Legal Massachusetts Promissory Note Form

Legal Massachusetts Promissory Note Form

In Massachusetts, individuals looking to formalize a loan agreement can utilize a tool known as the Promissory Note form. This document, essential for both lenders and borrowers, acts as a legally binding commitment, ensuring that money borrowed will be repaid under agreed upon terms. The form details critical elements like the amount borrowed, interest rates, repayment schedule, and any consequences of failing to meet the agreed terms. Its versatility means it can accommodate various lending scenarios, from personal loans between family members to more substantial loans involving real estate. Essential for providing legal clarity and minimizing misunderstandings, the Massachusetts Promissory Note form is a cornerstone in private lending, laying out the expectations and obligations of all parties involved.

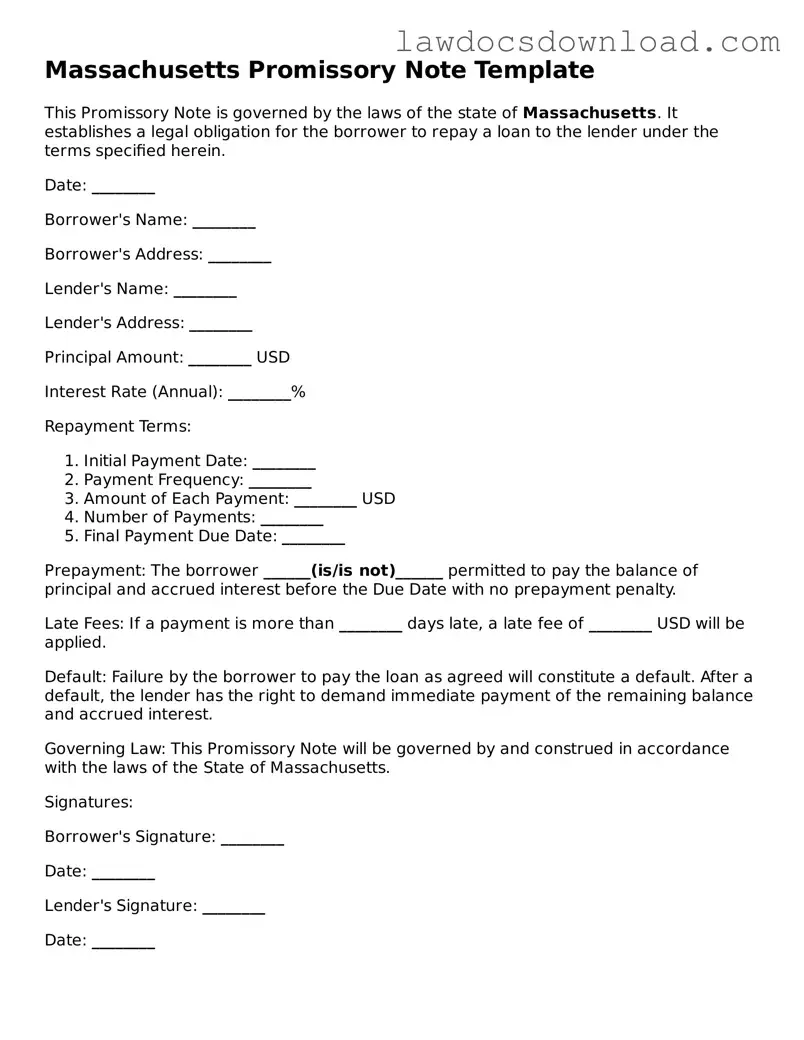

Massachusetts Promissory Note Template

This Promissory Note is governed by the laws of the state of Massachusetts. It establishes a legal obligation for the borrower to repay a loan to the lender under the terms specified herein.

Date: ________

Borrower's Name: ________

Borrower's Address: ________

Lender's Name: ________

Lender's Address: ________

Principal Amount: ________ USD

Interest Rate (Annual): ________%

Repayment Terms:

Prepayment: The borrower ______(is/is not)______ permitted to pay the balance of principal and accrued interest before the Due Date with no prepayment penalty.

Late Fees: If a payment is more than ________ days late, a late fee of ________ USD will be applied.

Default: Failure by the borrower to pay the loan as agreed will constitute a default. After a default, the lender has the right to demand immediate payment of the remaining balance and accrued interest.

Governing Law: This Promissory Note will be governed by and construed in accordance with the laws of the State of Massachusetts.

Signatures:

Borrower's Signature: ________

Date: ________

Lender's Signature: ________

Date: ________

| Fact Number | Fact Detail |

|---|---|

| 1 | Massachusetts promissory notes are legally binding documents. |

| 2 | They are governed by Massachusetts General Laws, specifically under chapters related to contracts and commercial paper. |

| 3 | A promissory note in Massachusetts must include the amount of money being borrowed. |

| 4 | It also must clearly state the interest rate, in compliance with the state's usury laws. |

| 5 | The full names and addresses of both the borrower and the lender need to be provided. |

| 6 | The repayment schedule, including dates and amounts, must be clearly outlined. |

| 7 | Signatures from both parties involved are mandatory for the document to be valid. |

| 8 | Any late fees or penalties for missed payments must be stated. |

| 9 | A provision regarding the acceleration of the loan, if applicable, should be included. |

Filling out the Massachusetts Promissory Note form is a straightforward process, yet attention to detail is crucial to ensure that the document is legally binding and clear to all parties involved. This form acts as a written promise by the borrower to pay back a specified sum of money to the lender by a certain date or on demand. It is often used for personal loans, business loans, and real estate transactions. The steps below are designed to guide you through the process, ensuring all necessary information is accurately captured to create a reliable and effective agreement.

Upon completing the steps above, it's essential to make copies of the signed document for both the borrower and the lender. This ensures that each party has a record of the agreement and understands their rights and obligations under the promissory note. Proper documentation and safekeeping of this form are key to protecting the interests of both parties throughout the duration of the loan.

What is a Massachusetts Promissory Note Form?

A Massachusetts Promissory Note Form is a legal document that outlines a loan's terms between a borrower and a lender within the state of Massachusetts. This document is crucial as it legally binds the borrower to repay the loan as agreed upon. The form contains important information such as the principal amount, interest rate, repayment schedule, and any other conditions agreed upon by both parties.

Is a Massachusetts Promissory Note required to be notarized?

In Massachusetts, a promissory note does not need to be notarized to be considered valid and enforceable. However, having the document notarized can add an extra layer of protection for both the lender and the borrower, verifying the authenticity of the signatures and helping to prevent disputes about the agreement's validity.

What are the legal requirements for a Promissory Note to be valid in Massachusetts?

Meeting these requirements helps ensure that the promissory note is enforceable in a court of law, should any disputes arise.

Can I modify a Massachusetts Promissory Note after it's been signed?

Yes, a Massachusetts Promissory Note can be modified after it has been signed, but any changes must be agreed upon by both the lender and the borrower. It is advisable to document these changes in writing and have both parties sign the modification to maintain clarity and legal protection. In some instances, creating a new promissory note to replace the old one may be necessary to reflect significant changes.

When individuals in Massachusetts set out to create a promissory note, a number of common mistakes often surface. These errors can potentially lead to disputes or legal misunderstandings. Understanding these pitfalls is the first step towards crafting a clear and enforceable promissory note.

One common mistake is not specifying the exact details of the loan. This includes the loan amount, interest rate, and repayment schedule. Without these details, a promissory note is often considered vague and can be difficult to enforce. It is crucial that these elements are clearly spelled out in the document to avoid any ambiguity.

Another frequent oversight is failing to include the legal names of all parties involved. Using nicknames or incomplete names can lead to confusion about who is legally bound by the note. For clarity and legal effectiveness, it's essential to use the full legal names of both the borrower and the lender.

A related issue is neglecting to outline the consequences of late payments or default. Without these details, enforcing penalties or taking legal action can be challenging. It's important to explicitly state the repercussions of failing to meet the terms of the note to protect the interests of the lender.

Many people also forget to have the promissory note witnessed or notarized. While this is not always a legal requirement in Massachusetts, having an impartial third party witness the signing can add an extra layer of validity to the document, especially in the event of a dispute.

Omitting the governing state law is another oversight. Specifying that Massachusetts law governs the promissory note helps ensure that any legal proceedings are conducted under the appropriate legal framework. This can be particularly important if the parties to the note reside in different states.

People often neglect to sign or date the promissory note, an error that can significantly undermine its legal standing. A promissory note must be signed by the borrower, and it's also advisable for the lender to sign. Including the date is crucial as it establishes when the agreement was made.

Another mistake is failing to provide a copy of the promissory note to all parties involved. Each party should have a copy for their records to prevent any disputes about the terms of the note. This practice ensures transparency and mutual understanding of the agreement's terms.

Finally, ignoring the need for an amendment procedure in the document is a common oversight. Circumstances can change, and having a predefined method for making amendments helps manage any modifications to the agreement in a legally sound manner. Without it, altering the note can be cumbersome and potentially contentious.

By avoiding these common mistakes, individuals can create a promissory note that is clear, enforceable, and minimizes the potential for legal complications. Attention to detail and adherence to legal norms are key to ensuring that both lenders and borrowers are protected.

When engaging in financial transactions in Massachusetts, the Promissory Note form is a crucial document. However, to ensure a smooth and legally sound agreement, several other forms and documents often accompany it. These documents not only provide additional legality and security to the transaction but also help in clearly delineating the rights and responsibilities of all parties involved.

These documents, when used together with the Massachusetts Promissory Note form, provide a framework that ensures clarity, legality, and enforceability of financial agreements. It is always recommended to properly understand and customize these documents to fit the specific needs of the individuals or entities involved. Consulting with a legal professional can help ensure that all paperwork is in order, thus protecting the interests of all parties involved.

The notion of a Massachusetts Promissory Note might resonate closely with the framework of a Loan Agreement. Both serve as binding contracts between a borrower and a lender, detailing the promise to repay a specified sum of money. However, the Loan Agreement dives deeper, encompassing detailed terms and conditions such as the repayment schedule, interest rates, and consequences of default. Thus, while a Promissory Note sketches the basic promise of repayment, a Loan Agreement paints the full financial picture between two parties.

Mortgage Notes exhibit a notable similarity to Promissory Notes, particularly with their shared emphasis on the borrower's promise to repay a debt. The distinctive factor for a Mortgage Note lies in its secured nature, often tied to a physical asset, such as real estate, as collateral. This collateral secures the lender's interest, providing a pathway to foreclosure should the borrower fail to honor the terms of repayment. Comparatively, while a Promissory Note may also be secured, a Mortgage Note specifically ties the promise to repay to a real property asset.

IOU documents, often seen as informal debt acknowledgments between parties, share a fundamental essence with Promissory Notes. Both declare a borrower's obligation to repay a lender, yet IOUs lack the detailed stipulations found in Promissory Notes. Typically, an IOU merely states that one party owes another without including repayment details, interest rates, or timelines. Contrarily, Promissory Notes formalize the debt obligation by incorporating these critical financial terms and conditions.

Line of Credit Agreements, while fostering a different financial structure, echo the Promissory Note's commitment to repay under specified conditions. These agreements allow the borrower access to a set amount of funds over a period, with the obligation to repay only the amount used. Unlike a Promissory Note, which specifies a fixed sum to be repaid, a Line of Credit Agreement offers flexible borrowing within a cap, underscoring a dynamic approach to borrowing and repayment.

Indenture Agreements, primarily used in the bond market, parallel the Promissory Note by recording a debt obligation. They typically involve multiple parties: the issuer, the trustee (representing the bondholders), and the bondholders themselves. Indenture Agreements detail the terms of the bond issue, such as the interest rate, maturity date, and the issuer's obligations. While Indenture Agreements are more complex and involve securities, at their core, they too are promises to repay borrowed money.

Student Loan Agreements, specific to educational borrowing, resonate with the Promissory Note through the mutual pledge to repay a debt. These agreements not only spell out the repayment obligations but also cater to the unique circumstances of student borrowers, often offering grace periods and varying interest rates. While Promissory Notes can be tailored for any lending purpose, Student Loan Agreements are inherently designed to support academic pursuits, making their specificity their standout feature.

Credit Card Agreements, although not a direct form of borrowing in the sense of receiving a lump sum upfront, share similarities with Promissory Notes in the obligations they create. These agreements grant the cardholder access to funds up to a certain limit, with the promise to repay the borrowed amount along with any accrued interest. The ongoing nature of credit card borrowing contrasts with the one-time loan structure of a Promissory Note but both ultimately revolve around the duty to repay under agreed-upon terms.

Personal Guarantees, while an assurance instrument more than a borrowing mechanism, share an intrinsic connection with Promissory Notes through the commitment to satisfy a debt. In a Personal Guarantee, a third party pledges to repay a borrower's debt should the borrower default. This guarantee underscores a layered promise to pay, akin to the direct promise found in a Promissory Note, adding a layer of security for the lender.

When it comes to filling out a Massachusetts Promissory Note form, accuracy and attention to detail are paramount. Below are key dos and don’ts to help guide you through the process:

Do:Verify the form is tailored for Massachusetts – laws can vary by state, and it’s critical to use the correct form for your jurisdiction.

Include all parties’ full legal names and addresses – this is essential for the identification of all involved and for future enforcement if needed.

Clearly state the loan amount in U.S. dollars – unambiguousness regarding the principal amount helps in avoiding any misunderstandings.

Outline the repayment schedule in detail – whether the loan is to be repaid in a lump sum, in regular installments, or upon demand, specify the terms clearly.

Specify the interest rate – ensure it's in compliance with Massachusetts’s legal rate limits to prevent the note from being usurious.

Rush through the process – taking the time to review every detail helps to avoid errors and future disputes.

Leave any blanks – incomplete information can lead to ambiguity or misuse of the promissory note.

Forget to define late fees or penalties for missed payments – clear consequences reinforce the importance of adhering to the agreed-upon repayment plan.

Omit the governing law clause – stating that Massachusetts law governs the note clarifies the legal framework for resolution of potential disputes.

By following these recommendations, you can fill out the Massachusetts Promissory Note form correctly and ensure a smooth and legally compliant transaction.

In discussing the Massachusetts Promissory Note form, there are several misconceptions that often cause confusion. Understanding these misconceptions can clear up many questions and concerns people have about these financial instruments. Here’s a breakdown:

Dispelling these misconceptions is vital for anyone involved in borrowing or lending in Massachusetts. Ensuring clarity and legal compliance in these matters can prevent disputes and foster stronger, more trustworthy financial relationships.

Filling out and using the Massachusetts Promissory Note form ensures that both lenders and borrowers are clear about the terms of a loan. This document is crucial for setting out repayment terms and protecting the interests of both parties involved. Here are eight key takeaways that individuals in Massachusetts should know when dealing with a Promissory Note:

While the process of drafting and signing a Promissory Note in Massachusetts may seem straightforward, paying attention to these key aspects can prevent future complications. Both lenders and borrowers should carefully consider their rights and responsibilities under the document to ensure a smooth financial transaction.

Promissory Note Template New York - Often used in conjunction with a loan agreement, providing a comprehensive overview of the loan terms.

Create Promissory Note - Business owners can leverage it as a tool for managing cash flow, either by obtaining quick funding or by offering credit terms to customers.

Texas Promissory Note Template - Modifications to the agreement, if needed, should be added through a formal amendment to the original promissory note to maintain its legal integrity.