Legal Florida Promissory Note Form

Legal Florida Promissory Note Form

In Florida, when individuals or entities agree on borrowing or lending money, a Florida Promissory Note form often becomes a crucial document in outlining the terms of the agreement. This form, while straightforward, holds significant legal importance as it clearly delineates the loan amount, interest rate, repayment schedule, and the consequences should the borrower fail to meet their obligations. Its role is not only to protect the lender by legally binding the borrower to repay the loan but also to provide a clear financial pathway for the borrower to follow, ensuring transparency and understanding for all parties involved. Whether the loan is between friends, family, or business associates, the Florida Promissory Note form serves as an essential tool for financial transactions, guiding both lenders and borrowers through the legal landscape of monetary exchange. Ensuring the form is correctly filled out and adhered to can prevent misunderstandings and potential legal disputes, emphasizing its value in personal and professional lending scenarios.

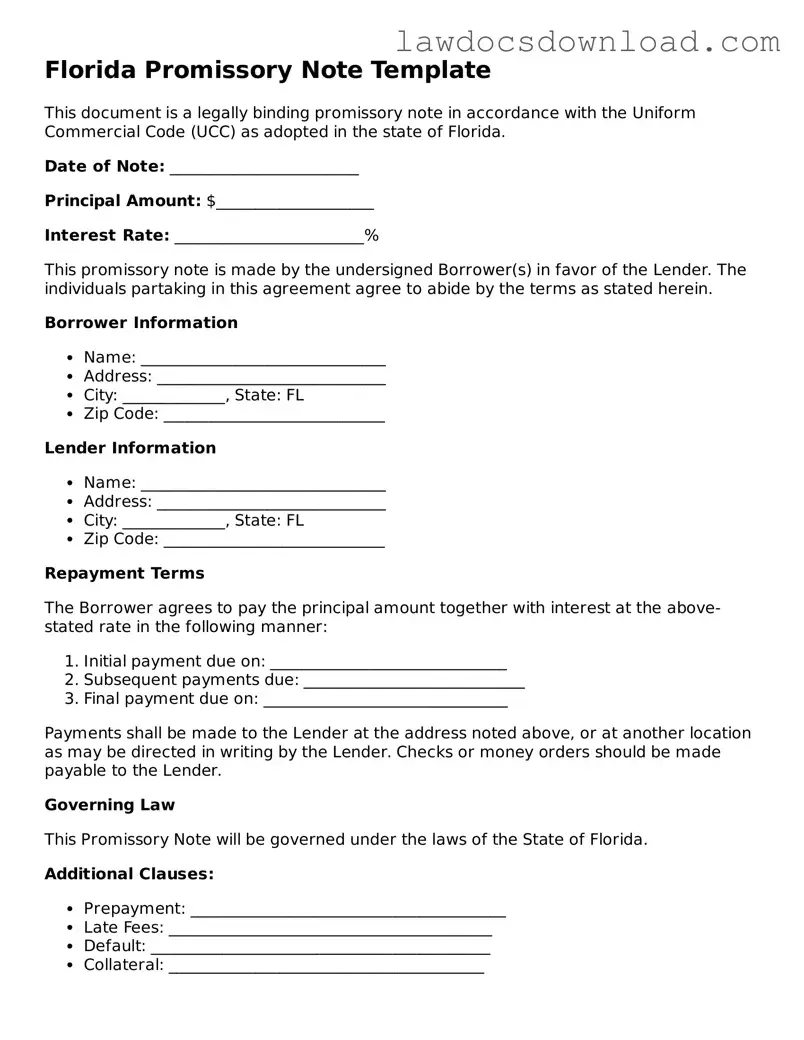

Florida Promissory Note Template

This document is a legally binding promissory note in accordance with the Uniform Commercial Code (UCC) as adopted in the state of Florida.

Date of Note: ________________________

Principal Amount: $____________________

Interest Rate: ________________________%

This promissory note is made by the undersigned Borrower(s) in favor of the Lender. The individuals partaking in this agreement agree to abide by the terms as stated herein.

Borrower Information

Lender Information

Repayment Terms

The Borrower agrees to pay the principal amount together with interest at the above-stated rate in the following manner:

Payments shall be made to the Lender at the address noted above, or at another location as may be directed in writing by the Lender. Checks or money orders should be made payable to the Lender.

Governing Law

This Promissory Note will be governed under the laws of the State of Florida.

Additional Clauses:

In witness whereof, the parties have executed this Promissory Note as of the date first above written.

Borrower's Signature: _______________________________

Date: ______________________________________________

Lender's Signature: ________________________________

Date: ______________________________________________

| Fact | Description |

|---|---|

| 1. Definition | A Florida Promissory Note form is a legal document that outlines a promise to pay a sum of money from a borrower to a lender. |

| 2. Types | There are two main types: secured and unsecured. Secured notes are backed by collateral, while unsecured notes are not. |

| 3. Interest Rates | Interest rates must comply with Florida's usury laws to prevent illegal interest charges. |

| 4. Governing Law | The form and its enforcement are governed by the laws of the State of Florida. |

| 5. Signature Requirement | Both the borrower and the lender must sign the promissory note for it to be legally binding. |

| 6. Co-signer Provision | If required, a co-signer can also sign the note, providing additional security for the lender. |

| 7. Payment Schedule | The note must specify the payment schedule, including the amount, frequency, and number of payments. |

| 8. Prepayment | The terms may include provisions for prepayment, allowing the borrower to pay off the note early. |

| 9. Default and Remedies | In case of default, the note outlines the remedies available to the lender, which may include seizing collateral for secured loans. |

Filling out a Florida Promissory Note form correctly is key to ensuring that the agreement between the borrower and lender is legally binding. This document outlines the repayment plan for any sum of money that is borrowed. It is essential to complete this form with clear and accurate information to avoid any misunderstandings or legal issues down the line. The importance of this task requires careful attention to detail, but by following each step methodically, you will be able to prepare the document correctly. Here’s what you need to do next:

Once the Florida Promissory Note form is fully completed and signed, copies should be made and distributed to all parties involved. This document should then be stored in a secure place, as it serves as a legal agreement for the repayment of the loan and may be needed for future reference. Both the lender and borrower should adhere to the terms laid out in the promissory note to ensure a smooth financial relationship and to avoid legal complications.

What is a Florida Promissory Note?

A Florida Promissory Note is a legal document that records a loan agreement between two parties in the state of Florida. It outlines the amount of money borrowed, the interest rate if applicable, repayment schedule, and the obligations of both the borrower and the lender. This document serves as a binding agreement to ensure that the borrower repays the borrowed amount under the terms specified.

Are there different types of Promissory Notes in Florida?

Yes, in Florida, there are mainly two types of Promissory Notes: secured and unsecured. A secured promissory note requires the borrower to pledge an asset as collateral, which the lender can seize if the borrower fails to repay the loan. An unsecured promissory note does not require collateral, but it usually comes with a higher interest rate due to the increased risk for the lender.

What information needs to be included in a Florida Promissory Note?

Each component is crucial for making the promissory note enforceable and clear to both parties involved.

How can a Florida Promissory Note be enforced?

If a borrower fails to repay according to the terms of the note, the lender has the right to pursue legal action to enforce repayment. For secured loans, this could involve seizing the collateral. For unsecured loans, the lender may need to bring a lawsuit against the borrower to collect the owed amount. It is advisable for lenders to keep detailed records of any communications and attempts to collect the debt, as these can be important in court proceedings. Additionally, involving an attorney can help navigate the complexities of the legal process effectively.

Filling out a promissory note in Florida can seem straightforward, but it's all too easy to make mistakes that could later affect its enforceability or the terms of the agreement. One common issue is not clearly identifying the parties involved. It's important to use full, legal names, and accurate addresses to ensure there is no ambiguity over who the borrower and lender are. Without clear identification, the agreement might be challenging to enforce.

Another frequent mistake is vague payment terms. A promissory note should spell out the loan amount, interest rate, repayment schedule, and any late fees in detail. When these terms are not clearly defined, misunderstandings can arise, leading to disputes between the borrower and lender. For instance, failing to specify whether the interest rate is fixed or variable can lead to confusion over payment amounts as market conditions change.

Incomplete information about the collateral is also a common error. If the loan is secured, the promissory note needs to describe the collateral that secures the loan. Neglecting to detail this information can make it difficult for the lender to claim the collateral if the borrower defaults on the loan. The description of the collateral should be detailed enough to identify it unmistakably.

Skipping the inclusion of a cosigner, if one is part of the agreement, can invalidate the security of the loan. A cosigner provides an additional layer of assurance for the repayment of the loan, and their details must be included within the note. Omitting this information might leave the lender with limited options if the borrower fails to make payments.

Not specifying the governing state law is another oversight. Florida law may govern the note, but if this isn't stated explicitly, the agreement may be subject to the general principles of contract law, which could result in unexpected interpretations. Clearly stipulating that Florida law applies ensures that both parties are aware of the legal context of the agreement.

A common faux pas is not providing for a successor clause. Life is unpredictable, and the note should address what happens if the borrower or lender dies or becomes incapacitated. Without this clause, the promissory note might not reflect the intentions of the parties regarding succession and inheritance.

Also, people often forget to outline the conditions of loan acceleration. This is the lender’s right to demand the full repayment of the loan under specific circumstances, such as the borrower defaulting on payments. Not including this information can leave the lender without recourse in speeding up the repayment process if the borrower fails to comply with the terms.

Lastly, many people fail to have the document witnessed or notarized, underestimating the importance of this step. While not always legally required, having a promissory note witnessed or notarized can add a layer of verification and legitimacy, promoting trust between the parties and aiding in the enforcement of the note.

When entering into a financial agreement in Florida, the Promissory Note form is a crucial document. However, to ensure a comprehensive and secure transaction, several other forms and documents are often used in conjunction with it. These supportive documents help clarify the terms, provide additional legal protection, and outline the responsibilities of all parties involved.

Together, these documents form a framework that supports the initial Promissory Note, ensuring that all aspects of the loan are legally accounted for and understood by all parties. Utilizing these additional documents can help prevent misunderstandings and provide a clearer path to fulfilling the obligations set forth in the Promissory Note.

One document similar to the Florida Promissory Note is the Loan Agreement. This document outlines the terms and conditions under which a loan is provided, including the repayment schedule, interest rates, and the parties involved. Like a promissory note, a loan agreement is a binding contract that obligates the borrower to repay the lender. However, it is typically more detailed, covering aspects like collateral requirements and actions in case of default.

Another related document is the Mortgage Agreement. Primarily used in real estate transactions, this agreement secures a loan by using the property as collateral. In similarity to promissory notes, it involves a pledge to pay back a debt. But, a mortgage agreement also grants the lender a lien on the property, giving them the right to seize it if the borrower fails to meet their obligations.

The IOU (I Owe You) is a simpler, less formal version of a promissory note. It acknowledges that a debt exists and generally specifies who owes who, but may not include detailed repayment terms. Unlike more formal arrangements, an IOU might lack legal enforceability in certain situations due to its informal nature and lack of details.

The Debt Settlement Agreement is a document used when a debtor and creditor agree on reducing the amount owed and setting new terms for repayment. Similar to a promissory note in its aim to settle debts, this agreement differs by often involving negotiation to adjust the original debt terms, which can include waiving certain fees or reducing the principal amount.

A Bill of Sale, while often used to document the transfer of ownership for goods or personal property, can sometimes resemble a promissory note when it includes terms for deferred payments. In those cases, it specifies what is being sold, to whom, and under what payment conditions, thereby committing the buyer to paying the seller over time for the acquired item.

The Guaranty Agreement adds a third party to the equation, where someone agrees to be responsible for a debt if the original borrower defaults. This is similar to a promissory note's purpose of ensuring repayment. However, it brings in an additional layer of security for the lender, with another individual or entity guaranteeing the loan.

Lines of Credit agreements can also have similarities to promissory notes. They allow borrowers to draw funds up to a specified limit and pay interest on the amount drawn. Similar to promissory notes, they require the borrower to repay the borrowed amount. However, they offer more flexibility, permitting multiple draws and repayments within the agreed limit.

A Revolving Credit Agreement, much like a line of credit, offers a borrower the ability to borrow, repay, and borrow again up to a certain credit limit. While it shares the promissory note's fundamental commitment to repay, it is more complex and flexible, often used by businesses for operational funding.

The Credit Agreement is another finance document similar to the promissory note, typically used in more sophisticated lending transactions. It outlines the terms under which credit is extended, including repayment conditions, interest rates, and covenants. While it serves the same primary function of documenting a loan and its repayment, credit agreements are more detailed and tailored to complex financing arrangements.

When filling out the Florida Promissory Note form, it's crucial to approach the task with care to ensure the document is legally binding and clear to all parties involved. Here's a guide to help you navigate what you should and shouldn't do during this process.

Things You Should Do

Things You Shouldn't Do

When it comes to financing and loans in Florida, promissory notes are commonly used documents that outline the details of a loan between two parties. However, there are several misconceptions about the Florida Promissory Note form that can lead to confusion. Here's a list of 10 common misconceptions and the truths behind them:

All promissory notes are the same: It's a common belief that all promissory notes are generic and interchangeable. However, Florida has specific requirements that may differ from those of other states. It's important to use a form that complies with Florida law to ensure its enforceability.

Only banks can issue promissory notes: Many people think that only banks or financial institutions can issue promissory notes. The truth is, any individual or entity can issue a promissory note as long as the borrower agrees to the terms and both parties sign the document.

You don't need a lawyer to create a promissory note: While it's true that you can draft a promissory note without a lawyer, seeking legal advice ensures that the note complies with Florida laws and that all necessary provisions are included to protect both parties.

Promissory notes are only for long-term loans: Another misconception is that promissory notes are exclusively for long-term loan arrangements. In reality, they can be used for any duration of loan, from short-term loans to longer financial agreements.

Vocal agreements can substitute for a written note: While verbal agreements are legally binding in some contexts, a written promissory note is essential for loan agreements. It provides a clear record of the terms agreed upon by both parties and is easier to enforce in court.

Interest rates can be as high as agreed upon: It's mistakenly believed that parties can set any interest rate they choose. In Florida, the interest rate on a loan cannot exceed the maximum rate set by state law. Charging higher can lead to penalties and the note being deemed usurious.

A promissory note is the same as an IOU: Some confuse promissory notes with IOUs, but a promissory note is more detailed. It includes information about the interest rate, repayment schedule, and consequences of non-payment, making it a more formal and binding document.

Signing a promissory note means you give up your rights: There's a fear that signing a promissory note means relinquishing all your rights. In truth, a well-drafted note will balance the rights and obligations of the borrower and the lender, ensuring fairness for both sides.

Electronic signatures aren't valid on promissory notes: With advancements in technology, electronic signatures are becoming more common and are indeed valid on promissory notes in Florida, as long as they meet the state's requirements for electronic transactions.

No collateral means no promissory note: Finally, there's the belief that a promissory note cannot be issued if there's no collateral. Promissory notes can be secured or unsecured; having collateral is not a prerequisite for creating a valid note.

Understanding these misconceptions about the Florida Promissory Note form can help borrowers and lenders navigate their financial transactions with greater clarity and ensure that their agreements are legally valid and enforceable.

When dealing with the Florida Promissory Note form, it's essential to understand its purpose and how to use it properly. This document serves as a legal agreement between a borrower and a lender, outlining the terms under which a loan will be repaid. Whether you are the lender or the borrower, paying careful attention to the details within this form can help ensure a smooth financial transaction and prevent potential misunderstandings or disputes down the line.

Approaching the Florida Promissory Note form with diligence and understanding its components can help ensure a fair and transparent deal for involved parties. It's always recommended to review the form carefully and, if necessary, seek legal advice to clarify any uncertainties or to tailor the note to specific needs and situations.

Promissory Note Template New York - A versatile tool that can be tailored to various types of loans, from commercial to personal use.

Promissory Note Template Oregon - The document can be prepared with a fixed or variable interest rate, depending on the agreement between the parties.

Texas Promissory Note Template - For lenders, it provides a level of security and reassurance that the borrowed funds have a structured path to repayment.