Legal North Carolina Promissory Note Form

Legal North Carolina Promissory Note Form

When individuals in North Carolina decide to enter into a borrowing arrangement, they often rely on a legal document known as the Promissory Note form to outline the terms of their agreement. This form serves as a crucial tool in ensuring clarity and enforceability of the financial understanding between the borrower and the lender. It meticulously details the amount borrowed, interest rates, repayment schedule, and the consequences of non-payment. Moreover, the form safeguards the interests of both parties involved, making clear the obligations and expectations. Importantly, it adheres to North Carolina’s specific legal standards, ensuring that the agreement is recognized under state law. This introduction to the North Carolina Promissory Note form highlights its significance in making borrowing clear and straightforward, while also pointing to the legal considerations integral to its effectiveness.

North Carolina Promissory Note

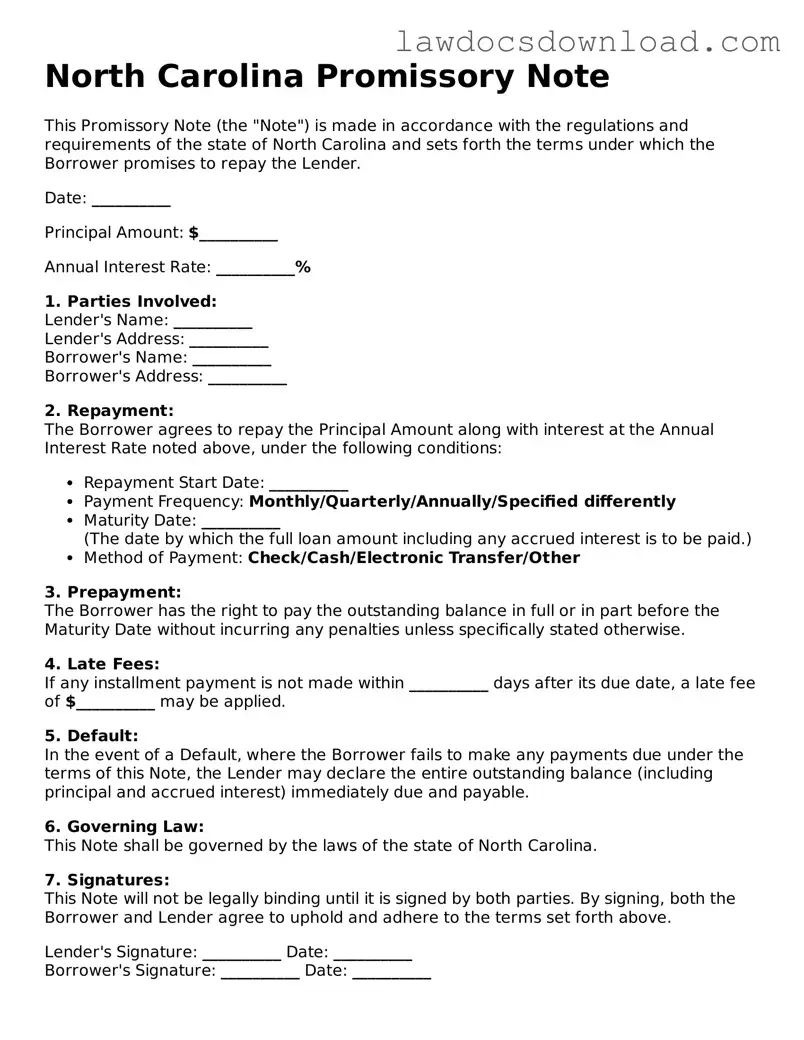

This Promissory Note (the "Note") is made in accordance with the regulations and requirements of the state of North Carolina and sets forth the terms under which the Borrower promises to repay the Lender.

Date: __________

Principal Amount: $__________

Annual Interest Rate: __________%

1. Parties Involved:

Lender's Name: __________

Lender's Address: __________

Borrower's Name: __________

Borrower's Address: __________

2. Repayment:

The Borrower agrees to repay the Principal Amount along with interest at the Annual Interest Rate noted above, under the following conditions:

3. Prepayment:

The Borrower has the right to pay the outstanding balance in full or in part before the Maturity Date without incurring any penalties unless specifically stated otherwise.

4. Late Fees:

If any installment payment is not made within __________ days after its due date, a late fee of $__________ may be applied.

5. Default:

In the event of a Default, where the Borrower fails to make any payments due under the terms of this Note, the Lender may declare the entire outstanding balance (including principal and accrued interest) immediately due and payable.

6. Governing Law:

This Note shall be governed by the laws of the state of North Carolina.

7. Signatures:

This Note will not be legally binding until it is signed by both parties. By signing, both the Borrower and Lender agree to uphold and adhere to the terms set forth above.

Lender's Signature: __________ Date: __________

Borrower's Signature: __________ Date: __________

| Fact Number | Detail |

|---|---|

| 1 | North Carolina promissory notes are legal agreements used for the borrowing and lending of money between two parties. |

| 2 | These forms must comply with North Carolina's statutes relating to interest rates and usury laws to be considered valid. |

| 3 | Under North Carolina law, the maximum interest rate a lender can charge on a personal loan without a written contract is 8% per annum. |

| 4 | For written agreements, North Carolina allows a maximum interest rate of 16% per annum. |

| 5 | North Carolina promissory notes can be classified as either secured or unsecured, depending on whether collateral is provided as security for the loan. |

| 6 | Secured promissory notes require the borrower to pledge assets as collateral, safeguarding the lender's investment. |

| 7 | Unsecured promissory notes do not involve collateral, presenting a higher risk to the lender. |

| 8 | Both parties should accurately document the loan amount, interest rate, repayment schedule, and any other relevant terms in the note. |

| 9 | For the promissory note to be enforceable in North Carolina, it must be signed by the borrower and, in some cases, witnessed or notarized. |

| 10 | In case of default, North Carolina law provides specific remedies which include accruing late fees, seeking full repayment, or pursuing legal action based on the terms of the promissory note. |

Filling out the North Carolina Promissory Note form is a straightforward process, but it's important to approach it with attention and care. This document is a binding agreement where one party promises to pay a specified sum to another. Completing this form accurately ensures clarity and legal protection for both the borrower and lender. Here are the steps needed to fill out the form correctly.

Once the form is completed and signed by both parties, it's essential to make copies for each party involved. This ensures that both the borrower and the lender have a record of the agreement for their files. Following these steps carefully will help establish a legally binding agreement that protects both parties' interests. Remember, it's always a good idea to consult with a legal professional if you have any questions or concerns while filling out the North Carolina Promissory Note form.

What exactly is a North Carolina Promissory Note form?

A North Carolina Promissory Note form is a legal document that outlines a loan agreement between a lender and a borrower. It specifies the amount of money loaned, the interest rate, repayment schedule, and other terms and conditions related to the loan. The form serves as a binding agreement, ensuring the borrower's promise to repay the lender under the agreed-upon terms, and it is governed by the laws of North Carolina.

Who needs to use a North Carolina Promissory Note form?

Anyone lending or borrowing a sum of money in North Carolina may need to use a Promissory Note form. This includes individuals lending to friends or family, businesses providing loans to customers, or transactions involving personal financing. Using a Promissory Note helps formalize the loan agreement and offers legal protection to both parties should disputes arise.

How can I ensure that a North Carolina Promissory Note is legally binding?

To ensure a North Carolina Promissory Note is legally binding, certain elements must be included: the names and addresses of both the lender and the borrower, the amount of money being loaned, the interest rate, and the repayment schedule. It’s also crucial that both parties sign the note. Additionally, having the signatures notarized can further strengthen the document's legal standing. Ensuring that the note complies with North Carolina's laws regarding loans and interest rates is equally important.

Can modifications be made to a Promissory Note after it has been signed in North Carolina?

Yes, modifications can be made to a Promissory Note after it has been signed, but any changes must be agreed upon by both the lender and the borrower. The best practice is to document these modifications in writing and have both parties sign off on any amendments. This documentation can prevent future disputes and will serve as evidence of the agreed-upon changes.

What happens if the borrower fails to repay the loan as agreed in the North Carolina Promissory Note?

If the borrower fails to repay the loan according to the agreed-upon terms in the Promissory Note, the lender has the right to take legal action to recover the owed amount. This may include filing a lawsuit against the borrower for breach of contract. In some cases, the note may include provisions for collateral, which the lender can claim in lieu of payment. It's advisable for lenders to consult with an attorney to explore their options and for borrowers to communicate openly with their lender to seek possible solutions or adjustments to the repayment terms.

In the process of drafting and completing a promissory note in North Carolina, individuals often make a variety of errors that can compromise the document's validity or enforceability. One common mistake is failing to clearly specify the terms of the loan. This includes not detailing the loan amount, interest rate, repayment schedule, and due date. Such omissions can lead to disputes and misunderstandings between the borrower and the lender.

Another frequent error is neglecting to include the legal names and addresses of both the borrower and the lender. This information is crucial for identifying the parties involved and can be particularly important if legal action is required to enforce the note. Without this information, the note may be considered incomplete or unenforceable.

Sometimes, people forget to specify the interest rate or, if they do, they set a rate that exceeds the legal limit in North Carolina. This can render the promissory note's interest terms unenforceable and, in some cases, might lead to penalties for charging usurious interest. It is crucial to adhere to state usury laws to avoid these pitfalls.

Moreover, parties often omit to outline the consequences of a default. This section is vital as it informs the borrower of the penalties for failing to make payments according to the agreed-upon schedule. Without clearly defined consequences, enforcing penalties or accelerating the loan repayment can become legally challenging.

A serious mistake made is not having the promissory note witnessed or notarized, as required for certain types of promissory notes in North Carolina. This oversight can affect the legal enforceability of the document, especially in cases where the document's authenticity is questioned.

Many borrowers and lenders do not consider the need to include a clause about what happens if the lender dies before the loan is fully repaid. This can create confusion and potential legal difficulties in determining how to proceed with the loan repayment, particularly in the absence of clear guidance.

Individuals sometimes neglect to define the governance of the note by North Carolina laws, which can lead to complications in the event of a dispute. Stating that the note is governed by the laws of North Carolina ensures that any legal interpretation or action taken on the note will be under the jurisdiction of North Carolina laws.

Another error is failing to provide a clear pathway for amending the terms of the note. Without this provision, any changes to the note require a new agreement, instead of an amendment, which can be cumbersome and lead to administrative difficulties.

Parties often overlook the importance of including a severability clause. This clause ensures that if one part of the note is found to be invalid, the rest of the agreement remains in effect. Without it, the entire note could be at risk of being declared unenforceable if challenged in court.

Lastly, not providing a copy of the signed promissory note to all parties involved is a common oversight. Each party should have a copy for their records to ensure that everyone has access to the agreed-upon terms and conditions, which can prevent future disputes and misunderstandings.

When entering into a financial agreement in North Carolina, particularly one involving a promissory note, there are several additional documents that are typically used to ensure that the agreement is comprehensively documented. These complementary forms help to protect the interests of all parties involved and provide a clearer framework for the financial transaction. Below is a list of documents often used alongside the North Carolina Promissory Note form.

These documents collectively create a structured and secure lending and borrowing environment. They can significantly reduce the risks involved by ensuring clarity and legal recourse for all parties. Individuals and entities are encouraged to consider the relevance and necessity of each document as they navigate through financial agreements in North Carolina.

A Mortgage Agreement is one document that shares similarities with the North Carolina Promissory Note form. Both documents are integral in the process of financing real estate purchases. While a promissory note serves as a borrower's promise to pay back a loan under agreed terms, the mortgage agreement secures the loan by using the property as collateral. This means that if the borrower fails to meet the terms of the note, the lender can enforce the mortgage agreement to reclaim the property.

The Loan Agreement is another document bearing resemblance to the North Carolina Promissory Note form. Both are legally binding contracts that detail the terms under which money has been lent and the obligations for repayment. However, a loan agreement typically provides more comprehensive details regarding the loan's conditions, including interest rates, repayment schedule, and consequences of default, making it broader in scope than a promissory note, which focuses more narrowly on the repayment promise.

The IOU (I Owe You) document also shares characteristics with the North Carolina Promissory Note. Both serve as acknowledgments of debt. However, the promissory note is more formal and includes specific repayment terms, such as payment amounts and due dates, making it more enforceable than an IOU, which is a more informal acknowledgment that a debt exists without detailing the repayment plan.

A Personal Guarantee is related to the Promissory Note form in that it involves a promise regarding payment. While a promissory note is a promise by a borrower to pay back a loan, a personal guarantee is a promise by a third party to repay the loan if the original borrower fails to do so. This provides an additional level of security to the lender that the loan will be repaid.

A Debt Settlement Agreement shares a purpose with the North Carolina Promissory Note in terms of addressing debts. It is typically used when a debtor is unable to pay back the original amount as agreed and the parties negotiate a lesser amount to be paid. While the promissory note outlines the terms of repayment from the beginning, a debt settlement agreement comes into play when those original terms cannot be met.

An Installment Agreement, much like the Promissory Note, outlines a repayment plan for a debt. This document is specifically tailored to situations where repayments are to be made in parts over time. Though both documents set forth a schedule for repayment, an installment agreement may be entered into after an initial promise to pay (like in a promissory note) cannot be adhered to as originally planned.

A Security Agreement has a connection to the Promissory Note form through its role in securing a loan. This document gives the lender a security interest in a specific asset or property of the borrower, serving as collateral for the loan. While the promissory note signifies the borrower’s intention to repay the loan, a security agreement provides the lender with a means to recover their funds if the borrower defaults.

The Credit Agreement shares its foundational concept with the Promissory Note: both involve the extension of credit from one party to another under defined conditions. Credit agreements, however, are often more complex and encompass not only the repayment plan but also the revolving nature of the credit, fees, covenants, and other detailed provisions not typically specified in a promissory note.

A Student Loan Agreement is particularly similar to a Promissory Note issued for educational purposes. It outlines the borrower’s commitment to repay borrowed funds used for education, including details on interest rates, deferment options, and repayment schedules. While both documents signify an agreement to repay a loan, student loan agreements often include specific provisions related to the educational nature of the loan, which are not found in general promissory notes.

Lastly, a Mortgage Note resembles the North Carolina Promissory Note form closely because it is a specific type of promissory note used in real estate transactions. It not only evidences the borrower’s promise to repay the loan but also includes details specific to mortgage loans, such as escrow arrangements for taxes and insurance. While all mortgage notes are promissory notes, not all promissory notes are mortgage notes, making their relationship particularly direct.

Filling out a promissory note in North Carolina requires attention to detail and a clear understanding of the obligations being documented. Here are some do's and don'ts to consider:

Do's:

Include full names and addresses of both the borrower and the lender to clearly identify the parties involved.

Specify the loan amount in words and figures to avoid any misinterpretation of the financial terms.

Clearly outline the repayment schedule, including due dates and amounts, to set clear expectations for repayment.

State the interest rate explicitly, ensuring it complies with North Carolina's legal limits to avoid issues of usury.

Include a clause regarding late fees and the grace period to manage late payments effectively.

Detail the collateral securing the loan, if any, to highlight the secured nature of the agreement.

Sign and date the document in the presence of a witness or notary to certify its authenticity and enforceability.

Don'ts:

Ignore state regulations regarding interest rates and loan agreements to avoid legal repercussions.

Omit any essential details such as the loan amount, repayment terms, or interest rates, as this could make the note ambiguous.

Forget to include consequences for non-payment or late payments, which are crucial for protecting the lender's rights.

Leave spaces blank that could be filled in later, as this could lead to fraudulent changes after signing.

Rely on verbal agreements to supplement the promissory note; instead, include all relevant details in the document.

Skip the step of having a witness or notary present during the signing, as their endorsement can add legal weight to the document.

Fail to provide each party with a copy of the signed promissory note, ensuring that all involved have a record of the agreement.

In discussing the North Carolina Promissory Note form, several misconceptions often arise. These misunderstandings can lead to confusion, potentially resulting in legal or financial missteps. Let's clarify some of these common misconceptions to ensure a stronger grasp of the document's usage and significance.

It's just a casual IOU. A common misconception about the North Carolina Promissory Note form is that it's an informal document, akin to an IOU. Contrary to this belief, it is a legally binding agreement that formalizes the terms of a loan between two parties. It outlines the borrower's promise to repay the lender according to the specified terms and conditions.

Only the borrower needs to understand it. It's often thought that only the borrower needs to fully grasp the contents of the Promissory Note. However, both parties—the lender and the borrower—must thoroughly understand the agreement. This mutual understanding ensures that both parties are aware of their obligations and rights under the note.

Legal assistance isn't necessary. Many assume that creating a Promissory Note doesn't require legal guidance. While it's possible to draft one without a lawyer, consulting a legal professional can help ensure that the document complies with North Carolina laws and addresses all necessary legal intricacies.

It doesn't need to be notarized. While not all Promissory Notes require notarization, having the document notarized in North Carolina can strengthen its legality and enforceability. Notarization formally verifies the identities of the signing parties, adding an extra layer of legitimacy.

All Promissory Notes are the same. Another misconception is the belief that all Promissory Notes are identical. In reality, each agreement can be customized to fit the specific terms of a loan, including interest rates, repayment schedules, and any collateral involved. The flexibility of the document allows it to cater to the unique needs of the parties involved.

A Promissory Note is only for financial institutions. It's often thought that only banks or financial institutions can issue Promissory Notes. However, individuals can also create and utilize these documents for personal loans. This flexibility makes it a valuable tool for a range of financial transactions beyond traditional lending institutions.

No legal consequences if not followed. A dangerous misconception is that failing to adhere to the terms of the Promissory Note carries no legal repercussions. On the contrary, breaching the agreement can lead to significant legal and financial consequences. The lender has the right to pursue legal action to enforce the note, which could include requiring payment in full or seizing collateral.

Understanding the true nature and function of the North Carolina Promissory Note form is crucial for anyone engaging in lending or borrowing. Dispelling these misconceptions helps in appreciating its importance as a tool for securing loans and ensuring clear, enforceable terms between parties.

Understanding the Purpose: The North Carolina Promissory Note form is a legal document that outlines the details of a loan agreement between a borrower and a lender. It's crucial for both parties to accurately complete this form to ensure clear communication and understanding of the loan terms.

Personal Information Is Key: Always fill in comprehensive personal information for both the lender and the borrower. This includes full names, addresses, and contact details. Clear identification can prevent misunderstandings and ensure that both parties are easily reachable.

Loan Amount and Interest Rate: Specify the loan amount in clear numeric and written form to avoid any discrepancies. The agreed-upon interest rate should also be included, adhering to North Carolina's legal limits to maintain the form's enforceability.

Repayment Schedule: The form should detail the repayment plan. Whether it’s a lump sum, due on demand, or in installments, clarity on this front helps in setting expectations and avoiding future conflicts.

Collateral: If the loan is secured, the promissory note must describe the collateral that secures the loan. This information provides legal recourse for the lender should the borrower fail to meet the repayment terms.

Signatures: The document isn’t legally binding until it's signed by both the borrower and the lender. Witnesses or a notary public may also be required to sign, depending on the specifics of the transaction and local legal requirements.

Understanding Legal Remedies: Both parties should be aware of the legal actions that the lender can take if the borrower fails to repay the loan as agreed. Knowledge and agreement on these terms can prevent surprises and ensure preparedness for any outcome.

Georgia Promissory Note - Critical for ensuring clarity and legality in loan agreements, it prevents misunderstandings and disputes between the involved parties.

Does Promissory Note Need to Be Notarized - In real estate transactions, a promissory note can be used in conjunction with a mortgage agreement to outline the loan details.