Legal Georgia Loan Agreement Form

Legal Georgia Loan Agreement Form

The Georgia Loan Agreement form stands as a crucial document for anyone embarking on the journey of either lending or borrowing money in the state of Georgia. This form not only delineates the terms and conditions of the loan in a clear-cut manner but also ensures that all parties involved have a mutual understanding of their obligations and rights. It serves as a legal testament to the loan's existence, specifying the loan amount, repayment schedule, interest rates, and any collateral involved. Furthermore, in the event of a dispute or misunderstanding, it provides a foundation for resolution, thereby safeguarding the interests of both the lender and the borrower. Crafted to meet the specific legal requirements of Georgia, it helps in preventing potential legal pitfalls by setting a standardized procedure for the lending process, making it an indispensable tool for executing a secure and efficient transaction.

Georgia Loan Agreement Template

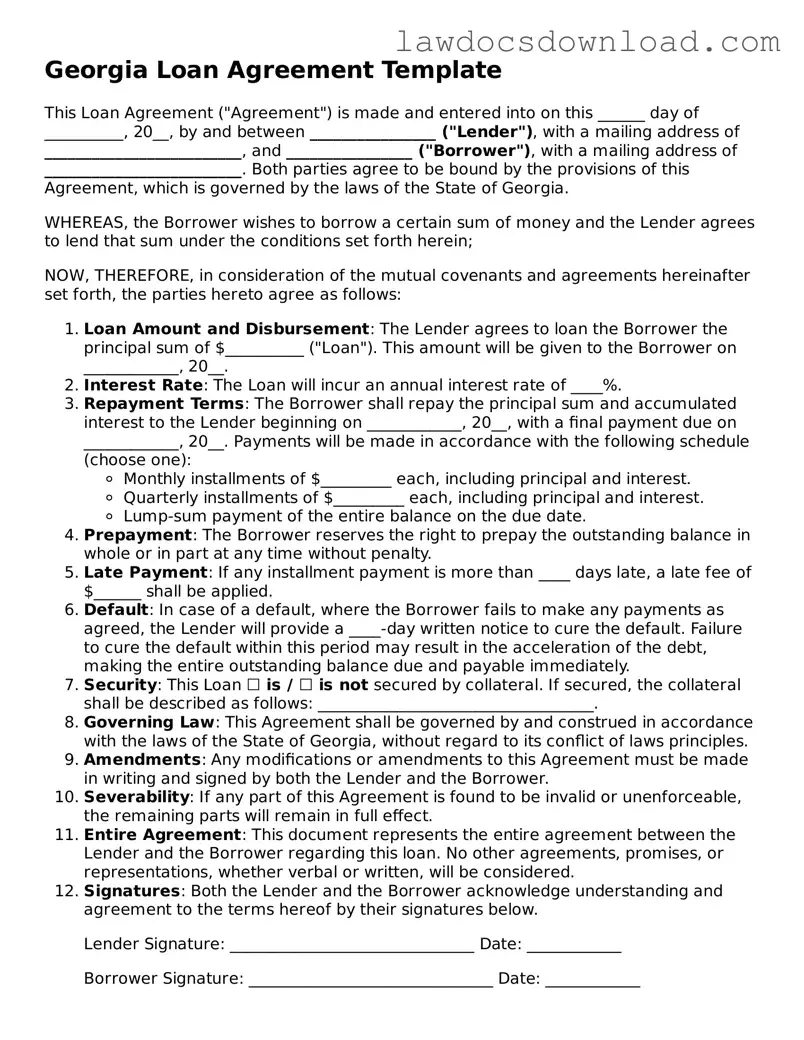

This Loan Agreement ("Agreement") is made and entered into on this ______ day of __________, 20__, by and between ________________ ("Lender"), with a mailing address of _________________________, and ________________ ("Borrower"), with a mailing address of _________________________. Both parties agree to be bound by the provisions of this Agreement, which is governed by the laws of the State of Georgia.

WHEREAS, the Borrower wishes to borrow a certain sum of money and the Lender agrees to lend that sum under the conditions set forth herein;

NOW, THEREFORE, in consideration of the mutual covenants and agreements hereinafter set forth, the parties hereto agree as follows:

Lender Signature: _______________________________ Date: ____________

Borrower Signature: _______________________________ Date: ____________

| Fact | Description |

|---|---|

| Governing Law | The Georgia Loan Agreement form is governed by the laws of the State of Georgia, including but not limited to, the Georgia Commercial Code and relevant federal laws. |

| Use | This form is used to outline the terms and conditions under which a loan is provided, including the repayment schedule, the interest rate, and the obligations of the borrower and lender. |

| Writing Requirement | In Georgia, most loan agreements must be in writing to be enforceable, especially those involving substantial amounts of money or complex terms. |

| Signatures | Both the lender and the borrower must sign the loan agreement form for it to be considered valid and binding under Georgia law. |

Completing a loan agreement form is a crucial step in formalizing the terms under which one party is borrowing money from another. In Georgia, like in many jurisdictions, a well-drafted loan agreement outlines the responsibilities and obligations of both the lender and the borrower. It provides a legal framework that protects the interests of both parties, establishing clear parameters for the repayment schedule, interest rates, and what happens in the event of a default. The following steps are designed to guide individuals through the process of filling out such a form, ensuring that all necessary details are accurately captured.

Once the form is fully completed and signed, the loan agreement becomes a legally binding document that holds both the lender and the borrower accountable to the terms outlined within it. It serves as a clear record of the loan, offering protection and clarity for both parties throughout the duration of the loan term. Proper completion and understanding of the agreement can help prevent misunderstandings and disputes, reinforcing a mutually beneficial relationship between lender and borrower.

What is a Georgia Loan Agreement form?

A Georgia Loan Agreement form is a legal document that outlines the terms and conditions under which a loan will be extended by a lender to a borrower in the state of Georgia. This agreement specifies the loan amount, interest rate, repayment schedule, and any other relevant details pertaining to the loan.

Who needs to sign the Georgia Loan Agreement form?

Both the lender and the borrower must sign the Georgia Loan Agreement form. Witnesses or a notary public may also be required to sign, depending on the complexity of the loan and the preferences of the parties involved.

Is a notary required for a Georgia Loan Agreement?

While not always mandatory, having a notary public witness the signing of a Georgia Loan Agreement can add a level of legal verification and can be beneficial in enforcing the terms of the agreement, should disputes arise.

What information should be included in a Georgia Loan Agreement form?

The form should include:

How can one ensure the agreement is legally binding?

To ensure the Georgia Loan Agreement is legally binding, all parties should provide accurate information and sign the document. Getting it notarized can also strengthen its legality. It’s advised to have a legal professional review the agreement before it is signed.

Can the terms of a Georgia Loan Agreement be modified?

Yes, the terms of a Georgia Loan Agreement can be modified if both the lender and borrower agree to the changes. Any modifications should be documented in writing and signed by both parties, with witnesses or a notary present as needed.

What happens if a borrower defaults on the loan?

If a borrower defaults on the loan, the lender has the right to pursue legal action to recover the owed amount. If collateral was included in the agreement, the lender might also have the right to seize the collateral. The specific consequences should be clearly outlined in the agreement itself.

Are electronic signatures valid on a Georgia Loan Agreement?

Yes, electronic signatures are generally recognized as valid under Georgia law for most types of agreements, including loan agreements. However, verify that the electronic signing method used complies with federal and state regulations.

Where can one get help drafting a Georgia Loan Agreement?

Drafting a Georgia Loan Agreement should ideally involve legal counsel to ensure that all terms are properly outlined and that the document complies with Georgia laws. Legal professionals can provide guidance, or one may use reputable legal document services that offer customizable templates.

One common mistake when filling out the Georgia Loan Agreement form is not providing complete information about the parties involved. This includes the full legal names of both the borrower and the lender, as well as their addresses. Incomplete information can lead to misunderstandings and legal issues. It's crucial that every detail requested about parties in the agreement is fully and accurately provided.

Another error often made involves the terms of the loan. Sometimes, individuals forget to clearly state the loan amount, interest rates, repayment schedule, and the loan’s maturity date. These elements are vital as they define the obligations of the borrower and the rights of the lender. Without clear terms, disputes and complications can easily arise.

The omission of the loan's purpose is also a frequent oversight. Specifying the reason for the loan in the agreement helps in maintaining transparency between the borrower and lender. This detail can also be important for legal and tax purposes, affecting how the loan may be perceived by external parties.

Many individuals neglect to include clauses that outline the procedure in the event of a default by the borrower. It is essential to have predefined consequences if the borrower fails to meet their repayment obligations. Not having these terms can make it difficult for the lender to recover the loaned amount.

Incorrect or missing signatures is a critical mistake that can render the agreement unenforceable. Both parties must sign the document, and in some cases, witness signatures may also be required for it to be legally binding. Ensuring that all necessary signatures are present is fundamental for the agreement’s validity.

Finally, not consulting a legal professional for advice or review of the document can lead to errors or omissions that might compromise the agreement’s enforceability. While it may seem straightforward, the legal nuances of loan agreements necessitate professional guidance to avoid mistakes that could have significant implications.

When entering into a loan agreement in Georgia, various additional forms and documents often accompany the main agreement to ensure clarity, legality, and the protection of all parties involved. These documents serve a range of purposes, from verifying the identities of the parties to securing the loan with collateral. Understanding these accompanying forms can help the parties have a smoother lending experience.

Collectively, these forms and documents ensure that both the borrower and the lender are protected and that the terms of the loan are clearly defined and understood by all parties. Ensuring the proper completion and filing of these documents is crucial for a legally binding and enforceable agreement in Georgia.

The Georgia Loan Agreement form shares similarities with a Promissory Note. Both documents are binding agreements involving a lender and a borrower, where the borrower agrees to pay back a certain amount of money to the lender under specific conditions. A promissory note is more streamlined, focusing mainly on the repayment schedule and interest rates, lacking the detailed provisions about the borrower's obligations and rights that a loan agreement includes.

Mortgage Agreements have a notable resemblance to the Georgia Loan Agreement form, primarily because both secure loans with property. In a mortgage, the property acts as collateral in case the borrower defaults on the loan. The Georgia Loan Agreement might also include terms about securing the loan with collateral, detailing the obligations of the borrower to maintain the property and the rights of the lender to seize the property if the borrower fails to make payments as agreed.

The Line of Credit Agreement bears similarities to the Georgia Loan Agreement form. Both outline the terms under which money is borrowed, including interest rates, payment schedules, and the consequences of default. However, a Line of Credit Agreement differs by offering a revolving fund that the borrower can draw from, repay, and draw from again, up to a set limit, providing more flexibility than a conventional term loan as outlined in a typical loan agreement.

Personal Guarantee forms are related to the Georgia Loan Agreement form because they both deal with the assurance that a loan will be repaid. In a loan agreement, the borrower is directly responsible for repayment. A Personal Guarantee, however, involves a third party agreeing to repay the loan if the original borrower defaults, offering an additional layer of security to the lender that is not typically detailed in the loan agreement itself.

Debt Settlement Agreements share objectives with the Georgia Loan Agreement form, as both aim to outline the terms for handling a debt. While the loan agreement sets the original terms of the loan, a Debt Settlement Agreement comes into play when the borrower cannot meet those terms, offering a plan to settle the debt, usually by reducing the owed amount or altering repayment terms. This is a reactionary measure not anticipated in the original loan agreement but crucial for renegotiating terms when the borrower encounters financial difficulties.

Lastly, Business Loan Agreements and the Georgia Loan Agreement form are closely related, with the primary difference being that Business Loan Agreements are specifically tailored to the needs and considerations of businesses borrowing money. These agreements might include provisions for investments, operations, and the allocation of profits that are not typically found in personal or standard loan agreements. However, both documents define the relationship between borrower and lender, repayment terms, and the legal recourse available if either party fails to meet their obligations.

When filling out the Georgia Loan Agreement form, it's important to approach the task with attention to detail and clarity. To ensure that you complete this document correctly and efficiently, here are some essential dos and don'ts that will guide you through the process.

By following these guidelines, you'll contribute to a smoother, more efficient, and legally compliant process in completing the Georgia Loan Agreement form.

When it comes to preparing and understanding the Georgia Loan Agreement form, there are several misconceptions that can confuse borrowers and lenders alike. It's crucial to debunk these myths for a clear understanding of the obligations and rights of each party involved. Here's a list of common misunderstandings:

Understanding these misconceptions and ensuring that both parties have a clear and mutual comprehension of the agreement can help prevent conflicts and ensure a smoother lending process.

When it comes to processing and utilizing the Georgia Loan Agreement form, it's important to keep a few key points in mind to ensure everything is handled correctly. This document outlines the terms and conditions of a loan, typically between two parties. Here are several takeaways to consider:

By paying attention to these details, individuals can ensure that their Georgia Loan Agreement form is thorough, clear, and legally sound, providing a solid foundation for the financial transaction it represents.

Sample Promissory Note Florida - The document might include a warranty section, asserting the borrower's ability to repay the loan.

Promissory Note New York - A financial contract that binds the borrower to repay the loaned amount under agreed conditions, including any penalties for late payments.

Loan Agreement Template Texas - It provides a framework for negotiating the terms of the loan before the agreement is finalized.