Legal Maryland Loan Agreement Form

Legal Maryland Loan Agreement Form

When individuals or entities in Maryland decide to lend or borrow money, the process is significantly streamlined and made more secure by utilizing a Maryland Loan Agreement form. This pivotal document plays a crucial role in ensuring the terms of the loan are clear, legally binding, and understood by all parties involved. It meticulously outlines the loan amount, repayment schedule, interest rates, and any collateral pledged against the loan. Furthermore, it serves to protect the interests of both the lender and the borrower, preventing misunderstandings and legal disputes that might arise in the absence of a written agreement. For anyone navigating the financial landscapes of lending or borrowing in Maryland, understanding the components and importance of this agreement is essential. It provides a foundation of trust and clarity, making it an indispensable tool in financial transactions.

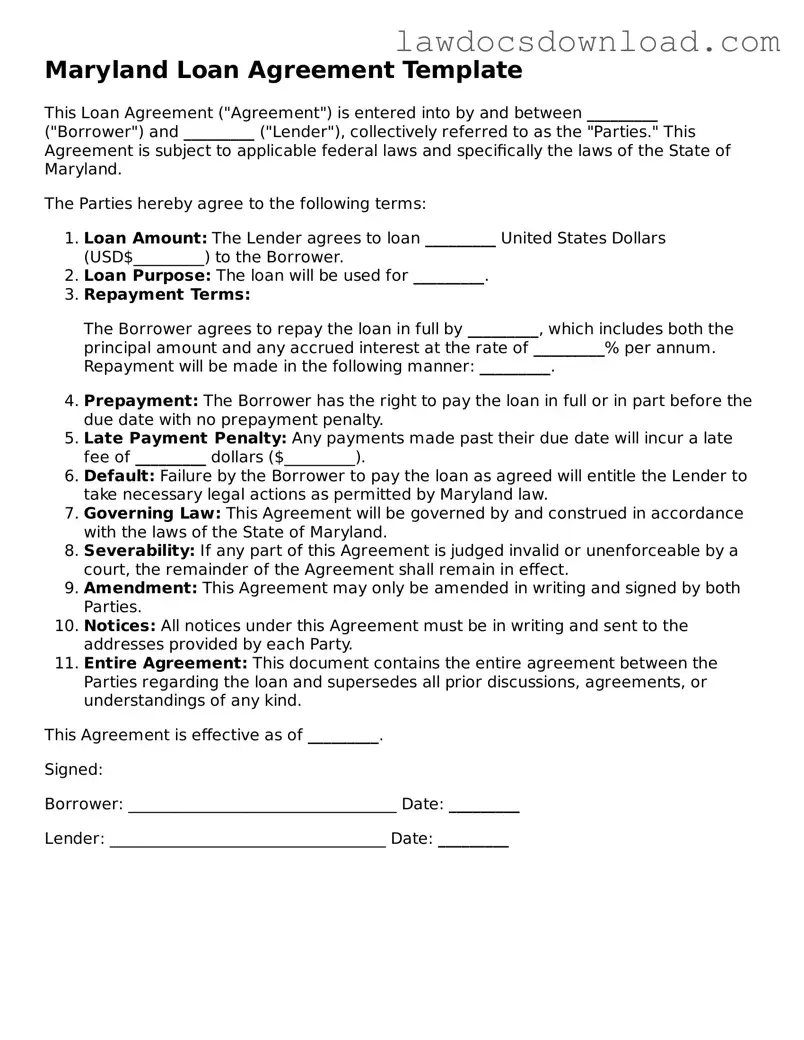

Maryland Loan Agreement Template

This Loan Agreement ("Agreement") is entered into by and between _________ ("Borrower") and _________ ("Lender"), collectively referred to as the "Parties." This Agreement is subject to applicable federal laws and specifically the laws of the State of Maryland.

The Parties hereby agree to the following terms:

The Borrower agrees to repay the loan in full by _________, which includes both the principal amount and any accrued interest at the rate of _________% per annum. Repayment will be made in the following manner: _________.

This Agreement is effective as of _________.

Signed:

Borrower: __________________________________ Date: _________

Lender: ___________________________________ Date: _________

| Fact Name | Description |

|---|---|

| Scope and Purpose | The Maryland Loan Agreement form is designed for use within the state of Maryland to outline the details of a loan between a lender and a borrower, specifying the terms, conditions, and responsibilities of each party. |

| Governing Laws | This agreement is governed by the laws of the State of Maryland, including but not limited to, the Maryland Commercial Law Article that regulates transactions and the Maryland Consumer Loan Law concerning loans made to consumers. |

| Usability | The form is versatile, suitable for a variety of loans, including personal loans, business loans, and mortgages, as long as the borrower and lender agree to abide by Maryland state laws. |

| Requirements | It must be completed in full and may require additional documents, such as proof of identity for both parties, details about the loan, and security agreements, if applicable. |

| Customization | The Maryland Loan Agreement form allows for customization to fit specific loan details, such as loan amount, interest rate, repayment schedule, and any collateral offered. |

| Legal Importance | Completing this form provides legal protection for both lender and borrower, ensuring there is a documented understanding and agreement which can be enforceable in a Maryland court of law, should disputes arise. |

Completing the Maryland Loan Agreement form is a significant step toward securing a loan within the state. This document, once filled out properly and submitted, acts as a legal representation of the terms and conditions agreed upon by both the borrower and lender. This process can seem daunting, but with careful attention to each step, individuals can navigate it successfully. The following instructions are designed to guide individuals through this process, ensuring that all necessary information is provided accurately to avoid any potential issues or delays.

After the Maryland Loan Agreement form has been filled out, it should be reviewed by both parties to ensure accuracy and understanding of the terms. Any errors should be corrected, and any unclear terms should be clarified before the document is signed. Following this, the form is to be filed appropriately, with each party retaining a copy for their records. This document then serves as a legal commitment between the borrower and lender, with enforceable terms and conditions as outlined in the agreement.

What is a Maryland Loan Agreement form?

A Maryland Loan Agreement form is a legally binding document between two parties, a lender and a borrower, outlining the terms and conditions of a loan. This form is specific to the state of Maryland, ensuring compliance with its laws and regulations regarding lending practices.

Who needs to use a Maryland Loan Agreement form?

Any individual or entity planning to either lend or borrow a sum of money within the state of Maryland should use this form. It is essential for both personal loans between family members or friends and commercial loans between businesses or between businesses and individuals.

What key elements should be included in the form?

Do I need a lawyer to create a Maryland Loan Agreement?

While it's not legally required to have a lawyer draft a loan agreement, consulting with one can ensure that the agreement complies with Maryland laws and fully protects your rights. For more complex agreements, especially involving large sums of money or collateral, getting legal advice is highly recommended.

How does a Loan Agreement protect the lender?

This agreement protects the lender by legally binding the borrower to repay the borrowed amount under the agreed-upon terms. It may also include provisions for recovering the loan through collateral in case of default, thus reducing the risk of financial loss.

How does a Loan Agreement protect the borrower?

The agreement also benefits the borrower by clearly stating the loan's terms, such as the interest rate, repayment schedule, and any fees, which helps prevent any surprises. Additionally, it ensures that the lender cannot arbitrarily change the terms or demand early repayment without cause.

Can the terms of a Maryland Loan Agreement be modified after it’s signed?

Yes, the terms can be modified, but any changes must be agreed upon by both the lender and the borrower. The modification should be made in writing and signed by both parties, ideally with the same level of formality as the original agreement to ensure its enforceability.

What happens if the borrower defaults on the loan?

The consequences of a default should be clearly outlined in the agreement. Typical consequences might include initiating a collection process, seizing collateral if any was provided to secure the loan, and/or taking legal action to recover the owed amount.

Is a Maryland Loan Agreement legally enforceable without being notarized?

Yes, a loan agreement is generally enforceable in Maryland without notarization. However, having the document notarized can add an extra layer of legitimacy and may help in the enforcement process, especially if the agreement’s validity is challenged.

Where can I find a template for a Maryland Loan Agreement form?

Templates for Maryland Loan Agreement forms can be found online through legal services websites, state-specific resources, or by consulting with a legal professional who can provide a customizable template suited to your specific needs.

One common error made by individuals when filling out the Maryland Loan Agreement form is neglecting to include all relevant parties in the document. This oversight can include failing to list every borrower, co-borrower, and guarantor involved in the agreement. Ensuring that all participating entities are correctly identified is crucial for the legal validity of the document.

Another mistake frequently encountered is the incorrect or incomplete description of the loan amount and terms. People often fail to specify the exact loan amount in words and figures or to fully outline the repayment schedule. This ambiguity can lead to misunderstandings and disputes about the loan obligations between the parties involved.

Failure to detail the interest rate is another common pitfall. Sometimes, individuals overlook specifying whether the interest rate is fixed or variable. Additionally, failing to mention how the interest is calculated - whether on an annual, monthly, or daily basis - can create significant confusion regarding the total cost of the loan over time.

Not addressing the consequences of a default properly is a major mistake. Many omit critical details about what constitutes a default, the notice period for a default, and the penalties or actions that will be taken if the loan is not repaid according to the agreed terms. This exclusion can weaken the lender's position in enforcing the loan agreement.

Leaving out governing law and dispute resolution clauses is often overlooked. Individuals sometimes forget to specify which state's laws will govern the agreement and how disputes related to the loan will be resolved. This omission can lead to legal uncertainties and complexities in the event of a disagreement.

Omission of signatures and dates at the end of the document is a crucial mistake. All parties involved must sign and date the loan agreement for it to be considered legally binding. Failing to do so means the document could be deemed invalid or unenforceable in a court of law.

Lastly, a lack of witness or notary public acknowledgments can undermine the formality and enforceability of the agreement. Although not always required, having the agreement witnessed or notarized adds a layer of verification and authenticity, making it more robust in legal contexts.

When entering into a loan agreement in Maryland, it's essential to be well-prepared with all the necessary documentation. This ensures a clear understanding between the borrower and lender, and legally safeguards the interests of both parties. Alongside the Maryland Loan Agreement form, several other documents are often utilized to support and clarify the terms, responsibilities, and obligations involved in the financial transaction. Knowing these documents can help both parties navigate the process more efficiently.

Gathering and understanding these supporting documents can significantly streamline the loan process, ensuring both parties are well-informed and protected throughout the duration of the loan agreement. It's always advisable to review all paperwork thoroughly and possibly seek legal guidance to ensure everything is in order, providing peace of mind for what can be a substantial financial commitment.

The Maryland Loan Agreement form shares similarities with a Promissory Note in that both establish a promise to pay a certain amount of money. A Promissory Note is usually more straightforward and involves fewer details about the repayment structure. It spells out the borrower's promise to repay the lender, often without needing collateral, whereas a Loan Agreement typically includes more detailed provisions such as interest rates, payment schedules, and security interests.

A Mortgage Agreement also shares common ground with the Maryland Loan Agreement, particularly in its function of outlining the terms under which money is borrowed to purchase real estate. The Mortgage Agreement goes a step further by securing the loan against the property being purchased, meaning the lender can foreclose on the property if the borrower fails to make payments as agreed, a level of security that may or may not be present in a generic Loan Agreement.

The Personal Loan Agreement is akin to the Maryland Loan Agreement, with both serving the purpose of documenting the terms under which one party lends money to another. The difference often lies in the relationship between the parties; personal loan agreements typically involve individuals, possibly friends or family. In contrast, the Maryland Loan Agreement might encompass broader professional lending scenarios, including business or commercial loans.

A Car Loan Agreement is specific to financing the purchase of a vehicle, making it similar to the Maryland Loan Agreement when it's used for the same purpose. Both outline the amount borrowed, the repayment schedule, interest rate, and consequences of non-payment. The Car Loan Agreement, however, is tailored specifically towards the purchase of a vehicle and often includes details about the vehicle as collateral.

Student Loan Agreements and the Maryland Loan Agreement form both facilitate the borrowing of money for educational purposes. However, student loan agreements are designed especially for students and usually contain terms reflecting the unique conditions of student loans, like deferment options during school attendance and grace periods after graduation, which aren't typically found in general loan agreements.

The Business Loan Agreement and the Maryland Loan Agreement can overlap when the loan's purpose is to finance business operations or expansion. Both outline the loan's terms, including repayment schedules, interest, and collateral. Yet, business loan agreements often include covenants or agreements reflecting the business’s performance, which might not be relevant or present in more generalized loan agreements.

Credit Agreements, while broad, share the concept of extending credit under specified terms, much like the Maryland Loan Agreement form. Credit agreements, however, can be more complex, covering lines of credit, credit cards, and revolving credit terms, whereas a loan agreement typically covers a single transaction with fixed repayment terms.

The Debt Settlement Agreement parallels the Maryland Loan Agreement in its focus on the aspects of repayment. However, it differs fundamentally in purpose; it is used to renegotiate or settle existing debt under new terms, often for a lesser amount than originally owed, which contrasts with a loan agreement's aim to structure the initial terms of a new loan.

A Co-Signer Agreement is related to the Maryland Loan Agreement in cases where a loan agreement requires the assurance of an additional party. This type of agreement outlines the co-signer's obligations to repay the loan if the primary borrower fails to do so, adding a layer of security for the lender. The main loan agreement defines the borrowing terms, while the co-signer agreement specifies the co-signer’s responsibilities.

Lastly, an Equipment Financing Agreement shares similarities with the Maryland Loan Agreement when the funds are used to purchase equipment. Both documents dictate the terms of financing, including repayment and interest. However, the equipment financing agreement uniquely addresses the specific scenario of acquiring equipment, often including provisions that treat the equipment itself as collateral for the loan.

Filling out the Maryland Loan Agreement form is a crucial step in securing a loan within the state. The document must be approached with care to ensure all information is accurate and complete. Below are lists of what you should and shouldn't do while completing this form.

What You Should Do

What You Shouldn't Do

When navigating the legal landscape of loan agreements in Maryland, several misconceptions can lead people astray. It is crucial to debunk these myths to ensure both lenders and borrowers are well-informed. Despite the common nature of these documents, there are details that often get overlooked or misunderstood.

All loan agreements are the same: A pervasive misconception is that loan agreements in Maryland follow a one-size-fits-all approach. However, the truth is each agreement is tailored to the specific circumstances of the loan it pertains to. Factors such as the loan amount, interest rate, repayment schedule, and collateral, if any, can significantly vary from one agreement to another.

Verbal agreements are just as binding: While oral contracts can be recognized legally in Maryland, relying solely on a verbal agreement for a loan presents significant risks. Without a written document, proving the terms of the agreement and the parties' intentions becomes challengingly complex. Moreover, the Maryland Statute of Frauds requires certain contracts, including those for loans over a certain amount, to be in writing to be enforceable.

A notary signature is always required: Many individuals mistakenly believe that a notary's signature is a prerequisite for a loan agreement to be valid in Maryland. While having a notary witness a loan agreement can add an extra layer of validity and protect against disputes by confirming the identity of the signatories, it is not a legal requirement for the enforceability of the document.

Only financial institutions can issue loan agreements: Contrary to popular belief, you do not have to be a bank or formal financial institution to enter into a loan agreement in Maryland. Private individuals can lend money to others and can use a loan agreement to ensure the terms are clear and enforceable. It is wise, however, for both parties to draft a comprehensive agreement that outlines the loan's terms to prevent misunderstandings and potential legal disputes.

Dispelling these misconceptions is essential for both lenders and borrowers. It helps protect their interests and ensures a smooth lending process. Whether partaking in a personal loan between friends or a more formal arrangement, understanding the legal requirements and rights involved in a Maryland Loan Agreement form is key to a successful and fair transaction.

When it comes to navigating the complexities of filling out and using the Maryland Loan Agreement form, attention to detail is key. This document is a legal contract between a borrower and a lender, where the borrower agrees to repay borrowed money with interest. Here are several important takeaways to ensure that the process is handled correctly and effectively:

By focusing on these key aspects, individuals can ensure that the Maryland Loan Agreement form is filled out and used effectively, safeguarding the interests of all parties involved.

Promissory Note Template Georgia - Force majeure clauses may cover circumstances under which repayment terms could be modified due to unforeseen events.

Promissory Note New York - Facilitates a legal and financial agreement where money is lent at an agreed-upon interest rate, with specified repayment dates and terms.