Legal New York Loan Agreement Form

Legal New York Loan Agreement Form

In the financial heart of the United States, New York, loan agreements are foundational documents that solidify the terms under which money is borrowed and paid back. Such agreements are instrumental in both personal and commercial finance realms, guiding the interactions between lenders and borrowers with precision and legal enforceability. They meticulously outline the loan amount, repayment schedule, interest rates, and the consequences of default, providing clear expectations and responsibilities for all parties involved. Furthermore, these forms serve as a protective mechanism, ensuring that lenders can recoup their investments and borrowers are shielded from unfair practices. Within the context of New York's robust legal framework, these documents are tailored to meet stringent state-specific requirements, addressing various legal considerations to ensure compliance and fairness. As instruments of financial engagement, New York Loan Agreement forms are essential for fostering trust, transparency, and stability in monetary transactions, effectively fueling both individual pursuits and the broader economic growth.

New York Loan Agreement Template

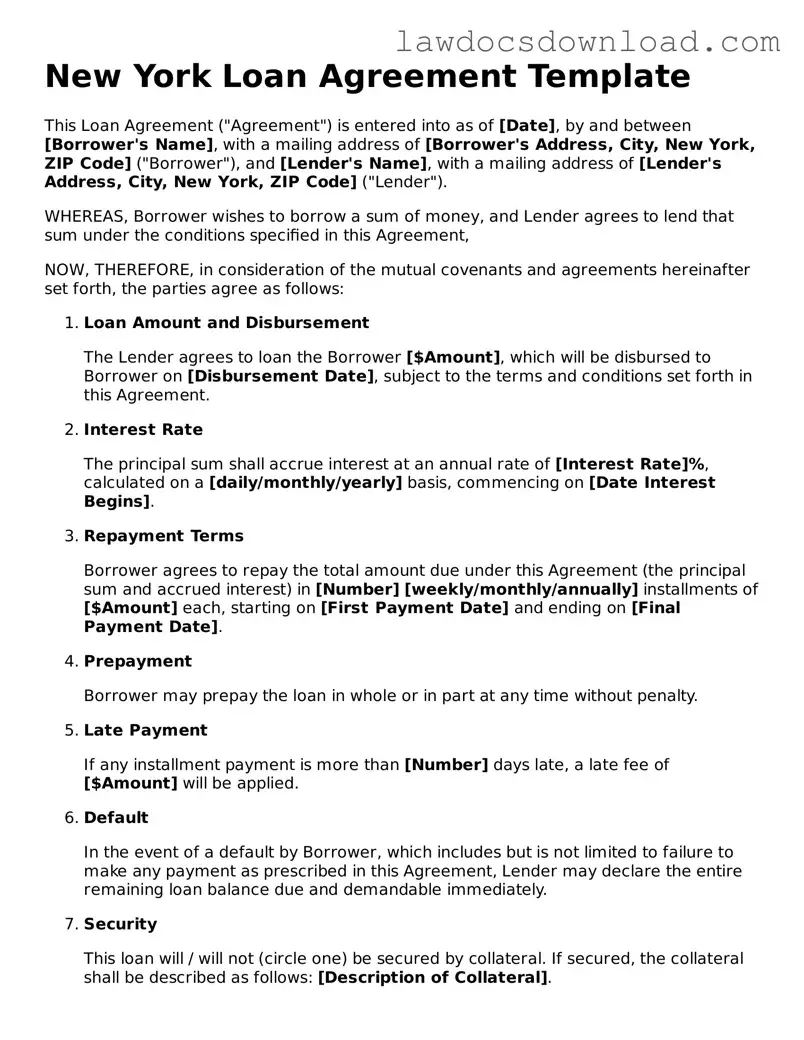

This Loan Agreement ("Agreement") is entered into as of [Date], by and between [Borrower's Name], with a mailing address of [Borrower's Address, City, New York, ZIP Code] ("Borrower"), and [Lender's Name], with a mailing address of [Lender's Address, City, New York, ZIP Code] ("Lender").

WHEREAS, Borrower wishes to borrow a sum of money, and Lender agrees to lend that sum under the conditions specified in this Agreement,

NOW, THEREFORE, in consideration of the mutual covenants and agreements hereinafter set forth, the parties agree as follows:

The Lender agrees to loan the Borrower [$Amount], which will be disbursed to Borrower on [Disbursement Date], subject to the terms and conditions set forth in this Agreement.

The principal sum shall accrue interest at an annual rate of [Interest Rate]%, calculated on a [daily/monthly/yearly] basis, commencing on [Date Interest Begins].

Borrower agrees to repay the total amount due under this Agreement (the principal sum and accrued interest) in [Number] [weekly/monthly/annually] installments of [$Amount] each, starting on [First Payment Date] and ending on [Final Payment Date].

Borrower may prepay the loan in whole or in part at any time without penalty.

If any installment payment is more than [Number] days late, a late fee of [$Amount] will be applied.

In the event of a default by Borrower, which includes but is not limited to failure to make any payment as prescribed in this Agreement, Lender may declare the entire remaining loan balance due and demandable immediately.

This loan will / will not (circle one) be secured by collateral. If secured, the collateral shall be described as follows: [Description of Collateral].

This Agreement shall be governed by and construed in accordance with the laws of the State of New York, without giving effect to any choice or conflict of law provision or rule.

Any amendment to this Agreement must be in writing and signed by both parties.

If any part of this Agreement is held unenforceable, the remainder of the Agreement will still be in effect.

IN WITNESS WHEREOF, the parties hereto have executed this Agreement as of the first date written above.

_______________________

[Borrower's Name and Signature]

_______________________

[Lender's Name and Signature]

| Fact Number | Detail |

|---|---|

| 1 | The New York Loan Agreement form is governed by the laws of the State of New York. |

| 2 | It is necessary for the agreement to be in writing to be enforceable for loans exceeding a certain amount, as per New York's Statute of Frauds. |

| 3 | Interest rates on loans provided under this agreement cannot exceed the maximum rate allowed by New York usury laws. |

| 4 | The agreement must clearly identify the parties involved, namely the borrower and the lender. |

| 5 | Details of the loan amount, interest rate, repayment schedule, and maturity date must be explicitly stated. |

| 6 | Collateral securing the loan, if any, must be described in detail within the agreement. |

| 7 | A default clause is included, outlining conditions and consequences of non-compliance by the borrower. |

| 8 | Provisions regarding amendment, waiver, or any changes to the agreement must be clearly stated. |

| 9 | The agreement can include a prepayment clause, allowing the borrower to pay the loan off early without penalty, depending on the terms. |

| 10 | Governing law and jurisdiction clauses ensure that any disputes under the agreement will be resolved under New York law and in its courts. |

Filling out the New York Loan Agreement form is a crucial step in formalizing the terms under which money is borrowed and will be paid back. This process ensures that both the lender and the borrower have a clear understanding of the obligations involved. The document outlines the amount of the loan, the interest rate, repayment schedule, and any other conditions that both parties have agreed upon. To complete this form accurately, follow the steps listed below. By doing so, you'll help protect both parties' interests and ensure a smoother transaction.

After completing these steps, it’s important for both parties to keep a copy of the signed agreement. This document serves as a legal record of the loan and can be crucial in resolving any future disputes. Furthermore, the borrower should start planning for the repayment according to the schedule agreed upon, and both parties should communicate openly about any issues that may arise during the term of the loan.

What is a Loan Agreement form?

A Loan Agreement form is a legal document that outlines the terms and conditions under which a loan is provided. It includes information such as the amount of the loan, repayment schedule, interest rate, and the obligations of both the borrower and the lender. This form serves as a binding agreement to ensure both parties fulfill their commitments related to the loan.

Who needs to sign the New York Loan Agreement form?

The New York Loan Agreement form must be signed by both the borrower and the lender. In some cases, if a guarantor is involved in securing the loan, they also need to sign the agreement. Witnesses or a notary public may also be required to sign, depending on the amount of the loan and the specific requirements set forth by New York State law.

Is a witness or notary required for the form in New York?

While not always mandatory, having a witness or notary public sign the loan agreement can add a layer of legality and enforceability. For larger loan amounts or more formalized lending, it's advisable to have the document notarized to deter any disputes over the validity of the signatures.

Can I customize the New York Loan Agreement form?

Yes, the Loan Agreement form can and should be customized to match the specific terms agreed upon by the borrower and lender. This includes details such as repayment schedule, interest rates, collateral (if any), and any other special conditions. Customization helps ensure that the agreement accurately reflects the understanding between the parties.

What happens if a payment is missed?

In the event that a payment is missed, the terms outlined in the Loan Agreement form dictate the consequences. Typically, there may be a grace period followed by penalties, which can include late fees or higher interest rates. Continual failure to meet payment obligations could result in the lender taking legal action to recover the owed amount.

Can the loan be paid off early?

Whether the loan can be paid off early depends on the terms outlined in the Loan Agreement form. Some agreements may allow for early repayment without penalty, while others may impose fees for early settlement. It’s crucial to review the terms related to early repayment before finalizing the agreement.

What should be done if the borrower or lender wishes to modify the agreement?

If either the borrower or the lender wants to modify the agreement, both parties should discuss and agree upon the new terms. Any changes should be made in writing, and an amendment to the original Loan Agreement form should be signed by both parties. This ensures that the modifications are legally binding.

Is the New York Loan Agreement form legally binding across the United States?

While the New York Loan Agreement form is designed to comply with New York State laws, its enforceability in other states may vary. When a loan agreement involves parties in different states, it's important to ensure that the agreement adheres to the legal requirements of both the lender's and borrower's states. Seeking legal advice to make sure the agreement is enforceable across state lines is advisable.

Filling out the New York Loan Agreement form can often be a daunting task. Many tend to overlook the importance of reading through every clause which leads to common mistakes. First among these errors is not specifying the loan amount in clear terms. This fundamental step is crucial as it sets the financial parameters of the agreement. Without a clear, written amount, disputes can easily arise regarding the expectations of both parties involved.

Another frequent oversight is neglecting to detail the repayment schedule. The agreement should clearly outline when payments are due, the amount of each payment, and over what period. Failing to define these parameters can lead to confusion and potential legal issues between the lender and borrower.

Interest rates are often another source of confusion. The contract should specify whether the interest rate is fixed or variable. Without this specification, the borrower may face unexpected changes in their payment amounts. Furthermore, it's essential to ensure that the agreed-upon interest rates comply with New York’s usury laws to avoid voiding the agreement.

Ignoring the need to outline the conditions for default is also a common mistake. A comprehensive agreement should include what constitutes a default, such as missed payments or bankruptcy, and what actions the lender can take. Not having these conditions clearly stated can limit the lender's options for recourse under New York law.

Failing to include clauses about amendment procedures is another oversight. There should be a clear process for how the agreement can be modified, requiring mutual consent from both parties. Without this, altering the agreement can become cumbersome and contentious.

Omitting the governing law section is not advisable. This part of the agreement specifies that New York law governs the contract. It's essential for ensuring that any legal disputes are handled within the familiar jurisdiction and according to New York laws, providing predictability and security for both parties.

Finally, both parties often forget to officially execute the agreement by signing and dating. This formal step is vital as it signifies the consent of both parties to the terms and conditions laid out in the document. An unsigned agreement is typically not enforceable in a court of law, making it nearly impossible to seek remedy or enforcement.

When entering into a loan agreement in New York, several additional forms and documents often accompany the main contract to ensure all aspects of the transaction are legally covered and clearly understood by all parties involved. These documents serve various purposes, such as providing security, outlining terms of the agreement, and ensuring compliance with state laws. Below is a list of documents commonly used alongside the New York Loan Agreement form, each briefly described to highlight its importance and function in the loan process.

Proper preparation and understanding of these documents are crucial in any loan transaction. They not only provide legal protection but also ensure clarity and fairness in the financial agreement. Both lenders and borrowers should review these documents carefully to ensure they fully understand the commitments they are making. Partnering with professionals to prepare and review these documents can also provide valuable peace of mind throughout the lending process.

The New York Loan Agreement form closely resembles a Promissory Note. Both documents are binding and detail the terms under which money is borrowed and must be repaid. Where they align is in their primary purpose: to clearly outline the loan amount, interest rate, repayment schedule, and the consequences of default. However, a Loan Agreement typically encompasses more comprehensive terms and conditions, including confidentiality clauses and dispute resolution mechanisms, making it more detailed.

Similar to the New York Loan Agreement form, a Mortgage Agreement also involves a lending and borrowing dynamic, but specifically ties the loan to real estate property as collateral. This similarity lies in the safeguard mechanisms for the lender, ensuring there's a secured asset that can be pursued in the event of non-payment. The difference primarily lies in the document’s application and the inclusion of property-specific terms in a Mortgage Agreement.

A Personal Guarantee is another document that shares attributes with the New York Loan Agreement, especially when loans require a guarantee from an individual apart from the borrower. The similarity rests in providing security to the lender that the loan will be repaid—either by the borrower or, in case of default, by the guarantor. Unlike a Loan Agreement that is between the borrower and lender, a Personal Guarantee engages an additional party to cover repayment risks.

Similarly, a Line of Credit Agreement is akin to the New York Loan Agreement in that it governs the borrowing of funds, but it differs in its flexibility. It allows the borrower to draw funds up to a certain limit over a period of time, unlike a loan agreement which involves a lump-sum disbursement. They share the objective of specifying terms under which money is lent, but the Line of Credit Agreement offers a reusable credit mechanism, making it unique.

An Installment Sale Agreement shares a common purpose with the New York Loan Agreement—both involve payment over time. However, an Installment Sale Agreement is typically used for the purchase of goods or property, where the buyer pays for the item in periodic installments. While both documents outline payment schedules and terms, the Installment Sale Agreement also directly ties to the transfer of ownership of an asset.

Equally, a Lease Agreement, while primarily used for renting property, shares the structured payment agreement feature with the New York Loan Agreement. Both set forth payments terms, albeit for different reasons—one for borrowing money and the other for the right to use an asset. However, they intersect in detailing the financial obligations of the parties involved, including the amount and timing of payments.

Finally, a Business Partnership Agreement can resemble the New York Loan Agreement in scenarios where funding is provided within the framework of a partnership. It outlines the terms under which capital is introduced into the business, expectations for return, and financial management of the partnership. While focusing on the broader governance of a partnership, when it includes provisions for financial contributions, its function parallels the clarity and enforceability of loan agreements.

Filling out a New York Loan Agreement form can be a crucial step in formalizing a loan, whether it's for personal use or business purposes. To ensure the process goes smoothly and to protect all parties involved, it's important to understand what to do and what to avoid. Below we'll explore the dos and don'ts when completing this important document.

What to Do:

What Not to Do:

When it comes to the New York Loan Agreement form, several misconceptions cloud its understanding and use. These misunderstandings can affect both lenders and borrowers, possibly leading to missteps in the loan process. Here's a clearer picture of what people often get wrong about this document:

Everyone believes that a lawyer must draft the New York Loan Agreement form. While legal advice is highly recommended, especially for complex loans, the form itself can be completed by the parties involved, provided it meets all legal requirements of the state.

Many think that this form is only for business loans. However, the New York Loan Agreement can cover various types of loans, including personal loans between individuals.

A common misconception is that the interest rate on a loan can be set at any level. In reality, New York State has usury laws that limit the interest rate that can be charged.

Some assume that a verbal agreement is as legally binding as the written form. While verbal agreements can be enforceable, a written loan agreement provides clear evidence of the terms agreed upon by the parties.

It is often believed that the New York Loan Agreement form is overly complex and difficult to understand. Though legal documents can be detailed, this form is designed to be straightforward, especially with proper guidance.

There's a misconception that once signed, the terms of the loan agreement cannot be changed. In fact, parties can agree to modify the loan terms, provided such amendments are documented in writing.

Many think that the New York Loan Agreement is a standard form that lacks flexibility. This is not the case; the form can be tailored to the specific terms and conditions agreed upon by the borrowing and lending parties.

Some individuals believe that if the borrower defaults, the lender immediately takes possession of the collateral. The process is more complex and must follow state laws regarding debt collection and repossession.

There's a misconception that the New York Loan Agreement only protects the lender. While it does outline the borrower's obligations, it also provides protections for the borrower, clearly stating the scope of what they are liable for.

Finally, many believe that downloading a generic form online is sufficient. While generic forms can provide a starting point, it's crucial to ensure that the agreement complies with New York laws and fully covers the agreement's specific terms and conditions.

Understanding the New York Loan Agreement form and the realities behind these misconceptions is essential for a smooth and legally compliant lending process. Whether you're the lender or the borrower, it pays to know what the agreement entails and to seek proper guidance if necessary.

Filling out and using the New York Loan Agreement form is an essential step in formalizing loan terms between a lender and a borrower. Here are key takeaways to ensure both parties understand their responsibilities and rights under this agreement.

By paying close attention to these key takeaways, lenders and borrowers can ensure a clear understanding of their obligations and rights under the New York Loan Agreement. This can help prevent disputes and ensure a smooth repayment process.

Sample Promissory Note Florida - An acceleration clause may be included, allowing the lender to demand immediate repayment under certain conditions.

Loan Agreement Template Texas - It includes detailed contact information for both the lender and borrower, facilitating communication regarding the loan.

Promissory Note Template Georgia - It often details the governance of late fees, processing charges, and any other fees associated with the loan.

Maryland Promissory Note Download - The agreement outlines the lender's right to demand repayment and the borrower's promise to repay the principal and interest.