Legal Florida Loan Agreement Form

Legal Florida Loan Agreement Form

If you're stepping into the realm of lending or borrowing money in Florida, understanding the Florida Loan Agreement form is essential. This legal document plays a pivotal role in formalizing the terms and conditions between a lender and a borrower, ensuring clarity and legal enforceability of the loan. Whether it's for a personal loan between family members or a more complex loan arrangement involving businesses, this form outlines critical aspects like the loan amount, interest rates, repayment schedule, and any collateral involved. Additionally, it addresses what happens if the borrower fails to meet the terms, such as late fees or legal actions. Given the legal and financial implications, both parties should carefully review and understand every element of the Florida Loan Agreement form before signing. It serves not only as a safeguard but also as a guide to ensure fair and transparent dealings, making it a cornerstone of financial transactions within the state.

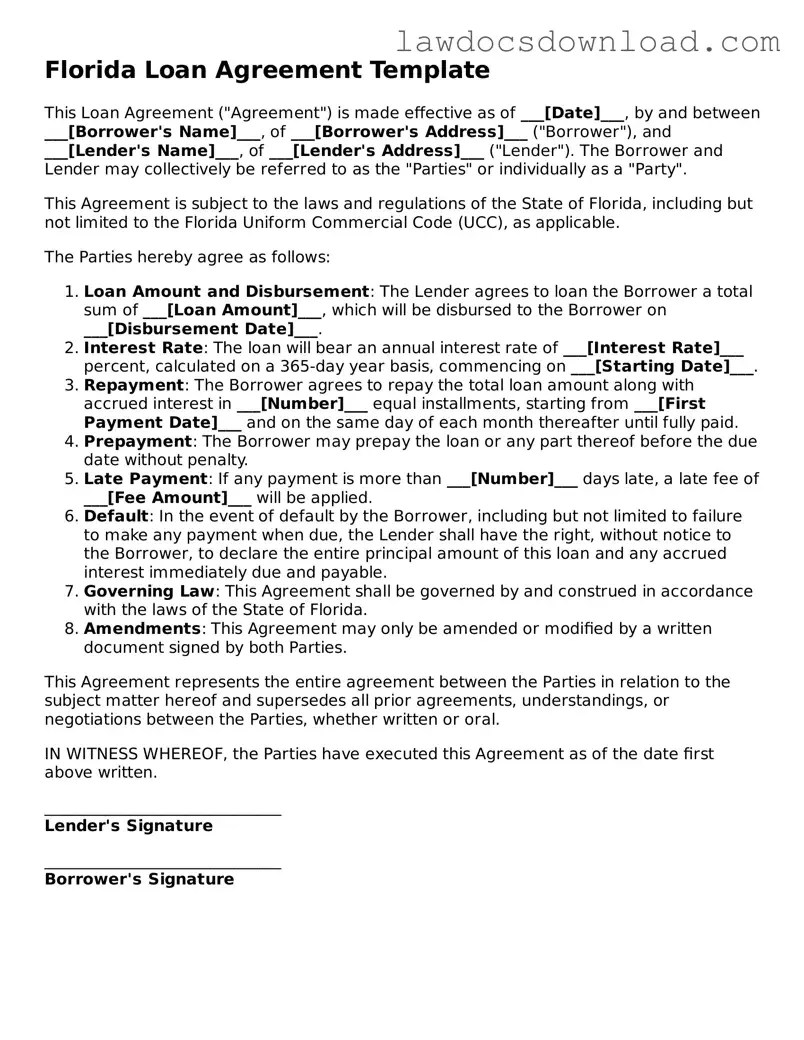

Florida Loan Agreement Template

This Loan Agreement ("Agreement") is made effective as of ___[Date]___, by and between ___[Borrower's Name]___, of ___[Borrower's Address]___ ("Borrower"), and ___[Lender's Name]___, of ___[Lender's Address]___ ("Lender"). The Borrower and Lender may collectively be referred to as the "Parties" or individually as a "Party".

This Agreement is subject to the laws and regulations of the State of Florida, including but not limited to the Florida Uniform Commercial Code (UCC), as applicable.

The Parties hereby agree as follows:

This Agreement represents the entire agreement between the Parties in relation to the subject matter hereof and supersedes all prior agreements, understandings, or negotiations between the Parties, whether written or oral.

IN WITNESS WHEREOF, the Parties have executed this Agreement as of the date first above written.

______________________________

Lender's Signature

______________________________

Borrower's Signature

| Fact Name | Description |

|---|---|

| Governing Law | The Florida Loan Agreement form is governed by the laws of the State of Florida. |

| Usage | Used for documenting a loan transaction between two parties within Florida. |

| Requirements for Validity | Must include the signature of both the lender and the borrower to be legally binding. |

| Consideration of Usury Laws | Interest rates on loans must not exceed the limits set by Florida's usury laws to avoid penalties. |

Navigating through the Florida Loan Agreement form streamlines the process of documenting the terms of a loan between two parties. This systematic approach ensures all the prerequisites, terms, and conditions are clearly outlined, promoting transparency and mutual understanding. Once the form is completed, it serves as a binding document that outlines the responsibilities and expectations of both the lender and borrower. Filling out the form accurately is crucial for legal protection and clarity throughout the life of the loan.

Here's how to fill out the Florida Loan Agreement form:

After these steps are completed, the document should be reviewed carefully by both the lender and borrower to ensure that all the information is accurate and reflects their understanding. Once it is signed, it's advisable to make copies for both parties for their records. This form, when properly filled out, becomes a critical document for both parties, laying the foundation for a clear and enforceable loan agreement.

What is a Florida Loan Agreement form?

A Florida Loan Agreement form is a legally binding document between two parties, where one, known as the lender, agrees to loan money to the other, known as the borrower. The form spells out the specifics of the loan, including the amount lent, the interest rate, repayment schedule, and any other terms and conditions related to the loan. This agreement is crucial in Florida to ensure both parties understand their responsibilities and the details of the financial transaction.

Who needs to sign the Florida Loan Agreement form?

The Florida Loan Agreement form must be signed by both the lender and the borrower to be considered valid and enforceable. In some cases, if either party is a business entity, a representative authorized to enter into contracts on behalf of the business must sign the agreement. Additionally, having a witness or a notary public sign the form can add an extra layer of protection and verification to the agreement.

What should be included in a Florida Loan Agreement form?

These elements ensure the agreement is thorough and covers all necessary aspects of the loan, providing clarity and preventing disputes.

How is the Florida Loan Agreement form enforced?

In Florida, a Loan Agreement form is enforced through the legal system if disputes arise or if the borrower fails to meet their repayment obligations. Initially, the lender might try to work out a solution with the borrower. However, if these efforts fail, the lender has the right to take legal action, seeking to recover the owed amount through court proceedings. The agreement itself serves as the primary evidence of the terms agreed upon by both parties, and courts typically uphold these agreements as long as they were entered into freely and contain no illegal terms. It's essential for both lenders and borrowers to understand their rights and obligations under the agreement to avoid legal issues.

One common mistake people make when filling out the Florida Loan Agreement form is not double-checking the accuracy of the information entered. This includes misspelled names, incorrect addresses, or inaccurate loan amounts. Such errors can lead to delays or legal issues down the line, undermining the trust and legal standing of the agreement.

Another frequent oversight is failing to specify the interest rate clearly. This lack of clarity can cause misunderstandings about the financial obligations expected from the borrower. It's critical to articulate whether the interest rate is fixed or variable and to detail how it's calculated and applied to the principal amount.

Many fail to outline the repayment schedule in a comprehensive manner. The agreement should include specific dates for payments, the number of installments, and what happens in the event of a late payment. Without this detail, managing and enforcing the agreement can become challenging, potentially leading to disputes.

Ignoring the inclusion of a clause regarding late fees or penalties for missed payments is a mistake. This omission can leave the lender without recourse to enforce penalties, making it difficult to manage late payments effectively. Clearly defining these terms upfront can help maintain a healthy lending relationship.

Overlooking the necessity to detail the loan's purpose is another common error. Specifying how the loan should be used can prevent misuse of the funds, ensuring that the borrower applies the loan to its intended purpose, which is particularly important for business or mortgage loans where the funds are meant for specific uses.

Some individuals neglect to include a prepayment clause. This oversight can lead to confusion or disputes over whether the borrower can repay the loan early and if any penalties apply for doing so. A clear prepayment clause protects both parties' interests.

Not stating what constitutes a default under the agreement is a critical mistake. This should cover scenarios beyond just missing payments, such as bankruptcy or failure to maintain insurance. Clearly defining default conditions ensures that both parties understand the severity and consequences of such actions.

Failing to identify collateral, if any, secures the loan, can be a significant oversight. For secured loans, detailing the collateral and what happens if the loan is not repaid is pivotal for the lender's protection.

A common error is not having the loan agreement witnessed or notarized, depending on the legal requirements. This step lends authenticity to the document and can be crucial in the enforcement of the agreement.

Last but certainly not least, many forget to have all parties involved sign the agreement. This might seem obvious, but it's a surprisingly common oversight that can invalidate the entire document. Making sure that everyone's signatures are on the loan agreement is fundamental to its enforceability.

When entering into a loan agreement in Florida, it's important to understand that the loan agreement form is just one piece of the puzzle. There are several other documents and forms that are often used alongside it to complete the transaction, ensure legal compliance, and protect the interests of both the lender and the borrower. Each of these documents serves a specific purpose and is essential for different aspects of the loan process. Here's a list of 10 other forms and documents that are frequently used along with the Florida Loan Agreement form, providing a comprehensive approach to handling loan transactions smoothly and efficiently.

Navigating through a loan agreement in Florida and complementing it with the right forms and documents is crucial for a successful and legally sound transaction. Understanding the purpose and requirement of each document ensures that both lenders and borrowers are well-informed and protected throughout the lending process. Whether you're securing a small personal loan or a large commercial loan, being prepared with the correct documentation will pave the way for a smooth financial transaction.

The Florida Loan Agreement shares similarities with the Promissory Note, as both documents outline the terms under which money is loaned to a borrower by a lender. Like a Loan Agreement, a Promissory Note clearly details the loan's amount, repayment schedule, interest rate, and consequences of non-payment. However, the Promissory Note is often more straightforward and less detailed than a comprehensive Loan Agreement, serving as a formal IOU between the parties involved.

Much like the Loan Agreement, a Mortgage Agreement is a type of contract used in the process of buying real estate in Florida. While a Loan Agreement can apply to various types of loans, a Mortgage Agreement is specifically tied to loans for purchasing property. It secures the loan by using the purchased real estate as collateral. This document outlines the borrower's obligations, including making regular payments and maintaining insurance, similar to the repayment and maintenance terms found in Loan Agreements.

The Florida Personal Guarantee is another document that bears resemblance to the Loan Agreement, particularly when a loan involves considerable risk to the lender. This legal form acts as an addendum of sorts, where a third party agrees to take on the debt obligation if the original borrower fails to make payments. While a Loan Agreement specifies the terms between borrower and lender directly, a Personal Guarantee introduces another layer of security for the lender, guaranteeing that the loan will be repaid.

Debt Settlement Agreements also share common ground with Loan Agreements, in that they are used to re-negotiate or settle a borrower's outstanding debts. Both documents formalize the terms of financial transactions and obligations. However, a Debt Settlement Agreement comes into play after the borrower has had difficulties fulfilling the terms of the original Loan Agreement, offering a plan to pay off the debt under new terms agreed upon by both lender and borrower.

Lastly, a Florida Security Agreement correlates with a Loan Agreement in its function of detailing collateral that secures a loan. Like a Loan Agreement, it outlines specific conditions under which the loan must be repaid and what happens if the borrower defaults. However, the focus of a Security Agreement is on the assets pledged as security for the loan, ensuring the lender has a legal claim to the collateral if the borrower fails to meet the loan's obligations.

When filling out the Florida Loan Agreement form, it's important to approach the task with care and precision. Keeping the following dos and don'ts in mind can help ensure the agreement is both accurate and legally binding.

Do:

Don't:

Understanding the nuances of loan agreements is crucial, particularly in the state of Florida, where misconceptions can lead individuals to make ill-informed decisions. Below are seven common misunderstandings about the Florida Loan Agreement form, each dissected to clarify the actual stance and implications.

All loan agreements in Florida are the same: This is a common misconception. In reality, loan agreements can vary significantly in terms of interest rates, repayment terms, and collateral requirements. Each agreement is tailored to the specific circumstances of the borrower and lender.

Verbal agreements are legally binding: While verbal agreements can be legally binding, the complexity and significance of loan transactions make written agreements essential in Florida. A written contract helps to prevent misunderstandings and provides a clear record of the terms agreed upon by both parties.

You don't need a witness or notary: For a loan agreement to be enforceable in Florida, it doesn't necessarily need to be witnessed or notarized. However, having a notary or witnesses can add a layer of validity and protection, ensuring that the document reflects the true intention of the parties involved.

Loan agreements are only for large amounts of money: This is not true. Loan agreements can be used for transactions of any size. They are a smart option for any situation where one party is lending money to another, as they clearly outline the terms and conditions of the loan, regardless of the amount.

All loan agreements require collateral: While many loan agreements do involve collateral as a security measure for the lender, it is not a universal requirement. Unsecured loans, which do not require collateral, are also common, though they may come with higher interest rates due to the increased risk for the lender.

Interest rates are standard across all loans: In reality, interest rates can vary widely depending on the lender, the borrower's creditworthiness, the amount of the loan, and the terms of the agreement. Florida law requires that interest rates comply with state usury laws, but within those parameters, rates can be negotiated.

Only financial institutions can provide loans: Individuals often believe that only banks or other financial institutions can issue loans. However, private loans between individuals are entirely legal and common in Florida. These agreements still need to adhere to legal requirements and should be documented in a loan agreement form to ensure clarity and legal enforceability.

When dealing with the Florida Loan Agreement form, it's critical to understand the implications and requirements involved to ensure both parties are protected and the terms are clear. Below are key takeaways individuals should keep in mind:

Promissory Note New York - An agreement providing thorough details on loan issuance, including conditions for repayment, interest rates, and guidelines for default or early payoff.

Loan Agreement Template Texas - The document may be required to be witnessed or notarized depending on the jurisdiction and the nature of the loan.

Maryland Promissory Note Download - A Loan Agreement form is a written contract between a borrower and a lender outlining the terms and conditions of a loan.

Promissory Note Template Georgia - It outlines the responsibilities and rights of both the lender and the borrower, ensuring clarity in the financial arrangement.