Blank Deed of Trust Template

Blank Deed of Trust Template

In real estate transactions, especially when it comes to securing a mortgage, one critical document often comes into play: the Deed of Trust. This legal instrument, while not universally used across all states, functions as a pivotal agreement involving three parties — the borrower, the lender, and a neutral third-party trustee. Essentially, it grants the legal title of the property to the trustee, providing the lender with a layer of security for the loan. The Deed of Trust stipulates that the borrower, also known as the trustor, retains the equitable title and the right to use and enjoy the property, as long as the terms of the loan are met. Should the borrower fail to comply with these terms, primarily by falling behind on payments, the trustee has the authority to initiate foreclosure proceedings on behalf of the lender. This mechanism serves as a protection for the lender's investment, ensuring that they can recover the loan amount if the borrower defaults. Once the loan is fully repaid, the trustee releases the property's title back to the borrower, marking the end of the agreement. The nuances of this arrangement, such as the specific powers of the trustee and the process for handling defaults, can vary significantly between jurisdictions, making a thorough understanding of local laws essential for anyone involved in a real estate transaction using a Deed of Trust.

Deed of Trust Template

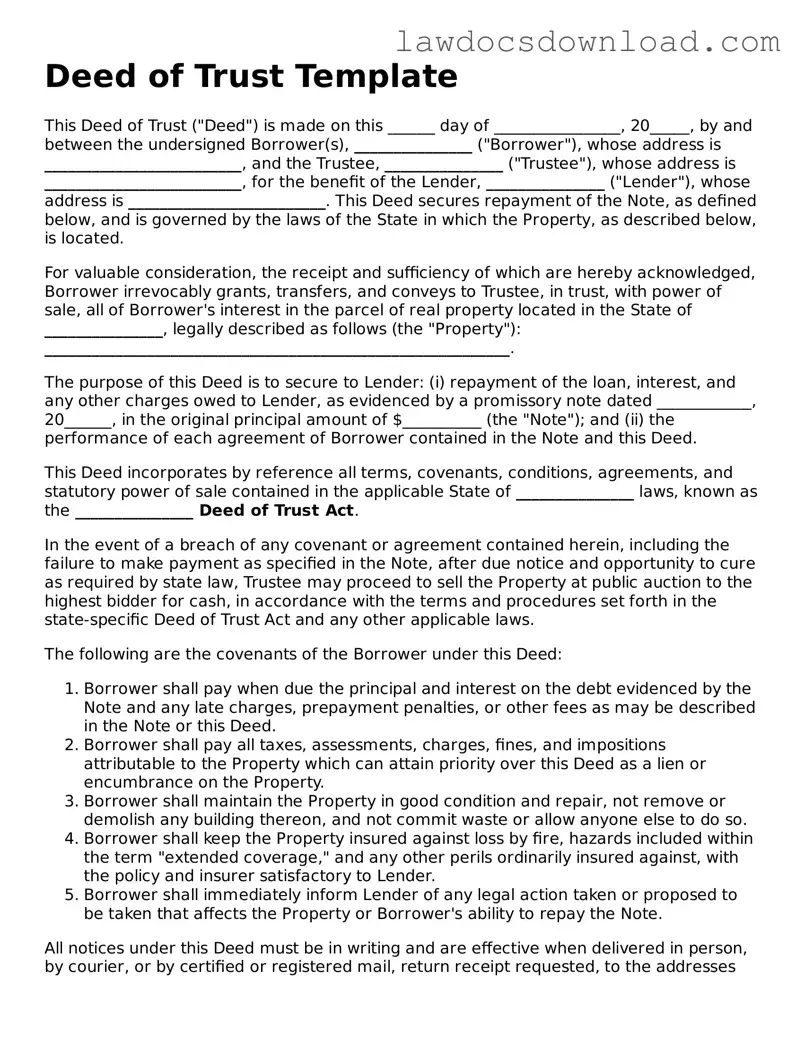

This Deed of Trust ("Deed") is made on this ______ day of ________________, 20_____, by and between the undersigned Borrower(s), _______________ ("Borrower"), whose address is _________________________, and the Trustee, _______________ ("Trustee"), whose address is _________________________, for the benefit of the Lender, _______________ ("Lender"), whose address is _________________________. This Deed secures repayment of the Note, as defined below, and is governed by the laws of the State in which the Property, as described below, is located.

For valuable consideration, the receipt and sufficiency of which are hereby acknowledged, Borrower irrevocably grants, transfers, and conveys to Trustee, in trust, with power of sale, all of Borrower's interest in the parcel of real property located in the State of _______________, legally described as follows (the "Property"): ___________________________________________________________.

The purpose of this Deed is to secure to Lender: (i) repayment of the loan, interest, and any other charges owed to Lender, as evidenced by a promissory note dated ____________, 20______, in the original principal amount of $__________ (the "Note"); and (ii) the performance of each agreement of Borrower contained in the Note and this Deed.

This Deed incorporates by reference all terms, covenants, conditions, agreements, and statutory power of sale contained in the applicable State of _______________ laws, known as the _______________ Deed of Trust Act.

In the event of a breach of any covenant or agreement contained herein, including the failure to make payment as specified in the Note, after due notice and opportunity to cure as required by state law, Trustee may proceed to sell the Property at public auction to the highest bidder for cash, in accordance with the terms and procedures set forth in the state-specific Deed of Trust Act and any other applicable laws.

The following are the covenants of the Borrower under this Deed:

All notices under this Deed must be in writing and are effective when delivered in person, by courier, or by certified or registered mail, return receipt requested, to the addresses specified above, or to such other addresses as any party may designate by notice to the other parties.

This Deed, together with the Note, represents the entire agreement between the parties concerning the subject matter hereof and supersedes all prior agreements, understandings, negotiations, and discussions, whether oral or written. This Deed may only be amended, modified, repealed, or waived by a written instrument signed by the parties hereto.

IN WITNESS WHEREOF, the parties hereto have executed this Deed of Trust as of the date first above written.

___________________________________

Borrower Signature

___________________________________

Trustee Signature

___________________________________

Lender Signature

| Fact Name | Description |

|---|---|

| Purpose | Secures a loan by using the property as collateral. |

| Parties Involved | Typically involves three parties: the borrower (trustor), the lender (beneficiary), and the trustee. |

| State-Specific Variations | Governing laws and requirements can vary significantly from state to state. |

| Recording | Must be filed and recorded with the local county recorder's office to be enforceable. |

When preparing to fill out a Deed of Trust form, it is essential that each step is followed accurately to ensure the document is legally binding and effectively records the agreement between the borrower and lender, using a trustee. This form establishes the borrower's property as security for the loan, a critical component in real estate transactions. Follow these guidelines meticulously to complete the form correctly.

Once the Deed of Trust form is fully completed and signed, it should be filed with the local county recorder's office. This step is critical as it makes the document a matter of public record, officially noting the lien on the property. This protects all parties involved and finalizes the trust deed process.

What is a Deed of Trust?

A Deed of Trust is a document that secures a real estate transaction involving a loan. Essentially, it involves three parties: the borrower (trustor), the lender (beneficiary), and a neutral third party (trustee) who holds the property title until the loan is paid off. This form ensures the lender's interest in the property is protected and outlines the terms under which the loan must be repaid.

How does a Deed of Trust differ from a Mortgage?

While both a Deed of Trust and a Mortgage serve to secure a loan on a property, they differ mainly in terms of the parties involved and the foreclosure process. A Mortgage involves just the borrower and the lender, and in case of default, the lender must go through the court to foreclose the property. On the other hand, a Deed of Trust includes a third party who holds the actual property title, and the foreclosure process can be faster since it may not require court intervention, depending on state laws.

Who can be a trustee in a Deed of Trust?

Typically, a trustee in a Deed of Trust is a neutral third party whose role is to hold the property title until the debt is paid off. This can be an individual or a company specializing in such roles, often involved in the real estate or escrow industry. The criterion is that the trustee must be impartial, able to efficiently manage the deed's directives, and recognized by state law as eligible to serve in this capacity.

What happens if the borrower defaults under a Deed of Trust?

Upon a borrower's default—the failure to meet the loan's terms as outlined in the Deed of Trust—the trustee has the authority to initiate the property's foreclosure. This process involves selling the property to repay the debt. The specific steps and procedures for foreclosure under a Deed of Trust can vary by state, but generally, it allows for a quicker and less costly process than foreclosure on a mortgage.

Can the parties involved modify a Deed of Trust?

Yes, modifications to a Deed of Trust are possible but require the agreement of all parties involved: the borrower, the lender, and the trustee. The modifications must be documented in writing and recorded with the same government entity where the original deed was filed. Common modifications include changes to the loan's terms, like the interest rate or the repayment schedule.

How is a Deed of Trust terminated?

A Deed of Trust is terminated when the loan is fully repaid. At this point, the trustee issues a Deed of Reconveyance, which transfers the property title back to the borrower, effectively releasing the lien on the property. This document should be recorded with the county clerk or similar local government authority to ensure the public record accurately reflects the property’s clear title.

Filling out a Deed of Trust form is a critical step in the home buying process, but it often comes with pitfalls that can lead to potential legal issues or delays. One common mistake is not verifying the legal description of the property. The legal description is more detailed than the address. It includes boundaries, measurements, and other specifics that uniquely identify the property. Errors or omissions in this section can invalidate the document or cause issues in the property's future conveyances.

Another area where people often err is in failing to list all the parties involved accurately. A Deed of Trust involves at least three parties: the borrower, the lender, and the trustee. Ensuring that the names, addresses, and relevant legal capacity (such as the correct business entity type for companies) of all parties are accurately reflected is crucial. Mistakes or inaccuracies can lead to disputes about who holds legal and financial responsibilities tied to the Deed of Trust.

Underestimating the importance of choosing the right trustee is another common error. The trustee holds the property title for the security benefit of the lender. Hence, it's vital to choose someone trustworthy and preferably with experience or understanding of real estate or legal processes related to property. Selecting a trustee without due diligence can complicate the situation if issues arise with the loan agreement.

A significant oversight often made by individuals is not understanding the terms of the loan that are outlined in the Deed of Trust. This document does more than just list the parties and describe the property; it also lays out loan amounts, interest rates, payment schedules, and what happens in the event of a default. Not fully understanding these terms can lead to surprises down the line, such as unexpected fees or actions taken by the lender.

Lastly, a critical mistake is neglecting to have the document notarized or failing to file it with the appropriate county or local government office. In many jurisdictions, for a Deed of Trust to be legally binding and enforceable, it must be notarized. Following notarization, it often must be recorded with the local government to establish the lien officially on the property. Failure to complete these steps can lead to the Deed of Trust being considered invalid, which puts the lender's security interest at risk and may complicate future sale or refinancing of the property.

When individuals are navigating the terrain of securing a mortgage for a home, a Deed of Trust is commonly used to outline the agreement between the borrower, lender, and trustee. This legal document is crucial for the process, but it's only one of several important pieces of paperwork involved. Alongside the Deed of Trust, several other forms and documents play pivotal roles in ensuring a smooth transaction and safeguarding the interests of all parties involved. Understanding these documents can help demystify the home-buying process and highlight the importance of each component.

Together, these documents form a comprehensive framework that supports the Deed of Trust, each with a unique function that promotes clarity, security, and fairness in the property buying process. They exemplify the careful structuring needed to navigate financial and legal commitments, designed to protect the involved parties and ensure that everyone is on the same page. Understanding these documents can provide individuals with a solid foundation for making informed decisions throughout the home-buying journey.

A Mortgage Agreement is closely related to a Deed of Trust, serving a similar purpose in the realm of real estate transactions. Both documents secure a loan on a property, providing the lender with a legal pathway to foreclose if the borrower fails to comply with the loan terms. However, a Mortgage Agreement involves just two parties—the borrower and the lender—while a Deed of Trust includes an additional party, a trustee, who holds the title for the benefit of the lender.

A Promissory Note walks alongside a Deed of Trust but focuses more on the borrower's promise to repay the loan under agreed terms. This document details the loan amount, interest rate, repayment schedule, and the consequences of default. It doesn't secure the loan with property like a Deed of Trust, but it serves as a foundational document that outlines the borrower's obligation to the lender.

A Land Contract mirrors a Deed of Trust by offering a form of financing for the buyer. Instead of borrowing from a traditional lender, the buyer makes payments directly to the seller until the full purchase price is paid. Unlike a Deed of Trust, the title remains with the seller until the final payment is made, at which point it's transferred to the buyer. This method can be advantageous for buyers who may not qualify for traditional financing options.

A Lease Agreement, while primarily used for rental arrangements rather than the buying and selling of property, shares the feature of laying out terms between two parties. It specifies the rights and duties of each party concerning the property, similar to how a Deed of Trust specifies the rights and responsibilities of the borrower, lender, and trustee. The key difference lies in the intent—leases don't typically lead to ownership, unlike the eventual transfer of property in a Deed of Trust arrangement.

A Quitclaim Deed also deals with transferring interests in property, often between known parties such as family members. Unlike a Deed of Trust, which secures a loan on the property, a Quitclaim Deed transfers ownership without any guarantee of clear title. It is simple and effective for transferring rights but does not involve the financial aspects of a Deed of Trust.

A Warranty Deed goes a step further than a Quitclaim Deed by not only transferring ownership but also guaranteeing that the seller holds clear title to the property. This similarity to the Deed of Trust lies in the emphasis on the legal status of the property—ensuring that rights are clear and unencumbered. However, it's chiefly about the transfer and guarantee of the title rather than securing a debt.

A Lien Release is somewhat the flipside of a Deed of Trust. While a Deed of Trust places a lien on the property to secure the loan, a Lien Release document removes this lien, typically after the loan has been paid off. Its connection to the Deed of Trust is through the lien: one document creates it, and the other removes it, marking the full circle of securing and then satisfying a debt with respect to property.

An Assignment of Rent is often used by lenders in commercial property loans, and it's akin to a Deed of Trust in that it involves security for a loan. In this arrangement, the borrower assigns their rights to the income from rents to the lender as additional security on the loan. Should the borrower default, the lender has the right to collect rents directly. This parallels the Deed of Trust's role in providing lenders with security, albeit through a different mechanism.

A Title Insurance Policy is an important companion to a Deed of Trust, intended to protect the lender (and often the buyer) from losses arising from disputes over the title after the transaction. It doesn't secure the property like a Deed of Trust but ensures that the title's history has been thoroughly checked for liens, disputes, or other issues. This reduces the risk to the lender and the borrower in property transactions.

A Construction Loan Agreement shares a basis with a Deed of Trust by providing a method of financing, focusing on the specific needs of building or renovating properties. Like a Deed of Trust, it secures the loan with the real estate in question. However, funds are typically disbursed in stages based on the progress of the construction, rather than in a lump sum. This specific form of financing underscores the adaptability of secured loans to various types of real estate transactions.

When filling out a Deed of Trust form, it's crucial to adhere to specific dos and don'ts to ensure the process is completed accurately and legally. Here’s a concise guide to help you through the process:

Do:Understanding the Deed of Trust form is crucial for anyone involved in purchasing or refinancing a home. However, several misconceptions can lead to confusion. Here are eight common misunderstandings and clarifications:

It's essential to have a clear understanding of the Deed of Trust and how it differs from other forms of real property security. Individuals looking into buying or refinancing their home should thoroughly research and consult legal advice specific to their situation to avoid these common pitfalls.

When dealing with a Deed of Trust, understanding the process and knowing what to expect can save time and prevent confusion. Below are five key takeaways for filling out and using a Deed of Trust form effectively.

Proper completion and understanding of the Deed of Trust are foundational to the security of the loan it secures and the rights and obligations of all parties involved. Taking the time to carefully address these key points can ensure a smoother, more reliable transaction.

Wuick Claim Deed - Typically, no money changes hands with a Quitclaim Deed, but it’s not a requirement.

California Correction Deed - A Corrective Deed is a failsafe, ensuring that minor oversights do not undermine major investments.