Legal New York Deed in Lieu of Foreclosure Form

Legal New York Deed in Lieu of Foreclosure Form

In the face of financial hardship, homeowners in New York have various options to avoid foreclosure, one of which is the Deed in Lieu of Foreclosure. This legal document is a voluntary agreement between the borrower and the lender, where the borrower transfers the ownership of the property to the lender. It serves as an alternative to foreclosure, offering a way for homeowners to relinquish their homes without going through the lengthy and damaging foreclosure process. By choosing this path, individuals can potentially avoid the negative impact on their credit scores that a foreclosure might entail. Furthermore, this agreement can provide relief for homeowners struggling to keep up with mortgage payments, while also allowing lenders to mitigate the often costly and time-consuming process of foreclosure. Understanding the major aspects of this form, including its benefits and implications, is crucial for New York homeowners considering this option.

New York Deed in Lieu of Foreclosure Template

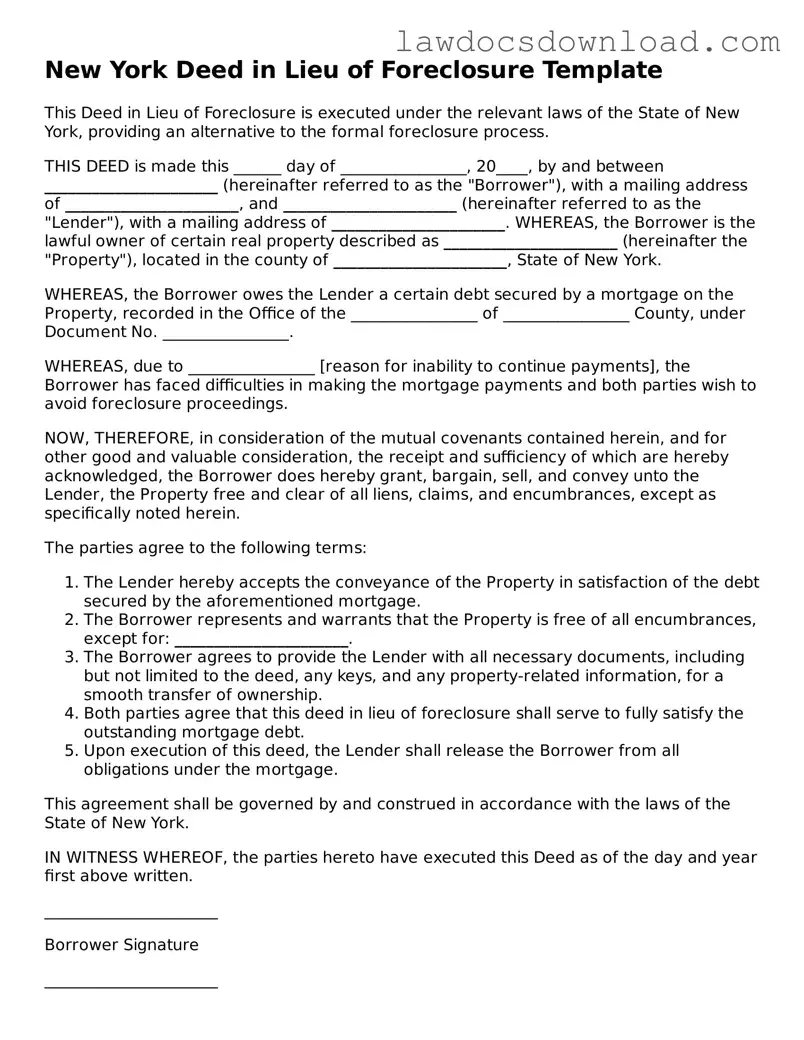

This Deed in Lieu of Foreclosure is executed under the relevant laws of the State of New York, providing an alternative to the formal foreclosure process.

THIS DEED is made this ______ day of ________________, 20____, by and between ______________________ (hereinafter referred to as the "Borrower"), with a mailing address of ______________________, and ______________________ (hereinafter referred to as the "Lender"), with a mailing address of ______________________. WHEREAS, the Borrower is the lawful owner of certain real property described as ______________________ (hereinafter the "Property"), located in the county of ______________________, State of New York.

WHEREAS, the Borrower owes the Lender a certain debt secured by a mortgage on the Property, recorded in the Office of the ________________ of ________________ County, under Document No. ________________.

WHEREAS, due to ________________ [reason for inability to continue payments], the Borrower has faced difficulties in making the mortgage payments and both parties wish to avoid foreclosure proceedings.

NOW, THEREFORE, in consideration of the mutual covenants contained herein, and for other good and valuable consideration, the receipt and sufficiency of which are hereby acknowledged, the Borrower does hereby grant, bargain, sell, and convey unto the Lender, the Property free and clear of all liens, claims, and encumbrances, except as specifically noted herein.

The parties agree to the following terms:

This agreement shall be governed by and construed in accordance with the laws of the State of New York.

IN WITNESS WHEREOF, the parties hereto have executed this Deed as of the day and year first above written.

______________________

Borrower Signature

______________________

Lender Signature

STATE OF NEW YORK

COUNTY OF ________________

On this ____ day of ________________, 20____, before me, the undersigned, personally appeared ________________, known to me (or satisfactorily proven) to be the person(s) whose name(s) is/are subscribed to the within instrument and acknowledged that he/she/they executed the same for the purposes therein contained.

______________________

Notary Public

My Commission Expires: ________________

| Fact Name | Description |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is a document in which a homeowner voluntarily transfers ownership of a property to the lender to avoid the foreclosure process. |

| Governing Law | In New York, Deeds in Lieu of Foreclosure are governed by state real estate laws and foreclosure statutes. Key statutes include Article 13 of the Real Property Actions and Proceedings Law (RPAPL). |

| Financial Impact | Executing a Deed in Lieu of Foreclosure may help homeowners avoid the negative credit implications associated with a full foreclosure process, though it may still have a significant impact on the borrower's credit score. |

| Consent Required | Lender consent is necessary for a Deed in Lieu of Foreclosure to be valid. The lender must agree to accept the deed as full satisfaction of the mortgage debt. |

| Benefits for the Borrower | Benefits for the borrower can include avoiding public foreclosure proceedings, potentially faster release from mortgage obligations, and a less severe impact on credit history. |

| Benefits for the Lender | For the lender, accepting a Deed in Lieu of Foreclosure can reduce the costly and time-consuming process of foreclosure, and the property can be more quickly prepared for resale. |

When a homeowner can no longer make payments on their mortgage, one option they might consider is a deed in lieu of foreclosure. This legal document effectively hands over the ownership of the property from the homeowner to the lender, bypassing the traditional foreclosure process. It's a step that can help both parties: the homeowner is relieved from the mortgage obligation, and the lender can avoid the lengthy and costly foreclosure process. Filling out the deed in lieu of foreclosure form in New York requires attention to detail and accuracy. The following steps will guide you through the process to ensure that the document is properly completed.

After completing these steps, the lender becomes the property's new legal owner, and the borrower is released from their mortgage obligation. It's important to keep a copy of the notarized and recorded deed for your records. Although this process can provide relief in challenging financial circumstances, it's advisable to consult with a legal professional before proceeding to ensure it's the right decision for your situation.

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal document where a borrower voluntarily transfers the ownership of a property to the lender as an alternative to foreclosure. This step is usually taken to avoid the consequences of a foreclosure proceeding, provided the lender agrees to accept the transfer. It’s a negotiated settlement between both parties, aiming to minimize additional financial burdens and potential legal conflicts.

Who can use the New York Deed in Lieu of Foreclosure form?

Property owners in New York facing financial difficulties, who are unable to continue making mortgage payments, can use this form. It's important that both the lender and the borrower agree to the terms laid out in the Deed in Lieu of Foreclosure. Legal consultation is advised to ensure that it meets the needs and circumstances of both parties involved.

What are the consequences of signing a Deed in Lieu of Foreclosure?

Signing a Deed in Lieu of Foreclosure transfers the property's ownership from the borrower to the lender, thus avoiding the foreclosure process. This action will still impact the borrower’s credit report but typically less severely than a foreclosure. The borrower may also be released from the obligation to pay the remaining balance on the mortgage, depending on the agreement. However, it’s vital to understand any tax implications or the possibility of a deficiency judgment being pursued by the lender.

What should be included in a New York Deed in Lieu of Foreclosure form?

The form should include the legal description of the property being transferred, the names and addresses of both the borrower and the lender, the terms of the agreement, and any additional conditions agreed upon by both parties. It should also outline any financial considerations, such as whether the transfer is in full satisfaction of the debt. Signatures from both the borrower and the lender, witnessed and notarized, are also necessary to complete the transfer.

Is the borrower responsible for any debts or liabilities after transferring the property?

Whether the borrower will be responsible for any remaining debts or liabilities after transferring the property depends on the terms negotiated with the lender. In some cases, the lender may agree to forgive the remaining debt entirely. However, in other situations, the borrower might still be responsible for any deficiency, which is the difference between the property's value and the outstanding debt. It’s critical to clearly understand these terms before completing the Deed in Lieu of Foreclosure.

Can a Deed in Lieu of Foreclosure be reversed or canceled?

Once a Deed in Lieu of Foreclosure is completed and recorded, it's very difficult to reverse. The agreement is considered final once both parties have signed and the document has been legally recorded. This underscores the importance of understanding all implications and having clear, precise terms before proceeding. Seeking legal advice before signing the document is strongly recommended.

Where can one obtain a New York Deed in Lieu of Foreclosure form?

The form can typically be obtained from a legal professional who can ensure that the document accurately reflects the agreement between the borrower and the lender. Additionally, certain online platforms might offer templates, but it’s essential to ensure that any form used fully complies with New York state laws. Customizing the document to the specific situation, with the help of legal counsel, is crucial to its effectiveness and legality.

When faced with the possibility of foreclosure, some individuals in New York consider the option of offering a deed in lieu of foreclosure to their lender. This choice can allow homeowners to voluntarily transfer the ownership of their property to the bank or financial institution holding the mortgage, potentially avoiding the foreclosure process. However, navigating the paperwork for such an agreement can be fraught with pitfalls. Here are eight common mistakes individuals make when filling out the New York Deed in Lieu of Foreclosure form.

One prevalent error is the failure to completely and accurately fill out all required sections of the form. Every field of the form serves a purpose, and neglecting any portion can result in the document being deemed invalid or cause delays in the process. Similarly, offering incorrect information, particularly regarding the property's legal description or mortgagor's details, can lead to significant issues, potentially rendering the agreement void.

Another misstep involves not adequately verifying that all lien holders have agreed to the deed in lieu transaction. Since a deed in lieu affects not only the primary mortgage but also any secondary liens on the property, consent from all parties is crucial. Failing to secure this agreement can complicate or nullify the process.

Overlooking the requirement to attach necessary documentation is yet another oversight. This could include a hardship letter, financial statements, or proof of the property being on the market and unsellable at a price that would cover the mortgage. Such documentation is vital for lenders to assess the situation fully and agree to the deed in lieu.

Individuals often neglect consulting with a legal professional or financial advisor before submitting the form. This step is crucial in understanding the potential impacts of a deed in lieu on one's financial situation and future homeownership prospects. Without professional guidance, homeowners may not fully appreciate the ramifications of their actions.

Another error is the failure to negotiate terms regarding the deficiency balance, which is the difference between the sale proceeds of the property (if any) and the amount owed on the mortgage. Without an agreement that the deed in lieu satisfies the debt in full, lenders may pursue the deficiency balance post-transaction.

Some individuals mistakenly believe that once they submit a deed in lieu of foreclosure form, the process is out of their hands. However, failing to follow up with the lender can lead to misunderstandings about the submission's status or additional requirements being overlooked.

Lastly, a significant mistake is not anticipating the tax implications of a deed in lieu. The forgiveness of debt can sometimes be considered taxable income, except under certain conditions outlined by tax law. Homeowners should consult a tax advisor to understand the potential tax consequences of their deed in lieu transaction.

Successfully navigating the deed in lieu of foreclosure process in New York requires meticulous attention to detail and an understanding of the legal and financial landscape. By avoiding these common mistakes, individuals can increase their chances of a smoother, more favorable transition out of homeownership under difficult circumstances.

When facing the possibility of foreclosure, some homeowners in New York may consider the option of a Deed in Lieu of Foreclosure. This legal document transfers ownership of the property from the homeowner to the lender, effectively avoiding the foreclosure process. However, this form is just one component of a comprehensive approach to addressing financial distress related to homeownership. Several other forms and documents are often used in conjunction with the New York Deed in Lieu of Foreclosure form to ensure a clear, legal, and efficient transfer of property.

A comprehensive understanding and careful handling of these documents ensure a smoother process for all parties involved in a deed in lieu of foreclosure. Homeowners considering this option should consult with legal professionals to fully understand the implications of these documents and to navigate the process effectively. This approach not only addresses immediate financial relief but also paves the way for future financial stability.

The Deed in Lieu of Foreclosure form shares similarities with the Mortgage Agreement. Both documents pertain to real estate transactions and the responsibilities of the borrower in relation to their lender. The Mortgage Agreement outlines the terms under which the lender provides a loan to the borrower for purchasing property, whereas the Deed in Lieu of Foreclosure comes into play as a remedy for a borrower's inability to meet those loan conditions. Essentially, both forms maintain the legal framework that governs the borrowing and lending of funds for real estate, but from different points within the lifecycle of the loan.

Another closely related document is the Quit Claim Deed. This document is utilized to transfer property ownership without any warranties regarding the title's clearness. Like the Deed in Lieu of Foreclosure, it results in a change of ownership. However, while the Deed in Lieu of Foreclosure specifically addresses the resolution of a delinquent loan by transferring property ownership back to the lender, a Quit Claim Deed can be used in various circumstances to convey property rights without guaranteeing the status of the property’s title.

The Short Sale Agreement also shares a relationship with the Deed in Lieu of Foreclosure. Both are alternatives to foreclosure that can be pursued by homeowners who are unable to continue making their mortgage payments. While the Deed in Lieu of Foreclosure entails the voluntary transfer of property back to the lender, a Short Sale Agreement involves selling the property for less than the amount owed on the mortgage with the lender's approval. Both options offer a way out for distressed borrowers, but they have different impacts on credit records and financial obligations.

Moreover, the Loan Modification Agreement is somewhat akin to the Deed in Lieu of Foreclosure in its attempt to avoid the foreclosure process. This agreement enables borrowers to renegotiate the terms of their existing loans with their lenders, potentially lowering their monthly payments or interest rates. Whereas the Deed in Lieu of Foreclosure signifies the end of the borrower’s ownership of the property, the Loan Modification Agreement signifies a mutual effort by the borrower and lender to continue the loan under modified terms that are manageable for the borrower.

Finally, the Foreclosure Notice is an important document that connects directly to the processes surrounding the Deed in Lieu of Foreclosure. It is an initial legal step a lender takes to inform a borrower that they are at risk of foreclosure due to non-payment. It precedes and contrasts the Deed in Lieu of Foreclosure, as the latter may be used to prevent the actual foreclosure process from going forward. Both documents are integral to the foreclosure sequence, but serve different roles; the Foreclosure Notice as a precursor and warning, and the Deed in Lieu of Foreclosure as a potential resolution.

When faced with the challenging decision of offering your property to the lender through a Deed in Lieu of Foreclosure as a way to avoid foreclosure, it's crucial to approach the process carefully and thoughtfully. Here are essential dos and don'ts to consider when filling out the New York Deed in Lieu of Foreclosure form:

Dealing with a Deed in Lieu of Foreclosure is a significant financial decision with long-term implications. Moving forward carefully, with a clear understanding and guidance, is critical in managing this process effectively and minimizing its impact on your financial future.

When discussing the New York Deed in Lieu of Foreclosure form, several misconceptions can arise due to its legal nature and the specific procedures involved in the state of New York. Below are five common misconceptions explained to provide clarity on the topic.

Understanding the specifics of a Deed in Lieu of Foreclosure in New York is crucial for homeowners considering this option. While it may offer a way to avoid foreclosure, both parties need to be clearly aware of the legal and financial implications involved.

When dealing with a Deed in Lieu of Foreclosure form, especially within New York State, there are several critical takeaways that can help make the process smoother and ensure that both parties’ rights are protected. Whether you're a homeowner facing financial difficulties or a lender seeking to mitigate losses, understanding these key points can be beneficial.

By keeping these key takeaways in mind, individuals can navigate the complexities of the Deed in Lieu of Foreclosure process in New York with greater confidence and understanding. This not only helps in making informed decisions but also in protecting the interests of all involved parties.

Sale in Lieu of Foreclosure - A preventative measure against foreclosure, where a borrower returns the property to the lender, fully transferring ownership.