory Note for a Car will create a clear, enforceable document that outlines the responsibilities of each party. This measure, while straightforward, provides a valuable layer of protection and clarity, facilitating a smoother transaction and fostering a mutual understanding between the buyer and the seller.

What is a Promissory Note for a Car?

A Promissory Note for a Car is a binding legal document where the borrower agrees to pay back the lender, the amount borrowed to purchase a car, along with any interest, by a set date. It outlines the terms of the loan, including the loan amount, interest rate, repayment schedule, and the consequences of failing to make payments on time.

When should I use a Promissory Note for a Car?

You should use a Promissory Note for a Car when borrowing or lending money for the purchase of a vehicle. Using this document helps to ensure that both parties have a clear understanding of the loan's terms and conditions, and it provides legal protection in case of disputes or misunderstandings.

What information is needed to fill out a Promissory Note for a Car?

How is the interest rate determined in a Promissory Note for a Car?

The interest rate in a Promissory Note for a Car is agreed upon by both the borrower and the lender at the time of the loan's origination. It can be a fixed rate that remains constant throughout the term of the loan, or a variable rate that can fluctuate based on certain financial indices. The agreed-upon rate should reflect prevailing market rates and comply with state usury laws to prevent illegal interest charges.

Is a Promissory Note for a Car legally binding?

Yes, a Promissory Note for a Car is a legally binding agreement. Once both the borrower and the lender sign it, they are legally obligated to adhere to its terms. Failure to do so, such as missing payments, can lead to legal consequences, including the right for the lender to demand full repayment or take possession of the vehicle.

What happens if I'm late on a payment?

If you're late on a payment according to the terms of the Promissory Note, you might incur late fees, increased interest rates, and potentially impact your credit score. The specific consequences depend on the terms outlined in the promissory note. It's essential to communicate with the lender if you anticipate difficulty in making payments to possibly negotiate temporary adjustments to the payment schedule.

Can a Promissory Note for a Car be modified?

Yes, a Promissory Note for a Car can be modified, but any changes must be agreed upon by both the borrower and the lender. The modifications should be documented in writing, and both parties should sign the updated agreement to make it legally binding. It's crucial to clearly document any changes to ensure that both parties have a mutual understanding of the new terms.

How do I enforce a Promissory Note for a Car?

Enforcing a Promissory Note for a Car typically involves legal action if the borrower fails to meet the terms. The initial step is often a formal demand for payment. If payment is not received, the lender may have the right to repossess the vehicle or seek repayment through court action. Consulting with an attorney to understand the specific enforcement options available based on the note's terms and local laws is advisable.

What should I do if I can no longer make payments?

If you find yourself unable to make payments as agreed in the Promissory Note, communicate with the lender as soon as possible. Many lenders prefer to work out a modified payment plan rather than initiate repossession or legal actions. Open and honest communication can lead to an agreement that suits both parties, avoiding negative consequences on your credit and ownership of the vehicle.

When completing a Promissory Note for a car, individuals often navigate through complexities and intricate details which are critical for the document's legality and enforceability. A common pitfall is overlooking the need to accurately describe the vehicle. Precision is key; including the make, model, year, and VIN (Vehicle Identification Number) ensures that there is no ambiguity about the asset in question. Missing or inaccurate details can render the agreement void or complicate enforcement, underlining the importance of thoroughness in this initial step.

Another misstep is neglecting to clearly outline the repayment terms. It's vital that the document specifies the loan amount, interest rate, repayment schedule, and conditions for late payments or default. Without these details, the expectations for both parties remain undefined, making it harder to enforce the agreement. Clarity in the terms of repayment safeguards the interests of both the lender and the borrower, ensuring a mutual understanding and reducing potential conflicts.

The acknowledgment of collateral, beyond the car itself, often gets overlooked. In some instances, additional security may be required by the lender. Failure to include this information in the Promissory Note can complicate matters if a default occurs. The omission of such details hinders the lender's ability to claim the collateral, thereby weakening the security of the loan. Ensuring that all forms of collateral are listed strengthens the agreement and provides a clearer course of action should complications arise.

Finally, many fail to have the document duly signed and witnessed. The authenticity and legality of the Promissory Note rest significantly on its execution, namely the presence of signatures from all parties involved and, where applicable, a witness or notary. Skipping this step can jeopardize the enforceability of the document, leaving the lender particularly vulnerable. Authenticating the document through proper signing practices confirms the agreement's validity and makes it legally binding, an essential safeguard for all involved.

When purchasing or selling a car, particularly in private transactions, the promissory note is a critical document, outlining the borrower's promise to pay back the seller according to the agreed terms. However, to ensure a smooth, legally sound transfer and to protect both parties, other documents are often used alongside the Promissory Note. These include contracts specifying the sale's terms, government forms for registration, and documents protecting the seller's rights or specifying the vehicle's condition. Understanding these documents can enhance the security and clarity of the transaction.

Together, these documents form a comprehensive package that supports the promissory note, ensures all parties are adequately informed, and secures their legal and financial interests. By understanding and properly using these documents, buyers and sellers can navigate the complexities of vehicle transactions with greater confidence and legal protection.

A Loan Agreement is closely related to a Promissory Note for a Car, as both outline the terms under which money is lent to purchase something, but a Loan Agreement typically provides more comprehensive details. It specifies the obligations of each party, interest rates, repayment terms, and the consequences of default. This document is often more formal and can include clauses concerning the resolution of disputes and jurisdiction, making it broader in scope than a simple promissory note.

A Mortgage Agreement shares similarities with a Promissory Note for a Car because both are forms of secured loans. In a Mortgage Agreement, the property is used as security for the loan, much like how a vehicle secures the loan in a Promissory Note for a Car. Both documents outline borrower’s repayment obligations and specify what happens if the borrower fails to make payments. However, a Mortgage Agreement typically involves real estate, whereas a Promissory Note for a Car is specific to vehicles.

A Personal Loan Agreement is similar because it also documents a loan between two parties, but it's more general and can apply to various types of loans beyond just vehicle purchases. Like a Promissory Note for a Car, it outlines the loan amount, repayment schedule, interest rate, and the consequences of not repaying the loan. The key difference is in their specificity; the Personal Loan Agreement isn't limited to car purchases and can cover a wide range of personal borrowing situations.

The Bill of Sale complements a Promissory Note for a Car by providing documented proof of the transfer of ownership from the seller to the buyer, often required in addition to proving the financial aspects of the transaction. While a Promissory Note outlines the terms under which the car is financed, a Bill of Sale confirms the transaction itself, detailing the item sold, sale date, and parties to the transaction. It serves as a receipt for the buyer and the seller.

A Vehicle Lease Agreement is akin to a Promissory Note for a Car, with the primary difference being that it pertains to renting a vehicle over a fixed period, not purchasing it. Both documents define terms such as the monthly payment amount and maintenance obligations, but a Lease Agreement also details terms regarding the return of the vehicle, mileage limits, and lease termination conditions.

An IOU (I Owe You) is a simple acknowledgment of debt much like a Promissory Note for a Car, which states that one party owes another a certain sum of money. However, IOUs are less formal and typically do not include detailed repayment terms, interest rates, or security interests in property. They serve as basic evidence of a debt's existence rather than a comprehensive lending agreement.

An Installment Agreement bears resemblance to a Promissory Note for a Car as it arranges for the repayment of a loan through regular payments over time. However, Installment Agreements can apply to any type of debt, not just car loans, and specify the installment amounts, due dates, interest rates, and the consequences of late or missed payments. It's a versatile document used for various debts beyond just vehicle financing.

A Guarantee Agreement is related in that it involves a third party agreeing to fulfill the obligations of a debtor in case of default, similar to how collateral might secure a Promissory Note for a Car. While a Promissory Note indicates the borrower’s promise to pay back the loan, a Guarantee Agreement provides an additional level of security for the lender, ensuring that the loan will be repaid either by the borrower or the guarantor.

A Security Agreement complements a Promissory Note for a Car by providing a legal framework that allows the lender to take possession of the collateral (the car) in the event of default. It outlines the process for repossession and sale of the collateral to recover the owed amount. Like a Promissory Note, it is a vital document in secured loans, detailing the rights concerning the secured asset, ensuring the lender has a means of recouping their loan if payments are not made.

When you're filling out a Promissory Note for a car, it’s essential to follow certain guidelines to ensure the document is valid and binding. A Promissory Note is a legal agreement in which one party promises to repay a debt to another party under specified conditions. Here are some do's and don'ts:

When discussing the Promissory Note for a car, several misconceptions often arise. Understanding these misconceptions is crucial for both buyers and sellers to manage their expectations and responsibilities accurately. Here's a clear rundown:

A Promissory Note is not legally binding. This is a common misunderstanding. In reality, a Promissory Note is a legally binding document once it is signed by both parties. It outlines the borrower's promise to pay back a debt under specified conditions.

It only outlines the repayment schedule. While the repayment schedule is a significant part of the Promissory Note, it also includes other essential details such as the interest rate, late fees, and the repercussions of failing to meet the agreed-upon payments.

Interest rates are not necessary. Some people believe that interest rates can be omitted from a Promissory Note for a car. However, including an interest rate is crucial as it compensates the lender for the risk of loaning the money and specifies the total amount the borrower owes over the loan term.

Verbal agreements can substitute for a written Promissory Note. Verbal agreements are challenging to enforce and prove in court. A written Promissory Note provides a clear, enforceable record of the loan's terms, protecting both the lender and the borrower's interests.

The borrower can’t negotiate the terms. Actually, before signing a Promissory Note for a car, both parties have the opportunity to negotiate the terms. This process can help adjust the repayment schedule, interest rate, and other conditions to make them manageable for the borrower and fair to the lender.

A Promissory Note is the same as a loan agreement. This misconception can lead to confusion. While both are debt instruments, a Promissory Note is usually a more straightforward document that specifies the borrower's promise to pay back a debt. A loan agreement is more comprehensive and typically involves detailed clauses regarding the obligations and protections of both parties.

A Promissory Note for a Car is a significant document that facilitates a smooth transaction and ensures agreement terms are clear and enforceable between parties. Whether you're buying or selling a car through private sale, understanding the implications and requirements for filling out and using a Promissory Note is essential. Here are ten key takeaways to keep in mind:

Using a Promissory Note when buying or selling a car through a private sale ensures that all financial aspects of the transaction are formally documented. This not only protects the interests of both parties but also lays down a structured repayment plan, making it easier to manage payments and uphold responsibilities. Always remember to review the terms of the Promissory Note thoroughly before signing to ensure that all parties have a clear understanding of their obligations.

Promissory Note Paid in Full Template - The Release of Promissory Note form is a simple yet powerful document that legally frees the borrower from the note's obligations.