Blank Promissory Note Template

Blank Promissory Note Template

A Promissory Note form is a vital document within the financial and legal landscapes, serving as a written agreement wherein one party, the maker, promises to pay a specified sum of money to another party, the payee. This form encapsulates several essential aspects, including the amount borrowed, the interest rate if applicable, repayment schedule, and the consequences of defaulting on the loan. Drafting a Promissory Note form requires meticulous attention to detail to ensure that all terms are clear, enforceable, and adhere to applicable state and federal laws, reflecting the nuances of the agreement between the parties involved. Its significance lies not only in its role in formalizing loans between individuals but also in its function in corporate finance, real estate transactions, and various other financial agreements. Understanding the components and legal implications of this form is crucial for both lenders and borrowers to safeguard their interests and foster a mutual understanding of the obligations agreed upon.

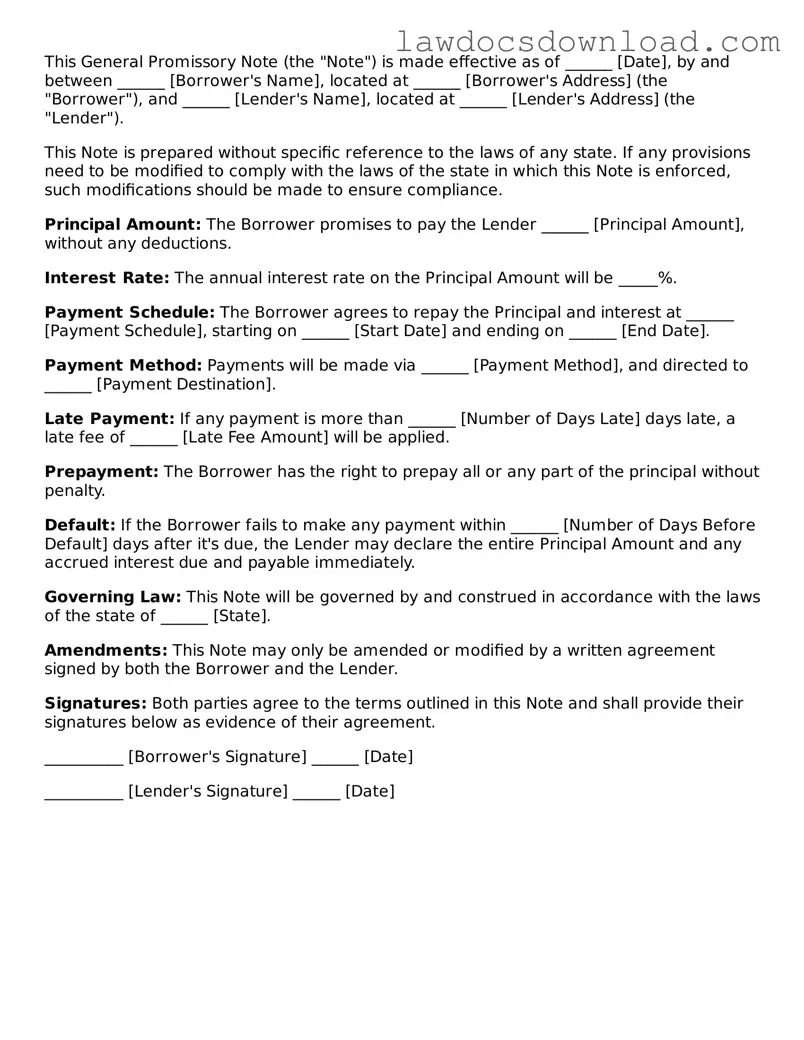

This General Promissory Note (the "Note") is made effective as of ______ [Date], by and between ______ [Borrower's Name], located at ______ [Borrower's Address] (the "Borrower"), and ______ [Lender's Name], located at ______ [Lender's Address] (the "Lender").

This Note is prepared without specific reference to the laws of any state. If any provisions need to be modified to comply with the laws of the state in which this Note is enforced, such modifications should be made to ensure compliance.

Principal Amount: The Borrower promises to pay the Lender ______ [Principal Amount], without any deductions.

Interest Rate: The annual interest rate on the Principal Amount will be _____%.

Payment Schedule: The Borrower agrees to repay the Principal and interest at ______ [Payment Schedule], starting on ______ [Start Date] and ending on ______ [End Date].

Payment Method: Payments will be made via ______ [Payment Method], and directed to ______ [Payment Destination].

Late Payment: If any payment is more than ______ [Number of Days Late] days late, a late fee of ______ [Late Fee Amount] will be applied.

Prepayment: The Borrower has the right to prepay all or any part of the principal without penalty.

Default: If the Borrower fails to make any payment within ______ [Number of Days Before Default] days after it's due, the Lender may declare the entire Principal Amount and any accrued interest due and payable immediately.

Governing Law: This Note will be governed by and construed in accordance with the laws of the state of ______ [State].

Amendments: This Note may only be amended or modified by a written agreement signed by both the Borrower and the Lender.

Signatures: Both parties agree to the terms outlined in this Note and shall provide their signatures below as evidence of their agreement.

__________ [Borrower's Signature] ______ [Date]

__________ [Lender's Signature] ______ [Date]

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specific sum of money to another party by a certain date. |

| Key Elements | Includes the amount borrowed, interest rate (if any), repayment schedule, and the final due date. |

| Secured vs. Unsecured | Can be "secured" with collateral or "unsecured," relying solely on the borrower's promise to pay. |

| Governing Laws | Subject to both federal laws and specific state laws where the note is executed. State laws vary significantly. |

| Usury Laws | Interest rates must comply with state-specific usury laws to prevent illegal high rates. |

| Consequences of Default | May result in legal action, seizure of collateral (if secured), and negative impact on borrower’s credit score. |

| Enforceability | Must be signed by the borrower and, in some cases, witnessed or notarized to be legally enforceable. |

After completing the Promissory Note form, the next step involves a formal review process. The note will be examined for any errors or missing information. Ensure all sections are filled out correctly and completely before submission. This document is crucial for outlining the terms of a loan between two parties. Therefore, accurate and clear completion is essential for a smooth agreement process.

To fill out the Promissory Note form correctly, follow these steps:

Once the form is fully completed and double-checked for accuracy, submit it to the necessary party or authority. Store a copy in a safe place for future reference. The form serves as a legal document binding both the borrower and the lender to the terms outlined within it, making its proper completion and submission crucial.

What exactly is a Promissory Note?

A Promissory Note is a written promise by one party, known as the borrower, to pay a certain sum of money to another party, the lender. This document outlines the loan's terms, including the principal amount, interest rate, repayment schedule, and any other conditions agreed upon by both parties. It serves as a legal record of the loan, ensuring both borrower and lender are clear on their obligations.

Is a Promissory Note legally binding?

Yes, a Promissory Note is a legally binding document. Once both parties have signed it, they are legally obligated to adhere to its terms. The lender is entitled to seek repayment as agreed, and the borrower is required to pay back the loan under the conditions outlined. Failure to meet these terms can result in legal consequences.

Who needs to sign the Promissory Note?

The Promissory Note must be signed by the borrower to be considered valid. Additionally, depending on the loan's circumstances and the requirements of the lender, a co-signer or guarantor might also need to sign it. Their signature implies that they agree to be responsible for the loan repayment if the primary borrower fails to pay.

What happens if the borrower does not repay the loan as agreed?

If the borrower does not make payments according to the agreed-upon terms, the lender has the right to seek repayment through legal means. This could involve taking the borrower to court to obtain a judgment against them or initiating collection actions. Depending on the terms of the Promissory Note and the laws of the state, the lender might also have the right to seize collateral if the loan is secured.

Can the terms of a Promissory Note be modified?

Yes, the terms of a Promissory Note can be modified, but any changes must be agreed upon by both the borrower and the lender in writing. The original note may be amended, or a new agreement may be created to reflect the changes. It’s important to document any modifications comprehensively to ensure both parties remain protected under the law.

Are there different types of Promissory Notes?

Yes, there are various types of Promissory Notes. They can be categorized based on their repayment structure, such as lump-sum, installment, or due on demand. Additionally, Promissory Notes can be secured, meaning the borrower provides collateral to guarantee repayment, or unsecured, where no collateral is provided. The specific type suitable for a transaction depends on the agreement between the borrower and lender.

How should a Promissory Note be stored?

After it is signed, the Promissory Note should be kept in a safe place by both the borrower and the lender. It's crucial to have this document readily available if there are any discrepancies or disputes about the loan terms or repayment. Ensuring the document is secure yet accessible to both parties involved can prevent future misunderstandings and protect the interests of everyone involved.

One common mistake people make when filling out a Promissory Note form is not specifying the exact terms of the repayment plan. It is crucial to detail whether payments will be made in installments or a lump sum, along with the due dates. Without clear repayment terms, misunderstandings can easily arise.

Another oversight is failing to include the interest rate or incorrectly calculating it. Interest rates should be explicitly stated to avoid future disputes. This rate must also comply with state laws to prevent the agreement from being considered usurious, which could make the promissory note unenforceable.

Often, individuals forget to clearly identify the parties involved by their full legal names. Using nicknames or incomplete names can lead to confusion about who is obligated to repay the loan. Accurate identification ensures there is no ambiguity regarding the parties' identities.

Not addressing what happens in the event of a default is a critical error. The note should outline the consequences if the borrower fails to make timely payments. Whether it includes late fees, acceleration of payment, or other remedies, these details help protect the lender’s interests.

Many fail to have the promissory note witnessed or notarized, thinking it unnecessary. While not always a legal requirement, having a witness or notarization can add an extra layer of authenticity and enforceability to the document.

Skipping the inclusion of a co-signer when needed is another mistake. If the borrower has questionable creditworthiness, a co-signer can provide additional security for the lender. Not considering this option may increase the lender’s risk.

A crucial detail often overlooked is defining the governing state laws. Promissory Notes are subject to state laws, and specifying which state’s laws govern the agreement can prevent legal uncertainties if disputes arise.

Some individuals make the error of not keeping the original document in a safe place. Losing the promissory note can complicate enforcement of the agreement. It’s important to treat it as a vital legal document and store it securely.

By skipping the step of reviewing the complete form before signing, people risk overlooking errors or omissions. A thorough review by all parties can catch mistakes that might otherwise lead to bigger issues down the line.

Last but not least, people often proceed without legal advice when dealing with complex loan situations. Consulting with an attorney can help ensure that the promissory note complies with all legal requirements and that the interests of both parties are adequately protected.

In the realm of financial agreements, a Promissory Note forms a pivotal document. It is a written promise by one party to pay another a definite sum of money either on demand or at a future date. Supporting and related documents often accompany this form to ensure a comprehensive and legally binding agreement. These documents vary based on the specifics of the transaction and the requirements of the involved parties.

Together, these documents create a legal framework that governs the loan transaction. Each plays a crucial role in defining the responsibilities and rights of the involved parties, ensuring the lender's security and the borrower's understanding of their obligations. Awareness and proper management of these documents are essential for the smooth execution of financial transactions.

The Loan Agreement shares common characteristics with a Promissory Note in that both outline loan terms, including repayment conditions and interest rates. However, a Loan Agreement is often more comprehensive, typically including detailed clauses on the obligations of both parties, default conditions, and legal recourse. This makes the agreement more suited for complex or larger loans where more protection for the involved parties is deemed necessary.

A Mortgage Agreement is similar to a Promissory Note in its function of outlining the borrower's promise to repay a loan used to purchase real estate. The primary difference lies in the Mortgage Agreement securing the loan through a legal claim on the property until the debt is fully paid. This document often includes terms about property insurance requirements, taxes, and maintenance obligations in addition to the repayment terms found in a Promissory Note.

The Deed of Trust, used in some states instead of a Mortgage Agreement, parallels the Promissory Note by binding the borrower to repay the loan under specified terms. However, it involves an additional party—a trustee—who holds the property's title until the loan is repaid. Functionally, it secures the loan by transferring legal title to the trustee, offering the lender protection similar to a mortgage but with some procedural differences in the event of default.

An IOU (I Owe You) document, while less formal and detailed than a Promissory Note, shares its fundamental characteristic of representing a debt owed. The IOU is a simple acknowledgment of the debt but typically lacks legally binding terms such as repayment schedules, interest rates, and security interests, making it more suitable for informal or small loans between individuals who trust each other.

A Line of Credit Agreement, like a Promissory Note, documents a borrower's promise to repay money drawn from a predetermined credit limit. But, it allows for the repeated withdrawal and repayment up to the credit limit over a period of time, offering more flexibility than the typically fixed loan amount and repayment schedule of a Promissory Note. This document frequently includes detailed terms on interest calculation, usage fees, and the conditions under which the credit line may be suspended or reduced.

The Student Loan Agreement bears similarities to a Promissory Note as it outlines the terms under which a student borrows money for education expenses and agrees to pay it back. It often includes specific provisions related to deferment, forbearance, and forgiveness that are unique to student loans. While both documents serve to bind the borrower to repay the loan, the Student Loan Agreement typically addresses the unique aspects of educational financing.

A Credit Card Agreement, though not directly related to a Promissory Note, involves a borrower agreeing to repay the lender for funds borrowed through credit card transactions. This agreement details interest rates, fees, penalties, and the repayment process but applies to revolving credit, where the borrower can make new charges up to a limit while paying off old balances. This contrasts with the more straightforward and fixed borrowing and repayment terms of a Promissory Note.

Finally, the Personal Guarantee is akin to a Promissory Note in that it secures a promise to repay. However, it is distinct in its purpose: a Personal Guarantee is signed by a third party, agreeing to repay the loan if the original borrower fails to do so. While a Promissory Note is a commitment between a borrower and a lender, a Personal Guarantee involves a third party to provide additional security to the lender, often used in conjunction with business loans to ensure repayment.

When filling out a Promissory Note form, it's crucial to ensure all information is accurate and clearly understood by all parties involved. Below are eight key dos and don'ts to guide you through the process:

When navigating the realm of financial agreements, promissory notes are common yet often misunderstood tools. These documents are crucial for formalizing the terms under which money is loaned and must be repaid. Let's clear up some common misconceptions:

All promissory notes are virtually the same. Contrary to this belief, promissory notes can vary greatly depending on the specifics of the loan, such as secured versus unsecured loans, interest rates, repayment schedules, and what occurs upon default. Tailoring a promissory note to the specific agreement is crucial.

Promissory notes are only for banks and financial institutions. This is not the case. Individuals can, and often do, use promissory notes for personal loans between family members or friends. This helps to clearly establish the repayment expectations and legally enforces the loan.

Verbal agreements are just as binding as a written promissory note. While oral contracts can be enforceable, the specificity and clarity provided by a written promissory note significantly reduce the risk of misunderstandings and disputes. Moreover, proving the terms of verbal agreements in court can be remarkably challenging.

You don't need a lawyer to draft a promissory note. While it's true that you can draft a promissory note without legal assistance, consulting with a professional can ensure that the document complies with state laws and adequately protects your interests. Small details can significantly affect the enforceability of the note.

Only the borrower needs to sign the promissory note. In reality, having all parties sign the promissory note—including co-signers if any—are present—strengthens the document's enforceability. Signatures confirm that everyone involved agrees to the terms outlined in the note.

Understanding the nuances of promissory notes can ensure that both lenders and borrowers are adequately protected. It's always advisable to thoroughly review the terms and, if possible, consult with a legal professional to navigate any complexities. Remember, a well-drafted promissory note can save a great deal of trouble in the long run.

When dealing with a Promissory Note, it's crucial to understand its purpose and the correct way to complete and utilize this legal document. A Promissory Note is a binding agreement between two parties, outlining a loan's terms and the repayment. Below are key takeaways to guide you through filling out and using a Promissory Note form:

Filling out and using a Promissory Note correctly is essential for both the lender and the borrower. It not only formalizes the loan agreement but also serves as a legal document that can be used in court if disagreements arise. Paying careful attention to the details and requirements of a Promissory Note will help ensure that both parties are protected throughout the duration of the loan.

Organization Meeting Minutes - An essential piece of documentation that aids in keeping meetings focused and productive, by providing a framework for reviewing decisions and action items.

Affidavit of Death Form California - The form helps in updating records with banks, loan providers, and government agencies, indicating that the named individual has died.