Legal Maine Promissory Note Form

Legal Maine Promissory Note Form

In the picturesque state of Maine, individuals and entities looking to formalize a loan agreement have a go-to legal instrument: the Maine Promissory Note form. This document is pivotal for delineating the conditions under which money is borrowed and the repayment is structured. It meticulously outlines the amount borrowed, the interest rate applicable, repayment schedule, and the consequences of failing to meet the agreed-upon terms. The significance of this form extends beyond its practical utility in preventing misunderstandings between the lender and borrower; it also holds legal weight in courts, serving as a binding commitment that can be enforced should disagreements arise. Tailored to Maine's specific legal requirements, the form ensures compliance with state laws, providing both parties with a sense of security and clarity. Whether for personal loans between friends and family or more formal lending arrangements, the Maine Promissory Note form stands as a critical document in the lending process, embodying the agreement's spirit while safeguarding both parties' interests.

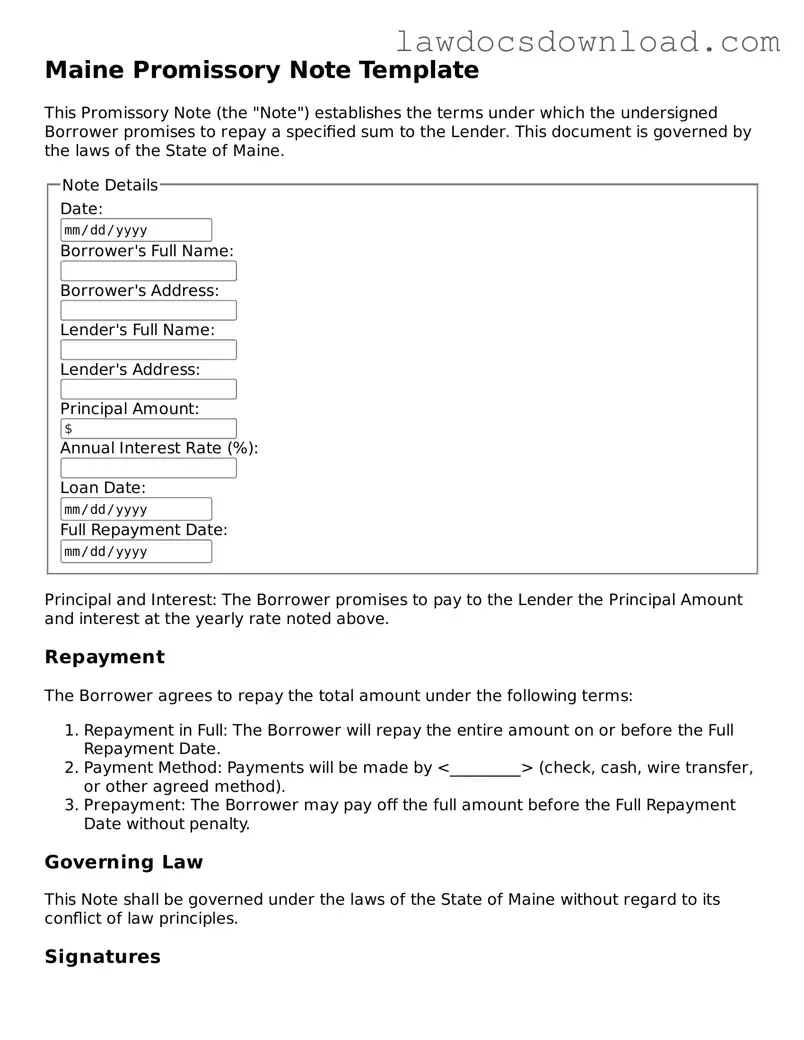

Maine Promissory Note Template

This Promissory Note (the "Note") establishes the terms under which the undersigned Borrower promises to repay a specified sum to the Lender. This document is governed by the laws of the State of Maine.

Principal and Interest: The Borrower promises to pay to the Lender the Principal Amount and interest at the yearly rate noted above.

Repayment

The Borrower agrees to repay the total amount under the following terms:

Governing Law

This Note shall be governed under the laws of the State of Maine without regard to its conflict of law principles.

Signatures

By signing below, both parties agree to the terms of this Note.

Borrower's Signature: ____________________________________ Date: ____________

Lender's Signature: ______________________________________ Date: ____________

| Fact | Description |

|---|---|

| Type of Document | Maine Promissory Note Form |

| Governing Law | Maine Uniform Commercial Code - Title 11, Article 3 |

| Function | Details the terms under which money is borrowed and must be repaid. |

| Types | Secured and Unsecured |

| Key Elements | Amount borrowed, interest rate, repayment schedule, and signatures. |

| Requirement for Validity | Must be signed by the borrower and, in some cases, co-signed by a guarantor. |

| Interest Rate Limit | Subject to Maine’s usury laws, maximum allowable rate unless otherwise legally exempt. |

| Prepayment | Borrowers can pay off the note early, potentially without penalty - specific terms vary. |

| Use in Legal Proceedings | Can serve as evidence of debt in a court of law in case of disputes or default. |

Filling out a Maine Promissory Note form is an important step in formalizing a loan agreement between two parties. It is a legally binding document that outlines the terms of the loan, including the amount borrowed, the interest rate, and the repayment schedule. By carefully completing this form, both the borrower and lender can ensure that the details of the loan are clearly understood and agreed upon, reducing the potential for disputes in the future. Below are steps to guide you through the process of filling out the Maine Promissory Note form.

By following these steps, parties can successfully create a Maine Promissory Note that is thorough, clear, and legally binding. This document plays a crucial role in ensuring that both the borrower and lender are protected and have a clear understanding of their responsibilities and rights under the loan agreement.

What is a Maine Promissory Note?

A Maine Promissory Note is a legal document where one party, known as the borrower, agrees to pay back a certain amount of money to another party, the lender. This document includes specifics such as the total amount borrowed, interest rate, repayment schedule, and any other terms related to the loan. It serves as a written promise from the borrower to repay the amount under the agreed conditions.

Do Maine Promissory Notes need to be notarized?

While notarization is not specifically required for a promissory note to be considered legal in the state of Maine, it can add a layer of security by verifying the identity of the signatories and the integrity of the document. Notarization can also help in the enforcement of the note, should there be a dispute or need for legal action.

Can I charge interest on a loan in a Maine Promissory Note?

Yes, lenders can charge interest on a loan in a Maine Promissory Note. However, it is important to adhere to the state’s usury laws to avoid charging an illegal amount of interest. Maine’s usury laws cap the maximum interest rate that can be charged in the absence of an agreement. Lenders should verify the current cap on interest rates to ensure compliance.

How can I ensure the borrower pays back the loan according to the Promissory Note?

To increase the likelihood of repayment according to the terms of the Promissory Note, the lender should:

Additionally, if the borrower fails to adhere to the repayment terms, the lender may pursue legal action to enforce the note.

What should I do if I need to change the terms of the Maine Promissory Note after it's been signed?

If both the lender and borrower agree to modify the terms of the Maine Promissory Note after it has been signed, they should document the changes in writing. Both parties should initial any alterations on the original document or draft a new promissory note to reflect the agreed-upon terms. Having a record of these changes is crucial for protecting the rights of both parties.

Is a Maine Promissory Note legally binding?

Yes, a Maine Promissory Note is a legally binding document. Once signed by both the borrower and the lender, it creates an obligation for the borrower to repay the loan as detailed in the agreement. Failure of the borrower to comply with the terms of the note can result in legal action for collection, making it enforceable in a court of law.

Filling out a promissory note in Maine requires careful attention to detail. Often, individuals make mistakes that can significantly affect the legality and enforceability of the agreement. One common error is not specifying the terms of repayment clearly. This includes failing to outline the repayment schedule, such as the due dates and the number of payments, or omitting the interest rate, which can lead to disputes over the amount owed.

Another frequent mistake is neglecting to include all necessary parties in the documentation. A promissory note must identify the borrower and lender with full legal names and contact information. Sometimes, individuals forget to add co-signers or guarantors, who also need to be named in the document, weakening the enforceability of the note.

Additionally, overlooking the legal requirements specific to Maine can be a critical error. Each state has its own laws governing interest rates and usury laws, and failing to comply with these can render a promissory note invalid or unenforceable. For example, charging an interest rate above the legal limit could lead to penalties, or the interest portion of the note being voided.

Certain individuals also make the oversight of not having the promissory note witnessed or notarized, believing it is not necessary. While this might not always be a legal requirement, having an impartial third party witness the signing of the document can significantly enhance its credibility and the ability to enforce it, should disputes arise.

A common trap is the use of vague or ambiguous language, which can lead to interpretations that were not intended by either party. It is crucial to use precise, clear language that leaves no room for misinterpretation. This includes defining terms used in the note, explaining the meaning of technical financial terms, and being explicit about the obligations of each party.

Lastly, a significant mistake is failure to retain a copy of the signed document. Both the borrower and the lender should keep a copy of the promissory note. Losing the document can lead to challenges in proving the terms agreed upon or even the existence of the loan itself, making it difficult to take legal action if repayments are not made as agreed.

When creating or managing a promissory note in Maine, several other documents and forms are often used in tandem to ensure a comprehensive and legally sound agreement. These forms support and clarify the terms of the promissory note, secure the loan, and define the obligations of all parties involved. Understanding each document’s purpose helps in maintaining the integrity and enforceability of the financial agreement.

Together, these documents form a legal foundation that supports the effective administration of a loan, from origination through to repayment or default. Proper use and understanding of each document ensure that both parties’ rights are protected and that the agreement adheres to Maine's legal standards.

The Maine Promissory Note form is similar to a Loan Agreement, as both are legally binding documents outlining the terms under which money has been lent and needs to be repaid. A Loan Agreement, much like a Promissory Note, usually contains detailed information about the loan's terms, including the interest rate, repayment schedule, and consequences of default. However, a Loan Agreement is typically more detailed and may include provisions on dispute resolution and jurisdiction.

Another similar document is the IOU (I Owe You), which acknowledges that a debt exists and a certain amount of money is owed by one party to another. While an IOU is less formal and lacks specific repayment terms, it shares the Promissory Note's basic principle of acknowledging a debt.

The Mortgage Agreement is also closely related to a Promissory Note when it comes to real estate transactions. In this context, the Promissory Note outlines the borrower's promise to repay the loan, while the Mortgage Agreement secures the loan with the property being purchased as collateral. Both documents are essential for the creation of a binding financial obligation backed by real estate.

Similarly, a Deed of Trust may be compared to a Promissory Note, particularly in real estate financing. While the Promissory Note details the borrower’s promise to repay the loan, the Deed of Trust involves a third party (trustee) who holds the property's title until the loan is repaid. This arrangement adds an extra layer of security for the lender.

A Bill of Sale is another document that, while primarily used to transfer ownership of goods or property from seller to buyer, shares a common purpose with the Promissory Note in documenting a transaction. However, a Bill of Sale does not usually detail the terms of repayment as a Promissory Note does for loans.

The Credit Agreement is akin to a Promissory Note but is often used in more complex borrowing situations, like revolving credit lines or term loans from financial institutions. It details the borrower's obligations and the terms under which credit is extended, including interest and repayment schedules, similarly to how a Promissory Note functions for simpler, single-payment loans.

Last but not least, a Student Loan Agreement shares similarities with a Promissory Note, especially since it often involves a promissory note as part of the agreement. This document sets out the terms and conditions under which a student borrows money for education and commits to repaying the loan over time, specifying interest rates and repayment schedules akin to those found in Promissory Notes.

When it comes to filling out the Maine Promissory Note form, it is crucial to approach this document with attention to detail and accuracy. This form serves as a legal agreement between a lender and a borrower, outlining the terms under which a loan will be provided and repaid. The following list includes essential dos and don'ts to consider:

Adhering to these guidelines can help ensure that the Maine Promissory Note form is completed in a manner that is clear, comprehensive, and legally sound, providing protection and clarity for both the lender and the borrower.

Many people have misconceptions about the Maine Promissory Note form, which can lead to confusion and potential legal issues. Understanding the realities can help individuals navigate their financial agreements more effectively. Here are seven common misconceptions explained:

It's legally binding without signatures: A common misconception is that a promissory note is legally binding in Maine even without the signatures of the involved parties. In truth, signatures are crucial for enforceability; they evidence the agreement of the parties to the terms.

All promissory notes are the same: People often think one promissory note is much like another. However, the terms can vary significantly, including interest rates, repayment schedules, and consequences of default. Tailoring the document to the specific agreement is essential.

No need for witnesses or notarization: While Maine law does not always require witnesses or notarization for a promissory note to be valid, having these can add a layer of authenticity and might be necessary for the note to be enforced in certain situations.

They're only for financial institutions: A common belief is that promissory notes are tools exclusively for banks or financial institutions. In reality, anyone lending money can use a promissory note to outline the terms of repayment.

Terms cannot be changed once signed: Another misconception is that the terms of a promissory note are set in stone once it is signed. The truth is, as long as all parties agree, the terms can be modified. Such modifications should be documented in writing.

Interest rates are non-negotiable: Many think the interest rates on a promissory note are fixed and cannot be negotiated. However, the rate can be anything that both lender and borrower agree upon, within the legal limits established by Maine law.

Oral agreements are just as good: Some believe an oral agreement can substitute for a written promissory note. While oral contracts can be legal, proving the terms and the existence of the agreement is vastly more challenging without a written document, especially in a court setting.

Clearing up these misconceptions can help all parties involved in a promissory note agreement proceed with a better understanding and more confidence in their financial dealings.

The Maine Promissory Note form is a valuable tool for documenting a loan agreement between two parties, ensuring clarity and legal enforceability. When preparing and utilizing this form, it's important to keep in mind several key considerations to ensure that the document fulfills its purpose effectively and protects the interests of both the lender and the borrower.

Adhering to these guidelines when filling out and using the Maine Promissory Note form can help ensure that the agreement is clear, fair, and legally binding. It provides a systematic approach to documenting the loan that protects both the borrower's and lender's interests.

Does Promissory Note Need to Be Notarized - It specifies the penalty for late payments and any potential recourse a lender has if the borrower defaults.

Blank Promissory Note - It serves as a formal IOU, containing the borrower's commitment to repay the debt by a specified due date along with any applicable interest.

Blank Promissory Note - Interest calculations should be clearly defined, whether fixed or variable, to prevent ambiguity and ensure both parties understand the financial commitments involved.