Blank Deed in Lieu of Foreclosure Template

Blank Deed in Lieu of Foreclosure Template

When facing financial difficulties, homeowners often seek various options to avoid the challenging process of foreclosure. Among these strategies, the Deed in Lieu of Foreclosure stands out as a dignified alternative that allows a borrower to transfer the ownership of their property back to the lender voluntarily. This process helps in circumventing the typical foreclosure route, potentially lessening the impact on the borrower's credit score and offering a semblance of control during a stressful period. The form that facilitates this transfer plays a critical role in ensuring both parties’ interests are adequately protected and the agreement is legally binding. It details the terms under which the property is transferred, including any conditions relating to the forgiveness of any deficiency balance that might remain after the property is sold. Understanding the nuances and legal implications encapsulated in this form is essential for both lenders and borrowers to make informed decisions and proceed with clarity and mutual respect.

Deed in Lieu of Foreclosure Template

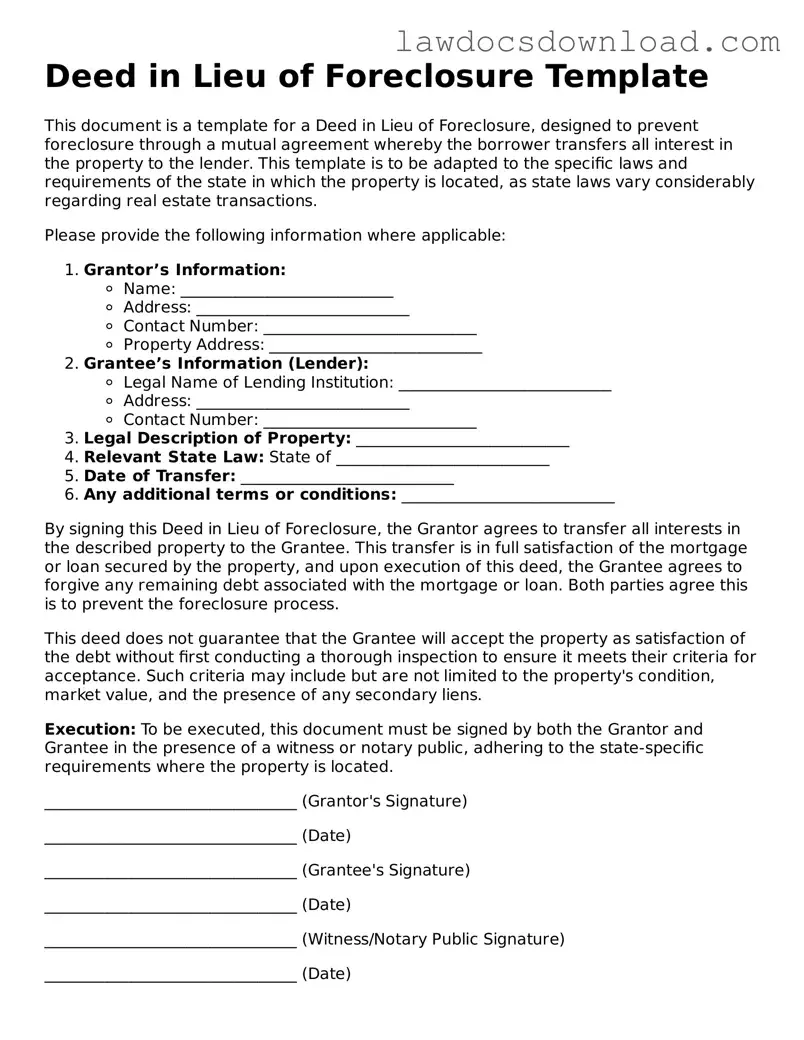

This document is a template for a Deed in Lieu of Foreclosure, designed to prevent foreclosure through a mutual agreement whereby the borrower transfers all interest in the property to the lender. This template is to be adapted to the specific laws and requirements of the state in which the property is located, as state laws vary considerably regarding real estate transactions.

Please provide the following information where applicable:

By signing this Deed in Lieu of Foreclosure, the Grantor agrees to transfer all interests in the described property to the Grantee. This transfer is in full satisfaction of the mortgage or loan secured by the property, and upon execution of this deed, the Grantee agrees to forgive any remaining debt associated with the mortgage or loan. Both parties agree this is to prevent the foreclosure process.

This deed does not guarantee that the Grantee will accept the property as satisfaction of the debt without first conducting a thorough inspection to ensure it meets their criteria for acceptance. Such criteria may include but are not limited to the property's condition, market value, and the presence of any secondary liens.

Execution: To be executed, this document must be signed by both the Grantor and Grantee in the presence of a witness or notary public, adhering to the state-specific requirements where the property is located.

________________________________ (Grantor's Signature)

________________________________ (Date)

________________________________ (Grantee's Signature)

________________________________ (Date)

________________________________ (Witness/Notary Public Signature)

________________________________ (Date)

This template is provided as a general guide. Individuals are strongly encouraged to consult with a qualified legal professional to ensure that all legal proceedings are conducted in accordance with local laws and regulations, and to address any specific circumstances or concerns.

| Fact | Description |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is a legal document by which a homeowner voluntarily transfers ownership of property to the lender to avoid foreclosure. |

| Voluntary Act | The process is initiated by the homeowner, making it a voluntary act to circumvent the negative consequences of foreclosure. |

| Financial Implications | Although it may relieve the borrower of the immediate debt, it does not always absolve all financial obligations that may arise from deficiencies or other related matters. |

| Credit Impact | The impact on the borrower's credit score can be significant but is generally less detrimental than that of a foreclosure. |

| State-Specific Laws | Variations in the process and the legal requirements exist from state to state, affecting how the deed in lieu is executed and processed. |

| IRS Considerations | The forgiveness of debt resulting from a deed in lieu may be considered taxable income by the IRS, though exceptions exist. |

| Mortgage Lender's Discretion | Acceptance of a deed in lieu of foreclosure is at the lender's discretion and may not be available in all cases or to all borrowers. |

| Prevention of Legal Claims | The agreement can include provisions that prevent the lender from later pursuing a deficiency judgment against the borrower for the difference between the sale price and the mortgage amount owed. |

Once the decision to proceed with a deed in lieu of foreclosure is made, accurately completing the necessary form is crucial. This document serves as a formal agreement between a borrower and a lender, where the borrower transfers the ownership of their property to the lender to satisfy a loan that is in default and avoid foreclosure. The process may seem daunting, but with careful attention to detail, it can be completed properly. Following are the steps required to fill out this essential form.

After the form is submitted, the document will be reviewed for completeness and compliance with local laws. Following approval, the deed in lieu of foreclosure will be recorded, officially transferring ownership of the property to the lender. This step marks the completion of the process, relieving the borrower from the mortgage debt associated with the transferred property and avoiding the more damaging impact of a foreclosure on their credit history.

What is a Deed in Lieu of Foreclosure form?

A Deed in Lieu of Foreclosure form is a legal document through which a homeowner can transfer ownership of their property voluntarily to the lender. This process is used as an alternative to foreclosure, where the lender can then sell the property to recover the loan balance. It's a mutual agreement that can benefit both parties by avoiding the lengthy and costly foreclosure process.

How does a Deed in Lieu of Foreclosure affect my credit?

While a Deed in Lieu of Foreclosure typically has a less negative impact on your credit score compared to a foreclosure, it still can significantly affect your credit history. It shows future creditors that you defaulted on your loan but took steps to mitigate the lender's loss. The impact varies based on individual credit history, but the notation will remain on your credit report for typically up to seven years.

What are the eligibility requirements for a Deed in Lieu of Foreclosure?

Can I cancel a Deed in Lieu of Foreclosure after signing it?

Once a Deed in Lieu of Foreclosure is signed and submitted, it is very challenging to cancel. The process involves voluntarily surrendering the property back to the lender, and after submission, the property title is transferred, effectively removing the homeowner's rights to the property. Before deciding on this course of action, it is crucial to fully understand your legal rights and possibly consult with a legal professional.

One common mistake individuals make when filling out the Deed in Lieu of Foreclosure forms is not thoroughly reviewing or understanding the terms and conditions. This oversight can lead to agreeing to unfavorable terms without realizing the long-term consequences, such as being held liable for the difference if the property sells for less than the balance on the mortgage.

Another issue is failing to accurately report all financial information. People sometimes either knowingly omit or unintentionally forget to disclose certain assets or liabilities. This can result in the bank rejecting the deed in lieu of foreclosure due to incomplete or misleading financial data. Transparency is crucial in these negotiations to ensure both parties are making informed decisions.

Incorrectly filling out the property details is also a frequent error. This includes mistakes such as wrong legal descriptions, parcel numbers, or incorrect addresses. Such inaccuracies can lead to significant delays in processing the form or may even nullify the agreement if the errors go unnoticed until after the process is assumed to be completed.

Neglecting to consult with a legal or financial advisor is a mistake that can have dire ramifications. Professionals can offer critical advice and insights that can prevent individuals from making uninformed decisions. They can help navigate the complexities of the agreement, ensuring that the rights of the individual are protected throughout the process.

Some individuals also fail to properly document and keep copies of all correspondence and documents related to the deed in lieu of foreclosure. This documentation can be critical if any disputes arise or if there are any questions about the agreement's terms after it has been processed.

Not negotiating the terms of the deed in lieu of foreclosure is another common oversight. Many do not realize they can negotiate terms such as relocation assistance, or the waiver of the deficiency balance. Accepting the first proposal without negotiation can leave individuals missing out on potential benefits.

Lastly, a significant mistake is waiting too long to initiate the deed in lieu of foreclosure process. This delay can limit the options available to the homeowner. Lenders may be less inclined to agree to a deed in lieu of foreclosure if the foreclosure process has already progressed too far, or if there are other liens against the property. Starting the conversation early can provide more latitude in negotiations and outcomes.

When homeowners face the possibility of foreclosure due to financial struggles, a Deed in Lieu of Foreclosure offers an alternative that allows them to transfer their property willingly to the lender. This agreement helps avoid the lengthy and stressful process of foreclosure, potentially preserving the homeowner's credit to some extent. Alongside the Deed in Lieu of Foreclosure form, there are several other documents and forms that are usually involved in the process to ensure that the agreement is comprehensive and all aspects of the property transfer are well-documented. Understanding these documents is crucial for both parties to ensure a clear and agreeable transaction.

Each of these documents plays a crucial role in the Deed in Lieu of Foreclosure process, providing clarity, legality, and fairness to the agreement. Both lenders and homeowners are advised to carefully prepare, review, and understand these forms and documents to ensure the transaction is conducted smoothly and without future disputes. Handling these complex situations with the proper paperwork can pave the way for a more positive outcome for all parties involved.

A deed in lieu of foreclosure form shares similarities with a mortgage agreement in that both documents involve agreements regarding property between a borrower and a lender. The mortgage agreement outlines the borrower's obligations to repay the borrowed funds used to purchase the property, establishing a lien on the property as security for the loan. In contrast, a deed in lieu of foreclosure acts as a resolution method when a borrower is unable to meet the mortgage obligations, allowing the transfer of the property's title to the lender to satisfy the debt, thereby avoiding foreclosure.

Another document resembling the deed in lieu of foreclosure form is the loan modification agreement. This document alters the original terms of the mortgage contract to provide borrowers with more manageable repayment terms. Like a deed in lieu, it serves as a foreclosure avoidance strategy, but rather than transferring property ownership to the lender, it adjusts the mortgage terms to prevent loan default and foreclosure.

The quitclaim deed also shows parallels to a deed in lieu of foreclosure form. A quitclaim deed transfers the owner's interest in property to another party without guaranteeing the title's status, which is similar to how a deed in lieu transfers property to satisfy a debt. However, the application contexts differ significantly; quitclaim deeds are often used between familiar parties, such as family members, rather than as a debt resolution strategy.

The short sale agreement is closely related to the deed in lieu of foreclosure form. In a short sale, the lender agrees to accept the proceeds from the sale of a property as full satisfaction of the debt, even if the sale price falls short of the outstanding mortgage balance. This agreement, like a deed in lieu, is a financial relief strategy for borrowers facing foreclosure, both aiming to mitigate the lender's loss and the borrower's financial strain.

The promissory note is another document with a connection to the deed in lieu of foreclosure form. A promissory note is a borrower's written promise to repay a specified sum of money to the lender at agreed-upon terms. While a promissory note outlines the obligation to pay the debt, a deed in lieu of foreclosure represents a method of settling that debt when repayment according to the original terms becomes untenable.

Finally, the warranty deed shares a resemblance with the deed in lieu of foreclosure form. A warranty deed transfers property ownership with guarantees from the seller that the title is clear of any claims or liens. While a deed in lieu of foreclosure involves a transfer of property to satisfy debt without such guarantees, both documents facilitate the conveyance of property titles under specific conditions.

In summary, while the deed in lieu of foreclosure form is distinct in its purpose and application, it shares functional and procedural similarities with a range of legal documents that involve property transfers, financial agreements, and foreclosure avoidance strategies. Each document plays a unique role in the broader context of property law and finance.

When faced with the decision to fill out a Deed in Lieu of Foreclosure form, it is critical to proceed with care. This document marks an agreement where a homeowner voluntarily transfers the ownership of their property to the lender to avoid foreclosure. The following guidelines aim to simplify the process, ensuring individuals are well-informed and able to navigate this complex situation with confidence.

Do:

Don't:

When homeowners face the distressing prospect of not being able to make their mortgage payments, they might consider a Deed in Lieu of Foreclosure (DIL) as an alternative. However, misconceptions about the process can lead to confusion and missed opportunities. Here are ten common myths about Deed in Lieu of Foreclosure, clarified to offer a better understanding.

Understanding the realities behind these misconceptions can help homeowners navigate the challenging path of potential foreclosure with a clearer perspective. Considering a Deed in Lieu of Foreclosure could offer a dignified exit from an untenable situation, but it's crucial to fully comprehend the ramifications and process involved.

Filling out and using the Deed in Lieu of Foreclosure form is an important process for homeowners facing foreclosure. It allows homeowners to transfer the ownership of their property to the lender to satisfy a loan that is in default and avoid foreclosure. Here are key takeaways to understand the process and its implications.

Wuick Claim Deed - Can be used to remove a name from a property title, such as after a marriage dissolution.

Lady Bird Johnson Deed - For those wanting to ensure their property avoids Medicaid estate recovery, a Lady Bird Deed can offer a potential solution.