Blank Loan Agreement Template

Blank Loan Agreement Template

When entering into a financial agreement where one party is lending money to another, it's crucial to have a clear and thorough document that outlines the specifics of the arrangement. The Loan Agreement form serves this very purpose, acting as a binding contract between the lender and the borrower. This important document covers various aspects such as the loan amount, interest rate, repayment schedule, and any collateral involved. It also outlines the obligations and rights of both parties, ensuring there is a mutual understanding and reducing the potential for disputes. Additionally, the form can include clauses related to late payments, default conditions, and early repayment options, making it a comprehensive tool for managing the loan effectively. By capturing all necessary details, the Loan Agreement form not only provides legal protection but also promotes transparency and trust between the involved parties.

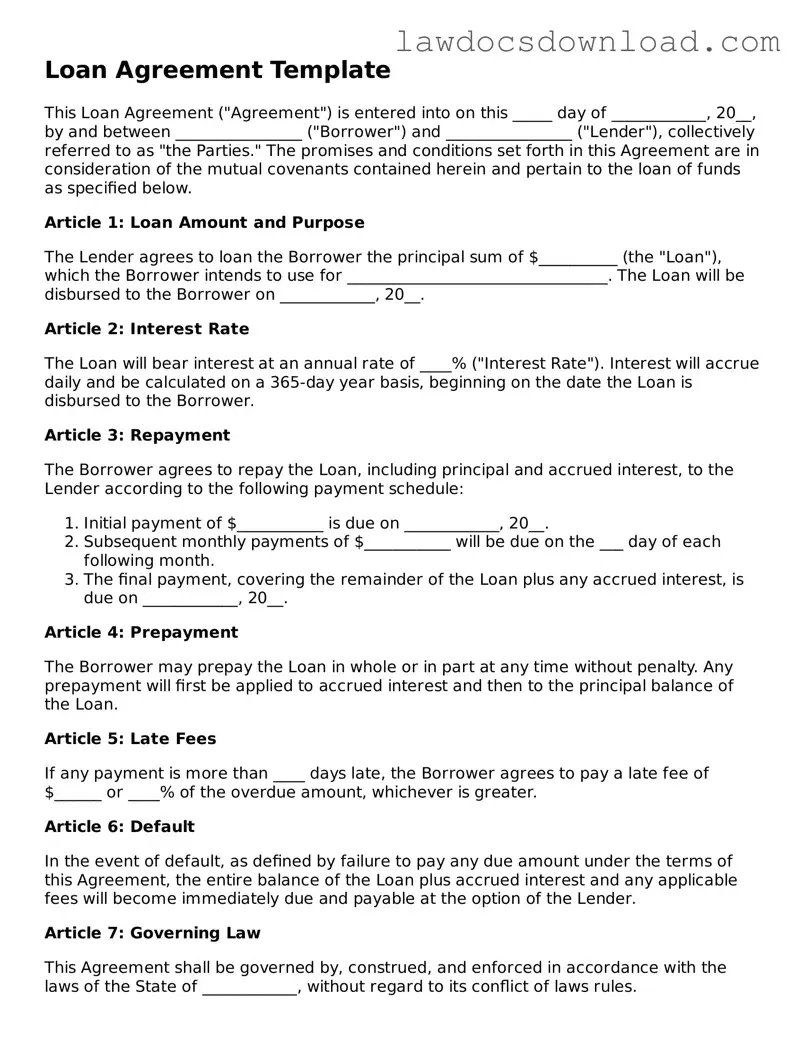

Loan Agreement Template

This Loan Agreement ("Agreement") is entered into on this _____ day of ____________, 20__, by and between ________________ ("Borrower") and ________________ ("Lender"), collectively referred to as "the Parties." The promises and conditions set forth in this Agreement are in consideration of the mutual covenants contained herein and pertain to the loan of funds as specified below.

Article 1: Loan Amount and Purpose

The Lender agrees to loan the Borrower the principal sum of $__________ (the "Loan"), which the Borrower intends to use for _________________________________. The Loan will be disbursed to the Borrower on ____________, 20__.

Article 2: Interest Rate

The Loan will bear interest at an annual rate of ____% ("Interest Rate"). Interest will accrue daily and be calculated on a 365-day year basis, beginning on the date the Loan is disbursed to the Borrower.

Article 3: Repayment

The Borrower agrees to repay the Loan, including principal and accrued interest, to the Lender according to the following payment schedule:

Article 4: Prepayment

The Borrower may prepay the Loan in whole or in part at any time without penalty. Any prepayment will first be applied to accrued interest and then to the principal balance of the Loan.

Article 5: Late Fees

If any payment is more than ____ days late, the Borrower agrees to pay a late fee of $______ or ____% of the overdue amount, whichever is greater.

Article 6: Default

In the event of default, as defined by failure to pay any due amount under the terms of this Agreement, the entire balance of the Loan plus accrued interest and any applicable fees will become immediately due and payable at the option of the Lender.

Article 7: Governing Law

This Agreement shall be governed by, construed, and enforced in accordance with the laws of the State of ____________, without regard to its conflict of laws rules.

Article 8: Amendments

This Agreement may only be amended, modified, or supplemented by an agreement in writing signed by each party hereto.

Article 9: Notices

All notices, requests, demands, and other communications hereunder shall be in writing and shall be deemed to have been duly given on the date of service if served personally on the party to whom notice is to be given, or on the third day after mailing if mailed to the party to whom notice is to be given, postage prepaid, and addressed to the party at the address stated above.

IN WITNESS WHEREOF, the Parties have executed this Loan Agreement as of the date first above written.

_________________________

Borrower: _________________________

_________________________

Lender: _________________________

| Fact Name | Description |

|---|---|

| Purpose | A Loan Agreement form is used to document the terms and conditions of a loan between a borrower and a lender. |

| Key Components | This form typically includes details such as the loan amount, interest rate, repayment schedule, and any collateral involved. |

| Legal Binding | Once signed by both parties, the Loan Agreement becomes a legally binding document that obligates the borrower to repay the loan under the agreed-upon terms. |

| Governing Laws | Loan Agreements are governed by the state laws in which the agreement is executed, and any disputes are resolved under those laws. |

| State-Specific Forms | Some states have specific requirements or provisions that must be included in the Loan Agreement, making the use of state-specific forms necessary. |

| Importance of Precision | Accuracy and thoroughness in detailing the loan terms, responsibilities, and obligations of both parties prevent future disputes and legal challenges. |

After deciding to formalize the terms of a loan between two parties, the next crucial step involves accurately completing a Loan Agreement form. This document not only sets the conditions of the loan but also serves as a legal record of the agreement, making it essential for protecting the interests of both the lender and the borrower. The process of filling out this form should be approached with care, ensuring that all relevant details are clearly and correctly documented. The following steps are designed to guide individuals through this process, helping them to complete the form efficiently and effectively.

Once the form is fully completed and signed, each party should keep a copy for their records. This serves as a protective measure and ensures that both the lender and the borrower have a reference to the agreed-upon terms. Completing the Loan Agreement form is a vital step in any lending process, providing clarity and legal standing to the financial transaction.

What is a Loan Agreement form?

A Loan Agreement form is a legally binding document between a lender and a borrower that outlines the terms of a loan. The agreement specifies the amount of the loan, the interest rate, the repayment schedule, and the obligations and rights of both the lender and the borrower. It's designed to protect both parties by making sure everyone understands their responsibilities and the terms of the loan.

Why is a Loan Agreement form important?

This form is crucial because it legally formalizes the loan. It helps in preventing misunderstandings or disputes by clearly defining the loan terms, such as the repayment period, interest rates, and any collateral involved. A detailed agreement can save both parties time and money by avoiding potential legal issues. Without this agreement, enforcing the terms of the loan becomes significantly harder if disagreements arise.

What key details should be included in a Loan Agreement?

Can I customize a Loan Agreement form to suit my needs?

Yes, a Loan Agreement form can and should be customized to fit the specific terms agreed upon by the lender and the borrower. It's important that the agreement accurately reflects all aspects of the loan's terms, including any special conditions or requirements. It's advisable to review the document carefully and ensure it meets your needs before signing.

Is a witness or notarization required for a Loan Agreement?

While not always legally required, having a witness or notarization can add a level of validity and enforceability to the agreement. The requirements can vary depending on the state and the complexity of the transaction. For larger loans or agreements involving collateral, notarization can help in verifying the identities of the parties and ensuring that the document is legally binding.

What happens if a borrower fails to repay the loan as agreed?

If a borrower fails to repay the loan according to the terms set out in the Loan Agreement, the lender has the right to enforce the agreement, which can include initiating legal action to recover the owed funds. The agreement may also specify penalties for late payments or default, which can include additional fees, higher interest rates, or the seizure of collateral. It's critical for borrowers to understand the consequences of failing to meet their repayment obligations.

One common mistake borrowers make when filling out a Loan Agreement form is not thoroughly reading the agreement. It's crucial to understand every clause to avoid agreeing to terms that are not favorable. Without a clear understanding, individuals may find themselves bound by conditions they did not anticipate, which can lead to significant financial and legal repercussions.

Another frequent error is inaccurately reporting financial information. Whether intentional or accidental, this misinformation can result in the rejection of the loan application or, even worse, legal action if the loan is granted based on false information. Honesty and accuracy are paramount when disclosing financial status and history.

Many individuals neglect to clarify the terms of repayment. It's essential to know not just the amount to be repaid, but the schedule, interest rates, and any penalties for late payments. Failure to fully grasp these terms can lead to defaults or unnecessary financial strain.

Overlooking the need for a witness or notary signature is also a common oversight. Some agreements require official witnessing to ensure the document's validity and enforceability. Ignoring this step can render the entire agreement void or subject to dispute.

Not considering the need for legal advice is a mistake many make. While it might seem straightforward to fill out a Loan Agreement form, legal expertise can ensure that the agreement is fair and legally sound. Skimping on professional advice can lead to agreeing to unfavorable terms.

Ignoring the fine print is another pitfall. Important details are often hidden in the least obvious sections of a contract. By not scrutinizing the fine print, borrowers might unknowingly agree to terms that are disadvantageous.

Failing to consider the consequences of a breach of the agreement is a serious oversight. Understanding what happens if either party fails to meet their obligations is crucial. This knowledge can significantly influence decision-making and encourage compliance with the agreement's terms.

Not keeping a copy of the signed agreement is an error too often made. Both parties should have a copy of the agreement for their records. This ensures that there is proof of the terms agreed upon, which can be pivotal in resolving any future disputes.

Lastly, a significant mistake is not updating the agreement when circumstances change. Life is unpredictable, and changes to financial situations, contact information, or terms of the agreement might necessitate adjustments. Failure to reflect these changes in the agreement can lead to misunderstandings or legal challenges.

A Loan Agreement form is a critical document, formalizing the terms, conditions, and expectations between a lender and a borrower. However, to fully encapsulate all the aspects of a lending transaction, several other forms and documents are often used in conjunction. These documents help in detailing the specifics of the loan, ensuring the security of the involved parties, and fulfilling legal requirements.

Together with the Loan Agreement, these documents form a comprehensive framework that manages the expectations and responsibilities of both parties. They provide clarity and legal grounding, making sure the lending process is fair, transparent, and accountable.

A Promissory Note is quite similar to a Loan Agreement as both serve as written promises to pay a certain amount of money. The key similarity lies in their function to outline the specifics of the loan's terms, including the amount borrowed, interest rate, and repayment schedule. However, a Promissory Note is usually more simplistic and might not include the comprehensive legal protections and detailed conditions that a Loan Agreement typically offers.

A Mortgage Agreement shares characteristics with a Loan Agreement, especially in the context of loans used to purchase real estate. In both documents, the borrower agrees to repay the borrowed amount under specified conditions. The significant difference is that a Mortgage Agreement specifically involves a secured loan that is protected by collateral, usually the property being purchased. This means if the borrower fails to make timely payments, the lender has the right to take ownership of the property.

The concept of a Line of Credit Agreement parallels a Loan Agreement in that both provide access to funds under agreed-upon terms. A Line of Credit Agreement, however, offers flexibility that a traditional Loan Agreement might not. It allows the borrower to draw funds up to a specified limit over a period, repay, and then borrow again, which is useful for ongoing expenses rather than a one-time lump sum need.

A Deed of Trust is another document similar to a Loan Agreement but with a unique structure involving three parties: the borrower, the lender, and a trustee. Like a Mortgage Agreement, it's used in financing real estate. The borrower transfers the property title to the trustee until the loan is fully repaid. This arrangement provides security to the lender that the loan will be repaid, or the property can be sold to recover the loan amount.

Credit Agreement forms share the foundational purpose with Loan Agreements, in that they enable a borrower to access funds from a lender. These are typically more detailed and complex, covering extensive terms of credit usage, repayment, and interest rates. Credit Agreements are commonly used in commercial lending and can encompass revolving credit lines, term loans, or letters of credit, offering businesses the capital needed for operations or expansion.

An Equipment Financing Agreement is specifically tailored for loans used to purchase equipment. Like a Loan Agreement, it outlines the amount of the loan, interest rate, repayment schedule, and any collateral involved - often the equipment itself. This specificity ensures both parties are clear about the terms, especially regarding what happens if the borrower cannot make payments, including repossession of the equipment.

A Student Loan Agreement is focused on loans provided for educational purposes. It shares similarities with a general Loan Agreement regarding the need to specify the loan amount, interest rate, and repayment terms. However, it often contains provisions related to deferment periods, grace periods after graduation, and sometimes options for loan forgiveness, which are particular to the context of student loans.

The concept of a Guaranty is closely related to that of a Loan Agreement, wherein it adds an extra layer of security for the lender. A Guaranty involves a third party, the guarantor, who agrees to repay the loan if the original borrower fails to do so. This document complements a Loan Agreement by providing additional assurance that the loan will be repaid, thus minimizing the lender's risk.

A Lease Agreement, while primarily known for its role in renting property or equipment, shares the concept of periodic payments and specific terms with a Loan Agreement. Both documents delineate responsibilities, terms, and conditions that the borrower or lessee must adhere to. In a Lease Agreement, instead of repaying a loan, the lessee makes regular payments to use or occupy the lessor's property or equipment.

When navigating the complexities of filling out a Loan Agreement form, individuals stand at a critical juncture that requires meticulous attention to detail and a full understanding of the implications of their commitments. The successful completion of this document hinges on a balanced approach of acknowledging what should be embraced and what must be avoided. Below are vital pointers to guide one through this process.

Things You Should Do:

Things You Shouldn't Do:

Understanding the intricacies of a Loan Agreement is crucial for both lenders and borrowers. Misconceptions can lead to misunderstandings and could potentially impact the relationship between the two parties. Here are six common misconceptions about the Loan Agreement form:

A Loan Agreement form is essential in formalizing the obligations and expectations between a lender and a borrower. Here are the key takeaways to keep in mind while filling out and using such a form:

Using a Loan Agreement form is a proactive step towards protecting the interests of both the lender and the borrower. It ensures that there is a legally binding document that lays out the terms of the loan and any obligations expected from both parties. When filled out carefully and thoroughly, it serves as a safeguard against misunderstandings and potential legal disputes in the future.

How to Write Up a Bill of Sale for a Boat - Completing the form accurately is crucial to avoid delays or issues with registering or using the boat.

What Are Constating Documents - Filling out the Articles of Incorporation accurately is paramount, as it impacts legal standing, taxation, and the ability to raise capital.