Blank IOU Template

Blank IOU Template

An IOU form is a straightforward document that plays a crucial role in personal and business finances. It serves as a tangible acknowledgment of debt, clearly stating that one party owes another a specified amount of money. This form, simple yet powerful, is often used to ensure clarity and prevent misunderstandings between the involved parties. By detailing the amount owed, the names of the parties in question, and the repayment terms, an IOU provides a clear path towards resolution of debt. Despite its informal appearance when compared to more complex legal agreements, an IOU holds significant weight in many scenarios, offering a level of flexibility and simplicity appreciated by lenders and borrowers alike. It's a testament to the idea that sometimes, the simplest forms of agreement are the most effective in facilitating smooth financial transactions and establishing trust.

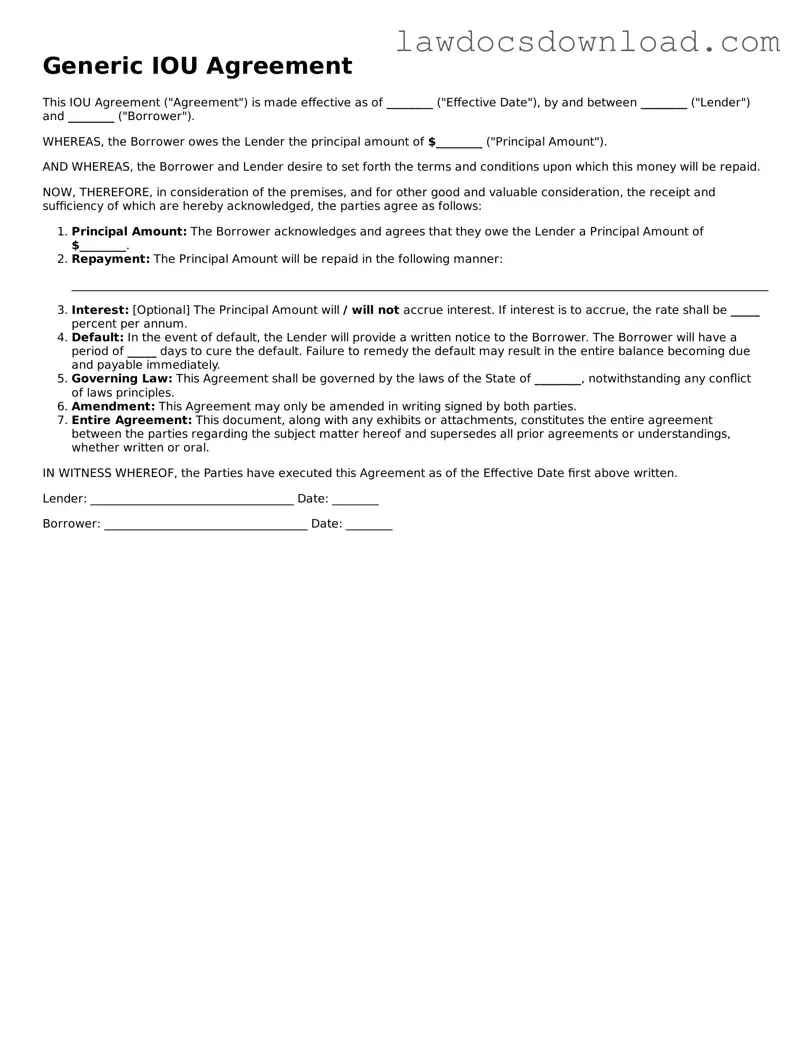

Generic IOU Agreement

This IOU Agreement ("Agreement") is made effective as of ________ ("Effective Date"), by and between ________ ("Lender") and ________ ("Borrower").

WHEREAS, the Borrower owes the Lender the principal amount of $________ ("Principal Amount").

AND WHEREAS, the Borrower and Lender desire to set forth the terms and conditions upon which this money will be repaid.

NOW, THEREFORE, in consideration of the premises, and for other good and valuable consideration, the receipt and sufficiency of which are hereby acknowledged, the parties agree as follows:

________________________________________________________________________________________________________________________

IN WITNESS WHEREOF, the Parties have executed this Agreement as of the Effective Date first above written.

Lender: ___________________________________ Date: ________

Borrower: ___________________________________ Date: ________

| Fact | Detail |

|---|---|

| Definition | An IOU form is a document that acknowledges a debt owed by one party to another. |

| Key Components | An IOU typically includes the amount owed, the parties involved, and the repayment date. |

| Legality | IOUs are legally binding in most jurisdictions, provided they meet the essentials of a contract. |

| Use Cases | They are commonly used for personal loans, informal borrowing, or business transactions. |

| Enforcement | Although enforceable, recovering debts under an IOU may require legal action. |

| Governing Laws | State-specific laws may influence the enforceability and terms of an IOU, including statutes of limitations on debt. |

| Notarization | Notarization is not a requirement but can add a level of authenticity and help in enforcement. |

When you borrow money or items from someone, it's common practice to acknowledge the debt in writing. An IOU (I Owe You) form serves this purpose by creating a clear, written promise to repay the lender. Although the form doesn't detail repayment conditions like a more formal contract, it still acts as a strong personal commitment. Below you will find straightforward steps to properly fill out an IOU form. This will ensure both parties understand the agreement and provide a record of the debt.

Filling out an IOU form is a straightforward way to recognize a debt. While simple, it serves as a personal reminder and a record that can help avoid any confusion or disputes about the agreement later on. Following these steps ensures that the form is completed correctly and reflects the agreement between the lender and the borrower accurately.

What is an IOU form?

An IOU form is a simple document that records a loan between two parties. It acknowledges that one party owes another a certain amount of money. While it might not be as complex as a formal loan agreement, it serves as a clear reminder and evidence of the debt.

Does an IOU form need to be notarized to be valid?

Generally, an IOU form does not need to be notarized to be valid. The critical component is that it clearly states the amount owed and both parties' names. However, getting it notarized can add an extra layer of verification and may help in enforcing the document.

Can an IOU form include interest rates?

Yes, an IOU can include interest rates. If both parties agree to have the loan amount accrue interest, this should be clearly stated in the IOU form along with the interest rate and how it will be calculated.

Is an IOU legally enforceable?

Yes, an IOU is legally enforceable. As a document that records the details of a loan and the agreement between two parties, it can be used in court to prove that the debt exists. However, the enforceability can depend on the specific details included in the IOU and the laws of your state.

What should be included in an IOU form?

Can an IOU be used between businesses?

Yes, an IOU can be used between businesses. It works similarly as it does between individuals, acknowledging a debt owed from one business to another. It's crucial for businesses to keep detailed records, and an IOU can serve as part of these financial documents.

How can you ensure an IOU is taken seriously by the borrower?

To ensure an IOU is taken seriously, both parties should discuss and agree on all terms before signing. It helps to have clear repayment terms and conditions outlined. Sometimes, having a witness present during signing or getting the document notarized can also underline its seriousness.

What happens if the borrower refuses to pay back as agreed?

If the borrower refuses to pay back the loan as agreed, the lender may have the option to take legal action. The IOU serves as evidence of the agreement and the debt. Legal proceedings can be initiated to enforce repayment, although it's always recommended to try and resolve the matter privately first.

Are there any alternatives to an IOU if you need a formal loan document?

Yes, if you're looking for something more formal than an IOU, you might consider a promissory note or a personal loan agreement. Both of these documents can also include the details of the loan, such as the repayment schedule and interest rates, and are legally binding. They tend to be more detailed and may provide better protection and clarity for both parties.

Filling out an IOU form might seem straightforward, but errors are common and can have significant ramifications. One major mistake is leaving sections of the form blank, assuming they are not applicable. This oversight can create ambiguities about the terms, making the agreement harder to enforce. It’s crucial to provide complete information, so both parties clearly understand the agreement’s scope and conditions.

Another frequent error involves unclear repayment terms. Often, individuals jot down the amount borrowed but neglect to specify the repayment schedule or deadline. This lack of clarity can lead to misunderstandings and disputes about when the debt should be fully repaid. To prevent such issues, it's essential to detail the repayment terms, including exact dates and amounts for each installment, if applicable.

Failing to include the interest rate, or not specifying whether the loan is interest-free, is also a common mistake. Including this information is vital, especially if the lender expects interest on the borrowed amount. Without an agreed-upon interest rate documented on the form, calculating the total amount owed can become a point of contention.

Lastly, neglecting to have the IOU form witnessed or notarized can undermine its enforceability. While not always a legal requirement, having a third-party witness or a notary public sign the document can add an extra layer of validity. It serves to confirm that both the lender and borrower entered into the agreement willingly and understood its terms. In disputes, this can be a critical piece of evidence to uphold the agreement's terms.

When individuals enter into financial transactions that involve borrowing or lending money, an IOU form serves as a straightforward document to confirm the transaction details. However, to bolster the agreement and cover broader legal and financial aspects, other forms and documents are often used in conjunction. These supplementary documents can greatly enhance the clarity and enforceability of the financial agreement, ensuring that both parties have a comprehensive understanding of their rights and responsibilities.

Together, these documents can provide a robust legal framework around financial transactions, offering protection and clarity for all parties involved. They help to ensure that each party's interests are safeguarded, and they can make the resolution of disputes more straightforward, should they arise. By complementing an IOU with these relevant forms and documents, individuals can navigate their financial arrangements confidently and securely.

The Promissory Note is a close relative of the IOU form, sharing its nature as a written promise. Unlike the simple statement of an IOU, which might just say "I owe you," a Promissory Note details the specifics: who owes whom, how much, and the repayment terms. This document is more formal, often used for loans that require a structured repayment schedule.

A Loan Agreement shares similarities with an IOU in that both outline a borrower's debt to a lender. However, the Loan Agreement is much more comprehensive. It includes not only the amount and acknowledgment of the debt but also interest rates, repayment schedule, collateral if any, and the consequences of non-payment. This makes the Loan Agreement a go-to document for substantial loans between parties seeking a legally binding arrangement.

A Bill of Sale is like an IOU in the sense that it acknowledges a transaction between two parties. While an IOU indicates that one party owes another, a Bill of Sale confirms that a sale took place, specifying what was sold and at what price. It serves as proof of ownership transfer, which is especially important for the sale of high-value items like vehicles or real estate.

The Mortgage Agreement is another document related to the IOU. It specifically relates to borrowing money to purchase real estate, with the property itself serving as collateral for the loan. The agreement outlines the loan's terms, including payments and interest rates, much like an IOU outlines the basic details of a debt. However, its focus on real estate transactions and the inclusion of legal claims on the property if the loan isn't repaid distinguish it.

A Credit Agreement resembles an IOU in documenting a debt. This agreement is broader and more detailed, covering the terms under which credit is extended by a lender to a borrower. This can include revolving credit lines, like credit card agreements, or term loans, where the document delineates repayment schedules, interest rates, and what happens if the borrower fails to make payments.

The Receipt is a document that, like an IOU, acknowledges a transaction. But while an IOU signifies a promise to pay, a receipt verifies that payment was made. This is essential for both parties as proof of purchase or payment, serving to prevent disputes over whether a debt has been settled.

A Lease Agreement, while primarily used for the rental of property, shares the IOU's essence of a financial obligation between two parties. The lessee agrees to pay the lessor for the use of property, equipment, or other assets for a specified period. Though it's more detailed, covering terms like rent, security deposit, and maintenance responsibilities, its core is similar to an IOU's promise of payment.

The Bond is a fixed income instrument that functions similarly to an IOU in that it represents a loan made by an investor to a borrower (typically corporate or governmental). A bond details the loan terms, including the due date and the interest the borrower will pay to the bondholder. It's a more formal and regulated way of acknowledging debt than an IOU.

An Equity Agreement, while involving ownership rather than debt, can be similar to an IOU in that it represents a financial arrangement between parties. In this case, an investor provides capital to a business in exchange for equity, or a share of ownership, anticipating a return on investment. Though it doesn't represent a debt, it's a formal acknowledgement of a financial obligation undertaken by the business towards the investor.

When filling out an IOU (I Owe You) form, it's important to follow specific guidelines to ensure that the document is legally binding and clear to all parties involved. Here are some essential dos and don'ts:

When dealing with IOU forms, misunderstandings can arise, leading to confusion and potential legal complications. It's important to address these misconceptions to ensure both parties understand the commitment they are making. Below is a list of nine common misconceptions about the IOU form:

An IOU is not legally binding: Contrary to popular belief, an IOU is a legally binding agreement. It indicates that one party owes a debt to another and is obligated to repay it. However, for it to hold up in court, it must be detailed and clear.

IOUs must involve large sums of money: There is no minimum amount for an IOU. It can document any amount, large or small, as long as both parties agree on the figure. The key is the acknowledgment of the debt, not the amount.

Interest cannot be added to an IOU: Interest can be included in an IOU, but it must be specified in the agreement. Both the lender and borrower should agree on the interest rate, and it should be documented within the IOU.

Only the borrower needs to sign the IOU: While it's crucial for the borrower to sign the IOU to acknowledge their debt, having the lender sign the document can also provide additional proof of the agreement and its terms.

IOUs must be notarized to be valid: Notarization is not a requirement for an IOU to be considered valid. However, having the document notarized can add a layer of verification and credibility, should it be needed in a legal dispute.

You cannot take legal action with only an IOU: If the borrower fails to repay the debt as agreed, the lender can take legal action to recover the funds based on the IOU. It serves as evidence of the debt and the terms agreed upon by both parties.

All IOUs are the same: There is no one-size-fits-all IOU. Each agreement should be tailored to the specific terms and conditions agreed upon by the parties, including the amount, repayment schedule, interest, and any other relevant details.

An IOU cannot replace a formal contract: While IOUs are simpler than formal contracts, they serve a similar purpose in documenting an agreement between two parties. However, for more complex transactions, a more detailed contract may be necessary.

An IOU cannot be modified once signed: If both parties agree, an IOU can be amended. Any modifications should be documented, signed by both parties, and attached to the original IOU to ensure clarity and legal standing.

Understanding these points can help individuals navigate the use of IOUs more effectively, ensuring that these agreements are treated with the seriousness they deserve while also safeguarding the interests of both parties involved.

When it comes to financial matters between individuals, clarity and documentation are crucial. An "IOU" form, which stands for "I Owe You," serves as a simple but formal acknowledgment of debt from one party to another. It's a tool that can prevent misunderstandings and legal disputes down the road. Here are some key takeaways about filling out and using the IOU form correctly.

Ultimately, an IOU form is more than just a piece of paper; it's a formal commitment that safeguards both the lender and borrower's interests. When filled out thoughtfully and with the necessary detail, it can prevent many common misunderstands and disputes over money between friends, family, or business associates.

Family (Friends) Personal Loan Agreement - Acts as a formal commitment between parties to ensure the borrower repays the loan to the lender.