Legal Georgia Promissory Note Form

Legal Georgia Promissory Note Form

In the state of Georgia, individuals seeking to solidify a loan agreement have at their disposal a critical legal instrument known as the Georgia Promissory Note form. This document, pivotal in its function, serves as a binding agreement between the borrower and lender, setting out the terms under which money is to be borrowed and repaid. Details such as the interest rate, payment schedule, amount borrowed, and consequences of default are meticulously outlined within this form, ensuring clarity and mutual understanding between the involved parties. Recognized under Georgia's legal framework, the promissory note not only fosters trust between the borrower and lender but also affords legal protection to both. By meticulously documenting the loan's specifics, this comprehensive form plays a fundamental role in personal and business finance transactions within the state, making it a staple in the realm of financial agreements.

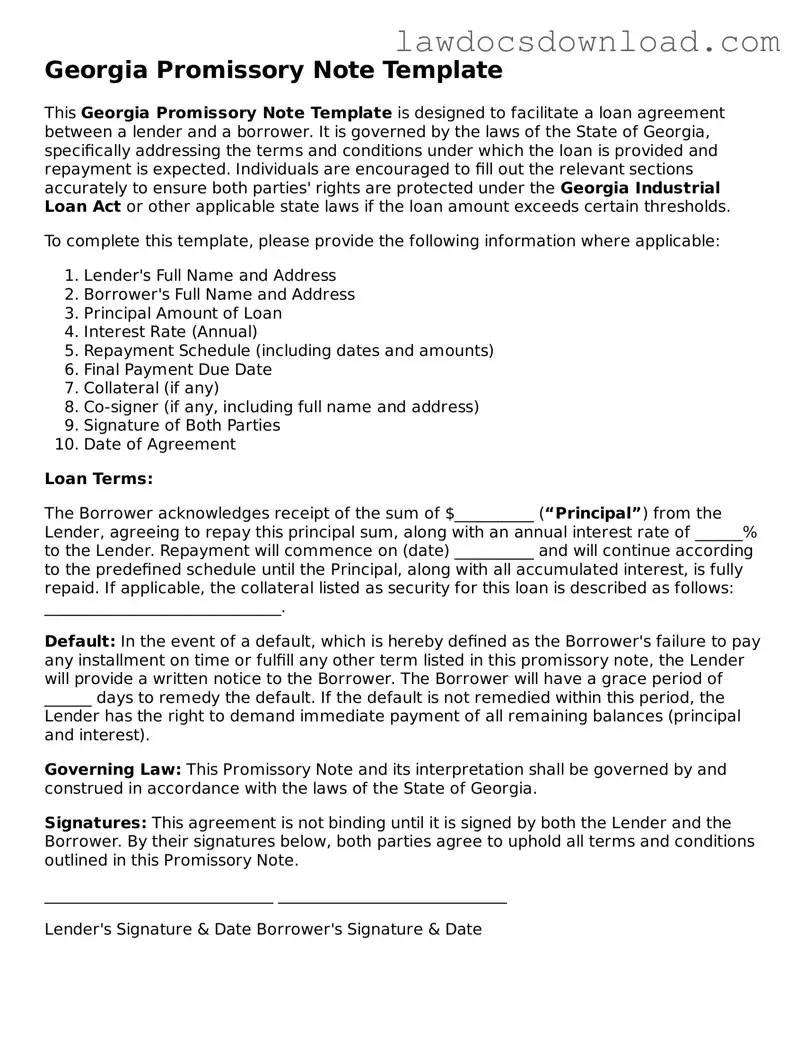

Georgia Promissory Note Template

This Georgia Promissory Note Template is designed to facilitate a loan agreement between a lender and a borrower. It is governed by the laws of the State of Georgia, specifically addressing the terms and conditions under which the loan is provided and repayment is expected. Individuals are encouraged to fill out the relevant sections accurately to ensure both parties' rights are protected under the Georgia Industrial Loan Act or other applicable state laws if the loan amount exceeds certain thresholds.

To complete this template, please provide the following information where applicable:

Loan Terms:

The Borrower acknowledges receipt of the sum of $__________ (“Principal”) from the Lender, agreeing to repay this principal sum, along with an annual interest rate of ______% to the Lender. Repayment will commence on (date) __________ and will continue according to the predefined schedule until the Principal, along with all accumulated interest, is fully repaid. If applicable, the collateral listed as security for this loan is described as follows: ______________________________.

Default: In the event of a default, which is hereby defined as the Borrower's failure to pay any installment on time or fulfill any other term listed in this promissory note, the Lender will provide a written notice to the Borrower. The Borrower will have a grace period of ______ days to remedy the default. If the default is not remedied within this period, the Lender has the right to demand immediate payment of all remaining balances (principal and interest).

Governing Law: This Promissory Note and its interpretation shall be governed by and construed in accordance with the laws of the State of Georgia.

Signatures: This agreement is not binding until it is signed by both the Lender and the Borrower. By their signatures below, both parties agree to uphold all terms and conditions outlined in this Promissory Note.

_____________________________ _____________________________

Lender's Signature & Date Borrower's Signature & Date

| Fact Number | Description |

|---|---|

| 1 | In Georgia, a promissory note is a legal agreement for borrowing money. |

| 2 | It must include the amount borrowed, interest rate, and repayment terms. |

| 3 | Georgia's legal interest rate is 7%; however, parties can agree to a higher rate in writing. |

| 4 | If interest exceeds the state's usury limits, it may be considered illegal. |

| 5 | Georgia promissory notes can be either secured or unsecured. Secured notes require collateral. |

| 6 | Upon default, lenders may take legal action to recover the borrowed amount and interest due. |

| 7 | Governing laws for promissory notes in Georgia are found in the Official Code of Georgia Annotated (O.C.G.A.). |

After completing the Georgia Promissory Note form, you will have created a legally binding agreement for borrowing and repaying a sum of money. The next steps include ensuring all parties understand their responsibilities and rights under this agreement. To successfully fill out the form, follow these instructions carefully. Each section requires accurate information to protect all parties involved and guarantee clear communication of the loan terms.

By following these steps carefully, you will have completed the Georgia Promissory Note form effectively. This document serves as a critical record of the loan and its terms, providing protection and clarity for both the lender and the borrower. Remember, it's always advisable for both parties to review the completed document together before signing, ensuring mutual understanding and agreement.

What is a Georgia Promissory Note?

A Georgia Promissory Note is a written agreement to pay back a loan. This document is legally binding in Georgia and outlines the terms of repayment, including the loan amount, interest rate, repayment schedule, and the obligations of both the borrower and lender.

Is a written Promissory Note required in Georgia?

While verbal agreements may be legally enforceable, a written Promissory Note is strongly recommended to provide clarity and legal protection for both parties. In Georgia, a written Promissory Note is invaluable in case of disputes or if the matter goes to court.

What information should be included in a Georgia Promissory Note?

How can interest rates be determined for a Georgia Promissory Note?

In Georgia, the legal maximum interest rate, unless otherwise agreed upon, is 7% per annum for written contracts. When an interest rate is agreed upon, it should not surpass the legal state limits to avoid being considered usurious. The parties can agree to any rate as long as it conforms with state law.

What types of Promissory Notes are there in Georgia?

What happens if the borrower does not repay the loan as promised?

If a borrower defaults on a Georgia Promissory Note, the lender has the legal right to demand immediate full payment of the remaining loan balance. For secured loans, the lender may also seize the collateral. Legal action may be pursued to enforce the note and recover the owed amount.

Can the terms of a Georgia Promissory Note be modified?

Yes, the terms of a Promissory Note can be modified, but any changes must be agreed upon by both the borrower and lender. It's best practice to document any amendments in writing and have both parties sign the updated agreement.

Is a witness or notarization required for a Georgia Promissory Note to be legal?

While not always legally required, having a witness or notarizing the document can add a level of validation and can be helpful if the note is ever contested in court. It's advisable to consider these steps to further solidify the agreement's legal standing.

How can a Georgia Promissory Note be enforced if the borrower refuses to pay?

In the event a borrower refuses to pay, the lender may file a lawsuit to enforce the note. Collecting on the debt may involve court judgment, wage garnishment, or seizing assets, depending on whether the note is secured or unsecured. Consulting with a legal professional in Georgia can provide guidance tailored to the specific situation.

Filling out a Georgia Promissory Note form can seem straightforward, but it's easy to make mistakes if you're not paying close attention. One common mistake people make is not specifying the interest rate clearly. In Georgia, if the interest rate is not stated, the implication might be that no interest is intended to be charged. However, under Georgia law, a legal rate of interest applies if none is specified, which might not align with the lender's intentions. Ensuring that the interest rate is clearly outlined protects both parties by setting expectations from the start.

Another mistake involves not being detailed about the repayment schedule. Many people fill out the form with a vague idea of when payments should start and end, but neglect to consider the implications of not setting a specific schedule. It's important to detail the frequency of payments (monthly, quarterly, etc.), the amount of each payment, and when the first payment is due. This not only helps in keeping both parties on the same track but also prevents any misunderstandings that could lead to disputes or legal complications down the line.

Incorrectly listing the parties involved in the transaction is another error that can have significant repercussions. Sometimes, individuals forget to include their full legal names, or they might use nicknames or incomplete names. This lack of clarity can create confusion about who is legally bound by the agreement. For businesses, the correct legal entity should be listed, not just the operating name of the business. Accuracy in identifying the borrower and lender ensures that the legal document is enforceable and reduces the potential for challenges.

Lastly, overlooking the need for signatures and dates at the end of the form is a surprisingly common error. For a Georgia Promissory Note to be considered valid and legally binding, it must be signed and dated by both parties involved in the agreement. Skipping this step can render the entire agreement voidable, leaving the lender without legal recourse in the event of non-payment. It's a simple yet crucial part of the process that completes the agreement and formalizes the obligations of each party.

When dealing with financial transactions, particularly those involving loans or lending in Georgia, a Promissory Note form is a crucial document. However, to ensure the security of both the lender and the borrower, this form is often accompanied by other important documents. Each of these documents plays a vital role in detailing the terms, responsibilities, and obligations involved in the financial arrangement. Here, let's dive into some of the commonly used forms and documents that complement a Georgia Promissory Note form.

Together, these documents form a comprehensive framework that supports the financial arrangement detailed in a Georgia Promissory Note. By clearly laying out the rights and obligations of all parties involved, these documents help to mitigate risks and provide clarity, making for smoother financial transactions and relationships.

The Georgia Promissory Note form shares similarities with a Mortgage Agreement. Both documents are used in the context of borrowing and lending, but while a promissory note is essentially a promise to pay a sum of money under agreed conditions, the Mortgage Agreement goes a step further by securing the loan with the borrower's property. This gives the lender the right to foreclose on the property if the borrower fails to make the agreed payments, making the Mortgage Agreement a more secure form of lending agreement than a promissory note for the lender.

Loan Agreements also bear resemblance to promissory notes, given that both set forth the terms under which money is borrowed and must be repaid. However, loan agreements are typically more detailed and comprehensive. They include specific terms regarding the repayment schedule, interest rates, collateral (if any), and actions in case of default. In contrast, a promissory note might be simpler, focusing mainly on the promise to repay the sum lent, making it less comprehensive but easier for personal loans between individuals.

A Line of Credit Agreement is akin to a promissory note in that it establishes an understanding between lender and borrower regarding funds being lent. Nonetheless, a line of credit agreement differs by offering a revolving fund that the borrower can draw from, repay, and draw from again up to a maximum limit, over a set period of time. This flexibility in borrowing and repayment is distinct from the more static sum and repayment schedule usually defined in a promissory note.

IOU documents are less formal cousins of the promissory note. Both document an obligation to repay borrowed money, but the IOU is often more informal and might not include detailed terms such as repayment schedules or interest rates that are commonly found in promissory notes. Essentially, an IOU is an acknowledgment of debt without the complex stipulations that legally bind the parties to specific repayment conditions.

The Bill of Sale is another document that, although different in purpose, shares an underlying similarity with promissory notes. While a bill of sale confirms the transfer of ownership of an item from seller to buyer, a promissory note confirms the promise to repay a debt. Both play crucial roles in transactions but on different spectrums; one on the sale of tangible assets and the other on the lending of money.

Lastly, a Debt Settlement Agreement is somewhat a resolution to situations that might originally involve a promissory note. When a borrower is unable to fulfill the repayment terms as stipulated in a promissory note, a debt settlement agreement can be negotiated, which allows for the adjustment of repayment terms, possibly reducing the debt or modifying the repayment schedule. This document represents a renegotiated understanding between the lender and borrower to resolve debt under new terms.

When preparing a Georgia Promissory Note, it's crucial to approach the process with caution and precision. This document is a binding agreement between a borrower and lender, detailing the loan's repayment. To ensure clarity and avoid legal pitfalls, follow these guidelines:

Do:

Don't:

When it comes to handling financial agreements in Georgia, a Promissory Note is a critical document, but it's often surrounded by misunderstandings. Whether it's due to hearsay or the complicated nature of financial documents, many people find themselves tripping over myths about what a Promissory Note does and doesn't do. Let's clear the air and address some common misconceptions.

Understanding these points can greatly demystify the use and importance of Promissory Notes, making financial transactions smoother and more secure. Whether lending to a friend or entering into a business arrangement, a well-prepared Promissory Note is an indispensable tool in ensuring that both parties understand their rights and obligations.

When handling the Georgia Promissory Note form, individuals are confronted with a document of paramount importance. Bearing legal implications, this form serves a critical role in documenting a loan agreement between two parties. As such, meticulous attention to detail and adherence to specific guidelines are imperative to ensure the agreement is valid, enforceable, and serves its intended purpose without unintended consequences. The following key takeaways highlight essential aspects and guidelines for filling out and using this form effectively.

The Georgia Promissory Note form is an indispensable tool in documenting loan agreements. Proper completion and understanding of its terms and legal implications ensure clarity and enforceability, providing peace of mind for both the lender and the borrower. By following these takeaway points, individuals can navigate the complexities of the form more effectively, upholding the integrity of the agreement and ensuring compliance with Georgia law.

Promissory Note Template Utah - Creating a promissory note requires critical details: amount, interest, repayment schedule, and parties involved.

Blank Promissory Note - Promissory notes play a vital role in finance, often used for loans between individuals, businesses, or between individuals and institutions.