Legal Maryland Promissory Note Form

Legal Maryland Promissory Note Form

In the world of finance and personal lending, the Maryland Promissory Note Form holds significant importance as a binding document that meticulously outlines the terms and conditions of a loan agreement between two parties. This essential piece of paper not only spells out the amount borrowed and the interest rate, if any, but also details the repayment schedule, ensuring both the lender and borrower have a clear understanding of their obligations. In Maryland, as in other states, this form serves as a legal acknowledgment of debt and carries with it the full force of the law should any disputes arise or the terms of the agreement are not met. It is tailored to meet the specific requirements of the state, thereby providing a level of security and peace of mind for those entering into personal or business financial transactions. The Maryland Promissory Note Form is a critical tool for facilitating a wide range of financial exchanges, from personal loans between family members or friends to more formal lending arrangements between businesses and individuals.

Maryland Promissory Note Template

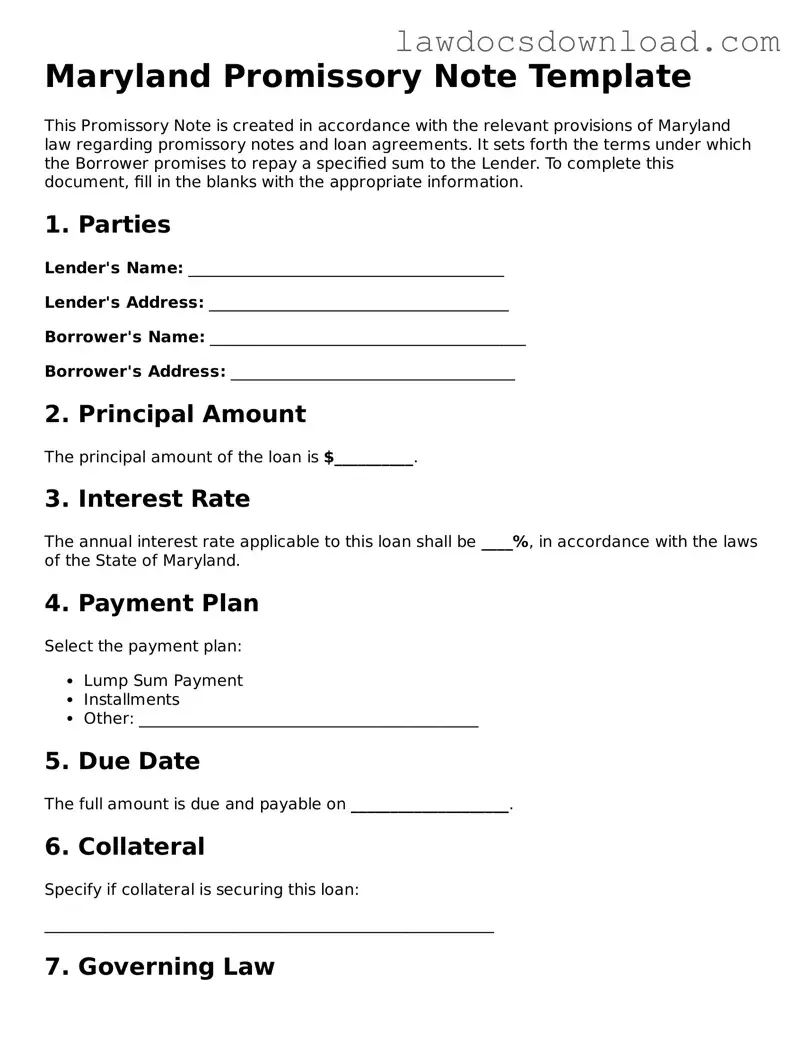

This Promissory Note is created in accordance with the relevant provisions of Maryland law regarding promissory notes and loan agreements. It sets forth the terms under which the Borrower promises to repay a specified sum to the Lender. To complete this document, fill in the blanks with the appropriate information.

1. Parties

Lender's Name: ________________________________________

Lender's Address: ______________________________________

Borrower's Name: ________________________________________

Borrower's Address: ____________________________________

2. Principal Amount

The principal amount of the loan is $__________.

3. Interest Rate

The annual interest rate applicable to this loan shall be ____%, in accordance with the laws of the State of Maryland.

4. Payment Plan

Select the payment plan:

5. Due Date

The full amount is due and payable on ____________________.

6. Collateral

Specify if collateral is securing this loan:

_________________________________________________________

7. Governing Law

This Promissory Note shall be governed under the laws of the State of Maryland.

8. Signatures

Both parties acknowledge receipt of this Promissory Note and agree to its terms and conditions:

Lender's Signature: ____________________________________

Date: ________________

Borrower's Signature: __________________________________

Date: ________________

9. Witness (Optional)

Witness's Signature: __________________________________

Date: ________________

Disclaimer

This template is provided "as is" without any warranty of any kind, expressed or implied. Both the lender and the borrower should review the terms of this agreement with legal counsel to ensure it meets their specific needs and complies with current Maryland laws.

| Fact Number | Detail |

|---|---|

| 1 | The Maryland promissory note form is a legal document that outlines the agreement between a borrower and a lender regarding a loan. |

| 2 | This form includes essential information such as the amount borrowed, interest rate, repayment schedule, and the parties' signatures. |

| 3 | In Maryland, the legal interest rate is set unless a different rate is agreed upon in the contract, in compliance with state laws. |

| 4 | Maryland law requires that promissory notes must be in writing to be enforceable. |

| 5 | The form serves as a legally binding agreement, ensuring that the borrower promises to repay the loan under the agreed-upon terms. |

| 6 | If the borrower fails to meet the repayment terms, the lender has the right to pursue legal action based on the promissory note. |

| 7 | Secured and unsecured are the two types of promissory notes; secured notes require collateral, while unsecured ones do not. |

| 8 | Under Maryland law, there are specific statutes of limitations for filing a lawsuit based on a promissory note, varying by situation. |

Completing the Maryland Promissory Note form is a formal way to establish the terms under which money is loaned and must be paid back. This document is crucial for both the lender and the borrower because it legally binds them to the agreement. The steps to fill out this form are straightforward, but attention to detail is essential to ensure that all the information is accurate and clearly understood by both parties. By following the steps closely, both the lender and the borrower can create a comprehensive agreement that outlines the repayment terms, interest rate, and what happens in case of a default.

Once the Maryland Promissory Note form is fully completed and signed, it serves as a legal document that both the lender and the borrower should keep in their records. It's a tangible reminder of the borrower's obligation to repay the loan and of the lender's rights to receive repayment. Proper completion and storage of this document can prevent misunderstandings and provide legal recourse in case disputes arise.

What is a Maryland Promissory Note?

A Maryland Promissory Note is a legal document that outlines a loan's terms and conditions between a lender and a borrower within the state of Maryland. This form serves as a written promise from the borrower to repay the loan amount plus any agreed-upon interest. The promissory note details the loan amount, interest rate, repayment schedule, and any penalties for late payments, ensuring both parties have a clear understanding of their obligations.

Are there different types of Promissory Notes in Maryland?

Yes, in Maryland, there are primarily two types of Promissory Notes: secured and unsecured. A secured Promissory Note requires the borrower to pledge an asset as collateral for the loan, providing the lender with security that the loan will be repaid. If the borrower fails to repay the loan, the lender has the right to claim the asset. An unsecured Promissory Note does not involve collateral, making it riskier for the lender, as there is no direct means to recover the loaned funds if the borrower does not repay the loan.

How is interest determined on a Maryland Promissory Note?

In Maryland, the interest rate on a Promissory Note must comply with the state's usury laws, unless a specific exception applies that allows for a higher rate. The agreed-upon interest rate should be clearly documented in the Promissory Note. It's important for both parties to be aware of the legal maximum interest rates to avoid usury violations, which can render the agreement void and result in penalties.

What are the requirements for a valid Promissory Note in Maryland?

To ensure a Promissory Note is legally valid and enforceable in Maryland, the document must include certain elements. These include the date the note was issued, the full names and addresses of both the borrower and the lender, the amount of money being loaned, the interest rate, and the repayment schedule. Signatures of both parties are also required. It is advisable for the note to be witnessed or notarized, although it is not a legal requirement in Maryland. Including these details provides clarity and legal standing to the agreement.

Can a Maryland Promissory Note be modified?

A Maryland Promissory Note can be modified if both the lender and the borrower agree to the changes. Any modification to the original terms should be documented in writing, and both parties should sign the amended agreement. Common modifications include changes to the repayment schedule, interest rate, or loan amount. It is crucial that any amendments are clearly outlined and agreed upon to maintain the note's enforceability.

Filling out a Maryland Promissory Note form is a critical step in formalizing a loan agreement. However, people often make mistakes during this process, which can lead to complications down the line. In the state of Maryland, as elsewhere, attention to detail and a clear understanding of the document's requirements are essential for both the borrower and the lender. Here are eight common mistakes that individuals make when completing this important document.

One frequent error is failing to include all necessary parties in the agreement. A Maryland Promissory Note should list everyone involved, not just the borrower and the primary lender. If there are co-signers or guarantors, their information must be included as well to ensure that all parties are legally bound to the agreement.

Another common oversight is not specifying the loan's interest rate. The interest rate directly affects the repayment amount and must be clearly stated. This rate should comply with Maryland's legal limits to prevent the agreement from being considered usurious or illegal.

Similarly, failing to outline the repayment schedule can lead to misunderstandings and disputes. This schedule details when payments are due, in what amount, and over what period. Without this, ambiguity could arise regarding expectations for loan repayment, potentially complicating the relationship between borrower and lender.

Many individuals also neglect to specify what will happen in the event of a default. This portion of the document protects the lender by detailing the actions that can be taken if the borrower fails to make payments as agreed. It's critical to be clear about this to avoid legal ambiguities if payments are missed.

Another mistake is not properly securing the promissory note. In Maryland, a secured note requires a description of the collateral that will be used to secure the loan. Without this, the loan is considered unsecured, possibly affecting the lender's ability to recoup the loaned amount if the borrower defaults.

Not including a clause on prepayment penalties or allowances is also a mistake. Borrowers benefit from knowing whether they can save on interest by repaying early without penalty, while lenders may wish to include a penalty to discourage early repayment.

Forgetting to clearly define terms such as "borrower" and "lender" can also lead to confusion. Each party's rights and responsibilities should be unmistakable to anyone reading the document, regardless of their familiarity with the agreement's context.

Last but certainly not least, failing to have the document witnessed or notarized in accordance with Maryland's requirements can affect its enforceability. Some types of promissory notes in Maryland must be notarized to be valid. Ignoring this step can lead to significant legal setbacks.

By avoiding these eight common mistakes, parties can ensure their Maryland Promissory Note is legally sound and reflects the agreement's terms accurately. This care in preparation helps protect all involved parties and supports a clear, enforceable loan agreement.

In Maryland, when entering into agreements involving financial transactions, a Promissory Note is often utilized to outline the details of the loan and the repayment terms. However, to fully secure the transaction and ensure all aspects are legally covered, other forms and documents are commonly used alongside the Promissory Note. These documents vary based on the specifics of the loan, the assets involved, and the parties' requirements for security and legal compliance.

These supplementary documents play a vital role in ensuring that all parties are fully aware of their rights and obligations and that the lender has adequate security for the loan. Using these forms in conjunction with a Maryland Promissory Note helps mitigate risks and provides a legal framework to address any issues that may arise during the repayment period.

The Loan Agreement shares similarities with the Maryland Promissory Note form, primarily due to its function of documenting the terms and conditions of a loan between two parties. In a loan agreement, the amount borrowed, interest rate, repayment schedule, and consequences of default are clearly outlined, much like they are in a promissory note. The main difference often lies in the level of detail and formalities involved, with loan agreements typically being more comprehensive and used for larger, more complex transactions.

A Mortgage Agreement is another document akin to the Maryland Promissory Note, as it specifically secures a loan on real property. Like a promissory note, a mortgage agreement outlines the borrower's obligation to repay the borrowed amount under agreed terms. However, it goes further by binding the loan to the physical property, allowing the lender to foreclose on the property if the borrower defaults, showcasing a key distinction tied to security and enforcement mechanisms.

The Personal Guarantee is related to the concept of a promissory note but from a third-party perspective. It involves an individual or entity (the guarantor) agreeing to repay a loan if the original borrower fails to do so, providing an additional layer of security to the lender. While a promissory note binds the borrower to the repayment terms, a personal guarantee extends the financial responsibility beyond the borrower, thus highlighting its role in risk mitigation for the lender.

An IOU (I Owe You) document is a simpler cousin of the Maryland Promissory Note, serving as a casual and informal acknowledgement of debt between two parties. While an IOU notes the basics like the amount owed and the parties involved, it lacks the legal robustness and detailed terms (such as repayment plan, interest, and collateral) typically found in a promissory note. This makes an IOU more suitable for minor loans between individuals who have a trust-based relationship.

Credit Agreements bear resemblance to promissory notes by detailing the terms under which credit is extended from a lender to a borrower. These agreements encompass a broad range of credit types, from personal loans to revolving credit lines, and define terms of interest rates, repayment schedules, and default consequences. Unlike promissory notes, which are usually more straightforward and involve a single lump-sum repayment or simple installments, credit agreements can offer more flexibility in borrowing and repayment terms.

The Deed of Trust is another related document, placing a third party in control of a borrower's property until a loan is fully repaid, similar to how a mortgage functions. This document accompanies a promissory note in transactions where real property is used as collateral. Despite its similarities, the deed of trust involves three parties (borrower, lender, and trustee), unlike the direct lender-borrower relationship in a promissory note, illustrating the inclusion of an intermediary in the lending and repayment process.

Student Loan Agreements are specialized versions of promissory notes, designed exclusively for borrowing funds to cover educational expenses. They outline the terms of repayment, interest rates, deferment policies, and forgiveness options — elements also present in standard promissory notes. However, what sets these agreements apart are the specific conditions and protections afforded to borrowers, reflecting the unique purpose and public policy considerations of educational financing.

Finally, a Line of Credit Agreement shares attributes with promissory notes, offering a flexible borrowing mechanism where the borrower has access to a specified amount of funds over a set period. Borrowers can draw from, repay, and redraw funds within the credit limit, making it distinctively adaptable compared to the static amount and repayment schedule of a promissory note. Both documents serve to formalize the terms under which money is borrowed, but the line of credit provides ongoing access to funds, unlike the one-time transaction nature of most promissory notes.

Filling out a Maryland Promissory Note form requires attention to detail and an understanding of what is legally binding. A promissory note is an important document that outlines how much money has been borrowed and the terms under which it will be paid back. When creating this document, there are certain practices you should follow to ensure everything is in order, as well as common pitfalls to avoid. Here's a helpful guide:

Do’s:Maryland's Promissory Note form is often misunderstood. Several misconceptions surround this legal document, affecting how it's used and interpreted. Here's a breakdown of common misunderstandings and the truth behind them:

It's the same as a loan agreement. People often confuse promissory notes with loan agreements. While both relate to borrowing, a promissory note is a promise by the borrower to pay back a debt under specified conditions. A loan agreement typically includes more detailed provisions, such as collateral and actions in case of default.

It doesn't need to be formal. Some believe that a promissory note does not require a formal structure or standard language to be valid. However, to be legally binding in Maryland, certain elements must be clearly stated, such as the amount borrowed, interest rate, repayment schedule, and the signatures of both parties involved.

Only the borrower needs to sign. A common misconception is that only the borrower's signature is necessary. In reality, for a promissory note to be enforceable in Maryland, it usually must be signed by both the borrower and the lender, acknowledging the terms and the agreement between both parties.

Verbal agreements are just as good. While oral contracts can be enforceable, a written promissory note provides clear evidence of the agreement's terms and conditions. Maryland law generally requires that promises to pay financial debts be documented in writing to be legally binding.

Any template will work. People often think they can use any template for a promissory note. However, Maryland may have specific requirements or recommended provisions to include in the note. Using a generic template without ensuring it complies with Maryland law could result in an unenforceable note.

Understanding the specifics of the Maryland Promissory Note form helps ensure that the process of lending or borrowing is both effective and legally compliant. Clear documentation, formalities, and adherence to state laws play crucial roles in protecting the interests of both parties involved.

When completing and utilizing the Maryland Promissory Note form, it's essential to be keenly aware of the specifics that set the groundwork for a legally enforceable agreement. Below are key takeaways to guide you through the process, ensuring clarity and compliance with Maryland state laws.

Proper completion and understanding of the Maryland Promissory Note are fundamental in safeguarding the interests of both the borrower and the lender. Adhering to these guidelines can help in ensuring that the promissory note fulfills its role as a clear, enforceable agreement that reflects the intent and terms agreed upon by the involved parties.

Promissory Note Template Oregon - If the borrower fails to comply with the terms, the Promissory Note provides a basis for legal recourse by the lender.

Georgia Promissory Note - Reflects a mutual understanding and agreement on the method of loan repayment, bridging trust gaps between the parties.

Blank Promissory Note - It should clearly state the parties involved, the loan amount, interest rate, repayment schedule, and any governing law to handle disagreements or defaults.