Legal New York Promissory Note Form

Legal New York Promissory Note Form

In the bustling corridors of financial transactions and personal loans within New York State, the Promissory Note form stands out as a cornerstone document, ensuring clarity and security for both lenders and borrowers. This crucial piece of paperwork operates as a legal agreement, meticulously documenting the amount of money borrowed, the repayment schedule, interest rates, and what happens if the terms aren't met. Its significance cannot be overstated—providing a solid foundation for personal and business finances by binding the borrower to their commitment to repay the loan under the agreed conditions. The form encapsulates a variety of types, each tailored to specific lending scenarios, such as secured and unsecured loans, thereby offering a broad spectrum of applications from straightforward personal loans to more complex commercial lending arrangements. It effectively bridges the trust gap between parties, serving as a legally enforceable reminder of the borrower's obligations and the lender's rights. By understanding the ins and outs of the New York Promissory Note form, individuals and entities can navigate their financial dealings with greater confidence and legal backing, ensuring that all parties are protected throughout the course of the loan.

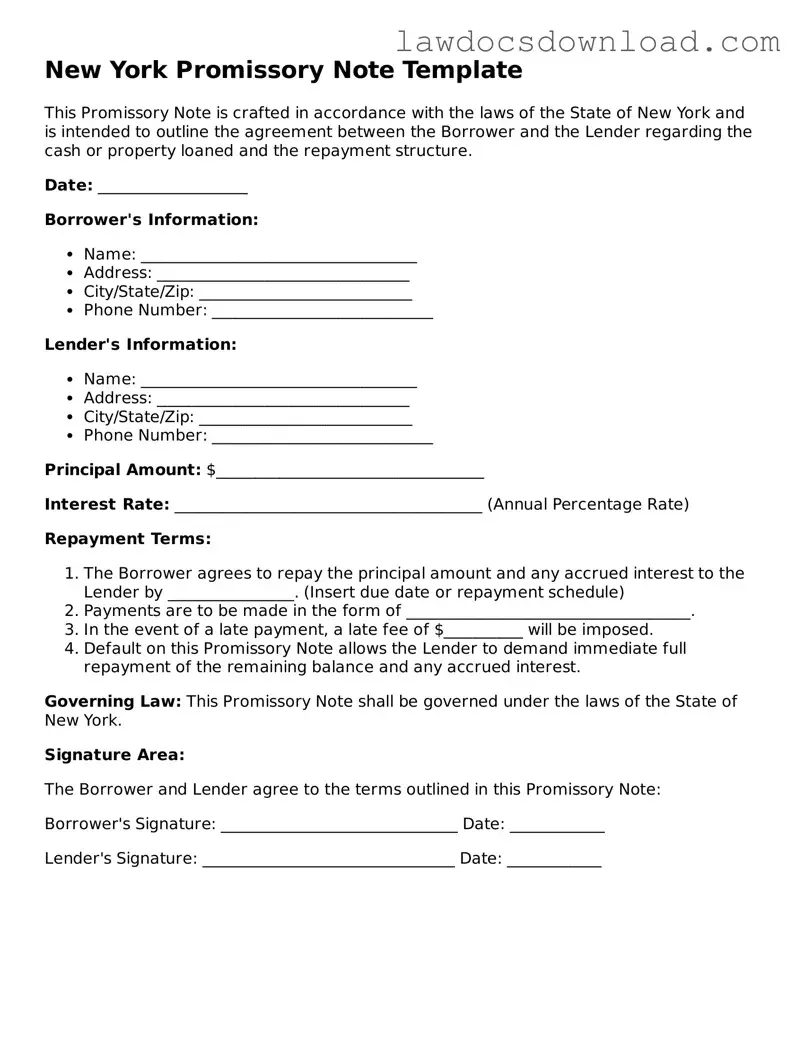

New York Promissory Note Template

This Promissory Note is crafted in accordance with the laws of the State of New York and is intended to outline the agreement between the Borrower and the Lender regarding the cash or property loaned and the repayment structure.

Date: ___________________

Borrower's Information:

Lender's Information:

Principal Amount: $__________________________________

Interest Rate: _______________________________________ (Annual Percentage Rate)

Repayment Terms:

Governing Law: This Promissory Note shall be governed under the laws of the State of New York.

Signature Area:

The Borrower and Lender agree to the terms outlined in this Promissory Note:

Borrower's Signature: ______________________________ Date: ____________

Lender's Signature: ________________________________ Date: ____________

| Fact | Description |

|---|---|

| 1. Definition | A New York Promissory Note is a legal agreement involving a monetary loan that is to be paid back under specified conditions between two parties, the lender and borrower. |

| 2. Governing Law | This form is governed by the laws of the state of New York, including the New York General Obligations Law. |

| 3. Types | There are two main types: secured and unsecured. A secured note requires collateral, whereas an unsecured note does not. |

| 4. Interest Rate | Under New York law, the maximum interest rate on a personal loan must not exceed 16% per annum to avoid usury violation. |

| 5. Co-signer | A co-signer can be included in the promissory note, adding an additional layer of security for the repayment of the loan. |

| 6. Repayment Schedule | The note must clearly outline the repayment schedule, including the start date, amount of each payment, and the frequency of payments. |

| 7. Late Fees | The agreement can include provisions for late fees, but they must be considered reasonable under New York law. |

| 8. Default Terms | Terms of default should be specified, detailing the consequences if the borrower fails to meet the repayment terms. |

| 9. Prepayment | Conditions for prepayment can be included, often specifying if there are any penalties for early repayment of the loan. |

Getting ready to fill out the New York Promissory Note form might seem daunting, but it's an important step in formalizing a loan agreement between two parties. This document is crucial as it clearly lays out the repayment plan, interest rate, and terms, thereby protecting both the lender and the borrower's interests. It’s vital to approach this task with attention to detail to ensure that every part of the agreement is correctly documented. The following steps will guide you through completing the form accurately.

Once the New York Promissory Note form is filled out and signed by both parties, each should keep a copy for their records. This document will serve as a legally binding agreement, ensuring that both the lender and borrower are protected and clear on the terms of the loan. Paying careful attention during the completion process will help prevent misunderstandings and disagreements in the future.

What is a New York Promissory Note?

A New York Promissory Note is a legal document that records a loan agreement between two parties: the borrower and the lender. It specifies the amount of money borrowed, the interest rate if applicable, repayment schedule, and other terms regarding the loan's repayment. It's essential for both personal and business loans within New York State to ensure there's a clear understanding and record of the loan.

Are there different types of Promissory Notes in New York?

Yes, in New York, there are typically two main types of Promissory Notes: secured and unsecured.

How can a New York Promissory Note be enforced if the borrower fails to repay?

Enforcing a Promissory Note in New York requires legal action. If a borrower fails to repay according to the terms of the note, the lender may file a lawsuit to recover the owed amount. For a secured note, this process might involve seizing the collateral. In contrast, an unsecured note may lead to a court judgment against the borrower, allowing the lender to pursue other assets or means of recovery. It's crucial for lenders to maintain accurate records of all payments and communications in case enforcement becomes necessary.

Does a New York Promissory Note need to be notarized or witnessed to be valid?

While notarization is not a requirement for a New York Promissory Note to be considered valid, it is strongly recommended. Notarization can provide an additional layer of authentication, making it easier to enforce the note if there's a dispute or if legal action becomes necessary. Similarly, having witnesses can also add credibility to the document, although, like notarization, it is not a legal requirement. Ensuring these steps can be crucial in safeguarding the interests of both the lender and the borrower.

One common mistake made during the completion of the New York Promissory Note form is neglecting to provide detailed borrower information. Proper identification of both parties involved is crucial. The inclusion of full legal names, addresses, and, if applicable, identification numbers, establishes the credibility of the document and the identity of the debtor and creditor. This oversight can lead to ambiguity, making the note less enforceable in legal proceedings.

Another error is not specifying the loan amount in clear, unambiguous terms. It is vital to state the principal amount being borrowed in both numeric and written form to prevent any disputes about the loan's size. This clarity helps in avoiding any misunderstandings or potential legal disputes over the amount owed.

Failure to define the repayment schedule is a significant mistake. A detailed repayment plan, including the due dates and whether the payments are monthly or at another frequency, ensures both parties have clear expectations. Without this information, enforcing the agreement's terms or protecting oneself against default becomes challenging.

Inaccurately setting or omitting the interest rate is a critical error. New York State has specific laws governing the maximum allowable interest rate. If the interest rate on the note exceeds this limit, it could be considered usurious, rendering the note unenforceable and illegal. It's essential to check current regulations to ensure compliance.

Many forget to include provisions for late fees and penalties for missed payments. Specifying these terms acts as a deterrent against late payments and compensates the lender for the inconvenience of delayed payment. Omitting these terms can lead to difficulties in managing late payments effectively.

Lastly, neglecting to have the note witnessed or notarized is a common oversight. While not always a legal requirement, having impartial parties witness or notarize the document can add an extra layer of verification and enforceability. This step can prove invaluable, especially in disputes where the authenticity of signatures might be questioned.

When navigating the complexities of financial agreements in New York, a Promissory Note often plays a critical role in documenting the terms of a loan between two parties. However, to ensure a comprehensive and legally sound agreement, several additional forms and documents may be utilized alongside the Promissory Note. These documents serve to protect the interests of both the lender and the borrower, providing further legal clarity and securing the agreement against potential disputes or misunderstandings.

Together, these documents create a robust framework that facilitates clear communication, reduces legal risks, and ensures that both parties' rights and obligations are clearly defined and protected throughout the life of the loan. Proper use of these documents not only streamlines the lending process but also provides a level of security and peace of mind for everyone involved.

The New York Promissory Note Form is closely related to a Loan Agreement, primarily because both are binding documents between a lender and a borrower concerning the borrowing of money. The distinction lies in their complexity and details; while a promissory note is a straightforward promise to pay back a sum of money under agreed terms, a loan agreement usually contains more detailed clauses regarding the obligations of both parties, collateral arrangement, and actions in the case of a default.

Similarly, an IOU (I Owe You) document echoes the simplicity of a promissory note but is even less formal. An IOU merely states the amount owed and to whom, without detailing the repayment schedule or interest rates, making it less enforceable than a promissory note. It’s an acknowledgment of debt but doesn’t bind the borrower to terms as strictly as a promissory note does.

Mortgage agreements also share similarities with promissory notes, as they both involve borrowing and lending practices. However, a mortgage specifies borrowing to finance real estate purchases, with the property itself serving as collateral for the loan. While the promissory note secures the promise to repay, the mortgage agreement contains specific details on the property involved and what happens if the borrower fails to make payments.

A Bond is another form that resembles a promissory note by representing a loan between an issuer and an investor, but it typically pertains to corporate or governmental borrowing. Bonds include terms regarding the loan's interest rate and maturity date but are designed for public investment rather than private loans between individuals.

A Line of Credit Agreement, while serving a different financial function, shares the notion of borrowing under specific conditions. Unlike the one-time loan of a promissory note, a line of credit agreement offers the borrower access to a set amount of funds to draw from as needed, detailing the terms under which this money can be borrowed and repaid over time.

A Student Loan Agreement is a specialized type of promissory note targeting educational funding. It outlines the terms under which a student borrows money for tuition and other expenses, including interest rates and repayment schedules. The focus on educational finance and the inclusion of particular deferment and forgiveness options distinguishes it from general promissory notes.

Installment Agreements, akin to promissory notes, involve the borrower agreeing to repay a sum in scheduled payments. However, they are more commonly used for transactions involving goods or services rather than loans of cash. These agreements detail the amount to be paid in each installment, any interest charged, and what happens in case of late or missed payments.

A Security Agreement complements a promissory note when a loan involves collateral. This legal document outlines the specifics of the property or asset pledged as security for the loan, ensuring the lender can take possession if the borrower defaults. While a promissory note signifies the promise to repay, the security agreement protects the lender's interest in the pledged collateral.

Filling out a New York Promissory Note form requires attention to detail and understanding the importance of accuracy. Below are essential do's and don'ts to guide you through the process effectively.

Do's:

Don'ts:

When it comes to the New York Promissory Note form, misunderstandings are common. Let's clarify some of these misconceptions to ensure individuals are well-informed and can navigate their financial agreements with more confidence.

It's just a casual agreement. Many believe a promissory note is a casual, informal agreement, akin to an IOU. However, in New York, it's a legally binding document that obligates the borrower to repay the loan under the terms specified.

No legal standards apply. Contrary to this belief, New York promissory notes must adhere to state laws, including interest rate caps and other regulations, making it critical to understand these rules when drafting or signing a note.

One size fits all. People often think that a standard form can be used for all promissory notes in New York. In reality, the terms can and should be tailored to the specific loan agreement, including repayment schedules, interest rates, and any collateral involved.

Not necessary between friends or family. The misconception here is that promissory notes are unnecessary for loans between close relationships. However, documenting the loan in this way helps prevent misunderstandings and legal disputes in the future.

Signing without a witness is okay. While not always legally required, having a witness or notary sign the promissory note can add a layer of validity and protection for both parties involved.

No need for specifics. A vague agreement might seem sufficient, but a promissory note should clearly outline all the loan's terms. This includes repayment dates, interest rates, and what happens in case of default.

Electronic signatures aren't valid. This is false. In the digital age, electronic signatures are recognized and can be just as legally binding as traditional signatures on a promissory note in New York.

It can't be modified. Many assume once a promissory note is signed, the terms are set in stone. However, if both the lender and borrower agree, the terms can indeed be modified.

Only banks can issue them. This is a common misconception. Any individual or entity can issue a promissory note as long as it complies with New York's legal requirements.

It guarantees payment. Unfortunately, while a promissory note legally binds the borrower to repay the loan, it does not absolutely guarantee that the lender will be paid back. Lenders may still need to take legal action to enforce the document in case of default.

Understanding these misconceptions is crucial for anyone involved in lending or borrowing money in New York. Being well-informed about the specifics of promissory notes helps ensure that these financial transactions are conducted smoothly and with fewer disputes.

When it comes to creating a Promissory Note in New York, knowing the essentials can make the process smoother and ensure all legal bases are covered. Here are four key takeaways to keep in mind:

By keeping these key points in mind, you can ensure that your promissory note is not only legally compliant but also clear and understandable for all parties involved.

Create a Promissory Note - It serves as a legal record of a loan, assisting in the prevention of misunderstandings or disputes over the terms agreed upon.

Loan Note Template - A financial commitment documented in writing ensuring the repayment of a loan to a lender, laying out repayment schedules, interest rates, and other relevant terms.

Texas Promissory Note Template - The promissory note is legally binding, making it enforceable in a court of law should the borrower fail to meet the agreed-upon terms.