Legal Connecticut Promissory Note Form

Legal Connecticut Promissory Note Form

In Connecticut, individuals and businesses often rely on a legal document known as a promissory note to formalize the terms under which money is borrowed and to be repaid. This document serves as a vital instrument in ensuring that the borrower agrees to pay back the lender, under specified conditions. It includes crucial details such as the amount borrowed, interest rate, repayment schedule, and consequences of non-payment. While it might seem straightforward, the Connecticut Promissory Note form is designed to protect all parties involved by clearly defining their rights and obligations. It provides a structured and enforceable framework for financial transactions, ranging from simple personal loans between family members to more complex lending agreements necessary for business operations. By having a well-drafted promissory note, lenders have a reliable means of legal recourse in case of default, whereas borrowers fully understand their repayment obligations, helping to prevent misunderstandings and potential legal disputes. This document is not only a cornerstone of private lending but also plays a significant role in the broader financial ecosystem within Connecticut, ensuring transparency and trust in personal and business financial affairs.

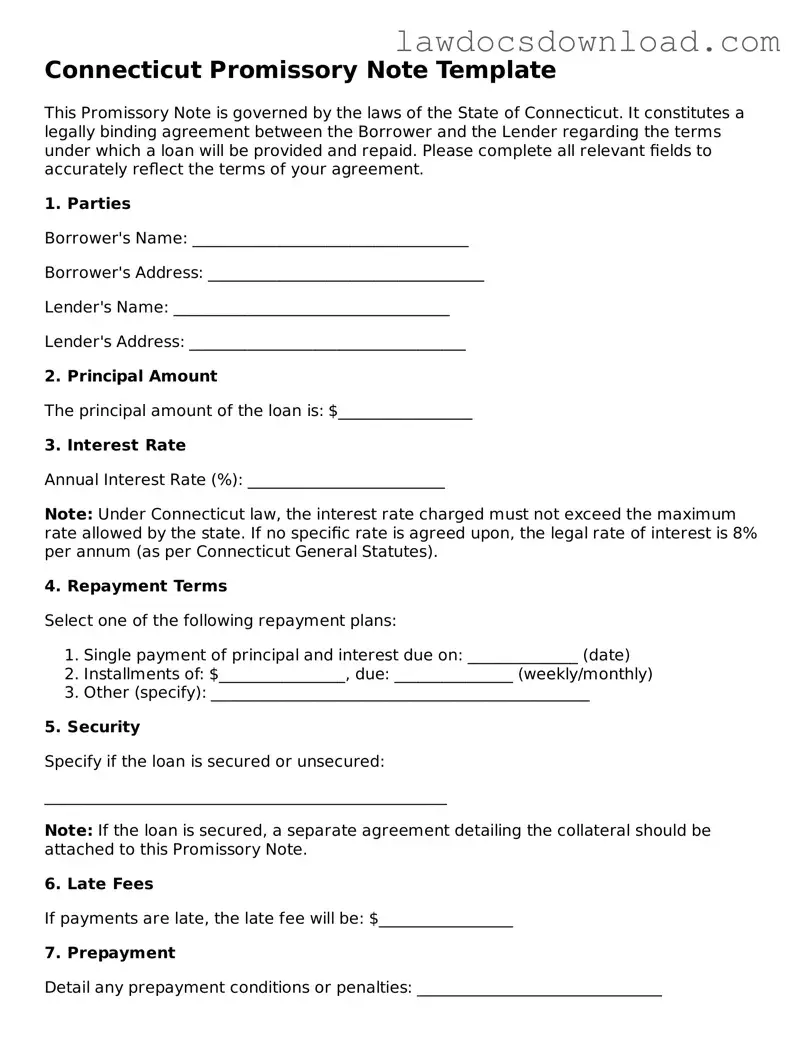

Connecticut Promissory Note Template

This Promissory Note is governed by the laws of the State of Connecticut. It constitutes a legally binding agreement between the Borrower and the Lender regarding the terms under which a loan will be provided and repaid. Please complete all relevant fields to accurately reflect the terms of your agreement.

1. Parties

Borrower's Name: ___________________________________

Borrower's Address: ___________________________________

Lender's Name: ___________________________________

Lender's Address: ___________________________________

2. Principal Amount

The principal amount of the loan is: $_________________

3. Interest Rate

Annual Interest Rate (%): _________________________

Note: Under Connecticut law, the interest rate charged must not exceed the maximum rate allowed by the state. If no specific rate is agreed upon, the legal rate of interest is 8% per annum (as per Connecticut General Statutes).

4. Repayment Terms

Select one of the following repayment plans:

5. Security

Specify if the loan is secured or unsecured:

___________________________________________________

Note: If the loan is secured, a separate agreement detailing the collateral should be attached to this Promissory Note.

6. Late Fees

If payments are late, the late fee will be: $_________________

7. Prepayment

Detail any prepayment conditions or penalties: _______________________________

___________________________________________________

8. Default

In the event of default, specify the actions that will be taken:

___________________________________________________

___________________________________________________

9. Governing Law

This Promissory Note will be governed by and construed in accordance with the laws of the State of Connecticut.

10. Signature

By signing below, the Borrower and Lender agree to the terms and conditions outlined in this Promissory Note.

Borrower's Signature: ___________________________________ Date: _____________

Lender's Signature: ___________________________________ Date: _____________

Witness (if any):

Name: ___________________________________

Signature: ___________________________________ Date: _____________

| Fact | Details |

|---|---|

| 1. Purpose | Connecticut Promissory Notes are used as a written promise to pay back a specified amount of money lent, with or without interest, by a specified date. |

| 2. Types | There are two main types: secured and unsecured. A secured promissory note requires collateral, while an unsecured note does not. |

| 3. Interest Rate | The maximum legal interest rate without an agreement in Connecticut is 12% per annum. With an agreement, the rate must not be usurious. |

| 4. Governing Law | Connecticut General Statutes govern promissory notes within the state, ensuring compliance with local lending practices and interest rates. |

| 5. Co-signer | Adding a co-signer is allowed to guarantee repayment. This is often used to strengthen the borrower's credibility. |

| 6. Payments | Repayment terms can be structured as interest-only, lump sum, due on demand, or in installments, depending on the agreement. |

| 7. Enforcement | In case of default, the holder may pursue legal action to collect the debt, as outlined in the promissory note and applicable state laws. |

| 8. Prepayment | Borrowers may be allowed to pay off the note early without incurring a penalty, depending on the specific terms of the note. |

| 9. Default Terms | Conditions of default should be explicitly stated, including the failure to make payments or breach of agreement terms. |

| 10. Amendment | Any modifications to the promissory note must be agreed upon in writing by all parties involved. |

Filling out the Connecticut Promissory Note form is a critical step for individuals who are entering into a loan agreement, either as a lender or a borrower, within the state of Connecticut. This document serves as a legal acknowledgment of the debt and outlines the terms for repayment, including the interest rate, payment schedule, and any collateral involved. The process requires attention to detail to ensure all parts are accurately completed to protect both parties involved in the transaction. Here are the steps to follow for filling out the form correctly.

Once the form is fully completed and signed, it's important for both the lender and the borrower to keep a copy for their records. This will help protect their interests and provide legal evidence of the loan agreement should any disputes arise in the future. Properly executing the Connecticut Promissory Note form is essential for ensuring that the loan process is conducted fairly and legally.

What is a Promissory Note?

A Promissory Note is a financial document that outlines a loan agreement between two parties—the lender and the borrower. It details the loan amount, interest rate, repayment schedule, and any other terms related to the borrowing and repayment of the loan. In Connecticut, like in other states, this document serves as a legally binding agreement ensuring the lender gets repaid under the agreed-upon conditions.

Who needs to sign the Connecticut Promissory Note?

Typically, the borrower and the lender must sign the Promissory Note. However, if a co-signer is part of the agreement, ensuring the loan's repayment, they must also sign. Some circumstances may require witness signatures or a notary public to officiate the document, enhancing its enforceability and credibility.

What are the types of Promissory Notes?

Two main types of Promissory Notes exist: secured and unsecured. A secured Promissory Note requires the borrower to pledge collateral against the loan. If the borrower fails to repay, the lender has the right to seize the collateral. An unsecured Promissory Note, on the other hand, does not require collateral, making it potentially riskier for the lender since recovery options for non-payment are limited.

Is a Connecticut Promissory Note legally binding?

Yes, in Connecticut, as in the rest of the United States, a properly executed Promissory Note is a legally binding document. This means that if the borrower fails to comply with the terms of the note, such as missing a payment, the lender has the legal right to pursue remedies, including taking the matter to court for enforcement and collection.

What information must be included in a Connecticut Promissory Note?

A Connecticut Promissory Note should include:

How can a lender enforce a Promissory Note in Connecticut?

If a borrower fails to meet the terms of the Promissory Note, the lender can take legal action to enforce repayment. This might involve filing a lawsuit against the borrower for the owed amount. For secured loans, enforcement can also include seizing and selling the collateral. Lenders are advised to adhere to Connecticut's legal procedures and guidelines for debt collection to ensure compliance.

Can a Connecticut Promissory Note be modified?

Yes, a Promissory Note can be modified, but any amendment must be agreed upon by all parties involved. This typically necessitates drafting an amendment to the original note or creating a new promissory note altogether. Any changes should be documented in writing and duly signed, following the same formalities as the original agreement.

What happens if the borrower pays off the Promissory Note early?

Early repayment terms should be addressed in the Promissory Note. Some notes may include a prepayment penalty, requiring the borrower to pay a fee for the privilege of early repayment. However, if no such terms are stated, or if the note explicitly allows for prepayment without penalty, the borrower can pay off the note early, thereby releasing any obligation under the terms of the note.

One common error when filling out the Connecticut Promissory Note form is neglecting to clearly identify both the borrower and the lender with their full legal names and addresses. This mistake can create confusion about the parties' identities, leading to potential enforcement issues. It is imperative that each party is accurately identified to uphold the note's legality and enforceability.

Another oversight is failing to specify the loan amount in clear, unambiguous figures and words. This precision is crucial to avoid disputes over the total amount borrowed. Insufficient clarity on the loan amount can undermine the entire agreement, making it difficult to enforce the terms set by the parties.

Often, individuals omit the interest rate, or if included, it might not comply with Connecticut's usury laws. This oversight not only leads to potential legal challenges but can also result in penalties or the voiding of the interest terms altogether. It's essential to verify that the interest rate is legal and clearly stated in the document.

The repayment schedule is another area frequently mishandled. Without a clear repayment plan, including due dates and the number of payments, misunderstandings and disagreements can arise. A detailed schedule helps both parties understand their obligations, reducing the risk of conflicts.

A crucial yet commonly neglected component is the inclusion of a clause regarding late fees and default consequences. Without these details, enforcing penalties or taking legal action in the event of non-payment becomes significantly more complicated. Clearly stating the repercussions of late or missed payments is essential for a comprehensive agreement.

Many fail to address co-signer responsibilities, assuming this note will not require one. However, including a co-signer clause, even if not immediately necessary, provides flexibility and security for the lender. It ensures another avenue for recourse should the primary borrower fail to meet their obligations.

An equally important misstep is not having the promissory note witnessed or notarized, despite it not being a strict requirement in Connecticut. This formality can lend credibility to the document and may assist in its enforcement. A witnessed or notarized document is harder to contest in court, providing added security to the involved parties.

Leaving out governing law information is another oversight. It is crucial to state that the note will be governed by the laws of Connecticut. This inclusion helps prevent legal uncertainties and clarifies which state's laws will adjudicate any disputes that might arise from the agreement.

Failure to include a severability clause is a common mistake. This clause ensures that if one part of the note is found to be invalid, the rest of the agreement remains enforceable. Such a provision helps preserve the intent of the agreement as much as possible, even if some aspects are contested.

Last but not least, individuals often neglect to keep a copy of the signed promissory note for their records. Maintaining a copy is vital for both parties as it serves as a proof of the agreement and the terms, which could be crucial in resolving any future disagreements or for tax and legal purposes.

When dealing with a Connecticut Promissory Note, several additional documents are frequently used to ensure a smooth financial transaction. These documents not only complement the promissory note but also offer legal protections and clarity for all parties involved. Understanding each document and its purpose can help in managing financial agreements more effectively.

Together, these documents form a comprehensive framework that ensures all aspects of the loan are clearly defined and understood. Handling financial agreements with the right documentation helps protect the interests of all parties involved and can make the difference between a smooth transaction and potential legal issues down the road.

A Loan Agreement, much like the Connecticut Promissory Note, outlines the terms and conditions of a loan between two parties. Both documents specify the loan amount, interest rate, repayment schedule, and the consequence of failure to repay. However, a Loan Agreement typically is more detailed and may include clauses on dispute resolution, confidentiality, and security agreements, offering comprehensive coverage of all aspects of the loan.

IOU Documents share similarities with the Connecticut Promissory Note, as they both acknowledge a debt owed. An IOU simply states the amount owed and the debtor, making it less formal and detailed. Unlike Promissory Notes, IOUs generally do not include specific repayment terms or interest rates, making them more suited for informal debts among friends or family.

Mortgage Agreements also mirror aspects of the Connecticut Promissory Note, particularly in their function of outlining the terms under which money is borrowed to purchase real estate. While both documents detail repayment terms, a Mortgage Agreement secures the loan against the purchased property, serving as collateral. This fundamental difference means that failure to repay the loan can result in foreclosure of the property under a Mortgage Agreement.

A Personal Guarantee is associated with the Connecticut Promissory Note through its assurance of debt repayment. In both, there's a promise to repay the borrowed amount. However, a Personal Guarantee is distinct because it involves a third party agreeing to repay the loan if the original borrower fails to do so, offering an additional layer of security to the lender.

Lines of Credit Agreements share a relation with the Connecticut Promissory Note in the promise to repay borrowed money. However, Lines of Credit Agreements offer more flexibility, allowing borrowers to withdraw funds up to a specified limit over a set period. In contrast, Promissory Notes typically involve a one-time loan and repayment plan without the ability to borrow more in the future.

Indenture Agreements, typically used in bond markets, bear resemblance to the Connecticut Promissory Note as they both involve a borrower agreeing to repay a lender according to specified terms. However, Indenture Agreements are more complex, involving multiple parties including a trustee who oversees the bond's administration and ensuring the issuer meets terms. This complexity supports larger, often corporate, borrowing scenarios.

Debentures are akin to the Connecticut Promissory Note in that they are both debt instruments. A Debenture indicates a medium to long-term debt with the promise to pay back the loan amount along with interest. Unlike Promissory Notes, Debentures are secured only by the reputation of the issuer and not by physical collateral, making them riskier.

Student Loan Agreements share common ground with the Connecticut Promissory Note, particularly in their function of detailing the terms under which a student borrows money for education. Both specify the loan amount, interest, and repayment schedule. However, Student Loan Agreements often include provisions specific to students, such as deferment options while in school and grace periods post-graduation, which are not typically found in standard Promissory Notes.

When filling out the Connecticut Promissory Note form, it is important to approach the task with careful attention to detail and a clear understanding of the obligations being entered into. The following list outlines key dos and don'ts to ensure that the promissory note is completed accurately and effectively:

When dealing with the Connecticut Promissory Note form, several misconceptions frequently arise. Understanding these misconceptions is vital in ensuring the proper use and interpretation of promissory notes in this state.

One does not need a witness or notarization. Many believe that for a promissory note to be valid in Connecticut, it doesn’t require a witness or notarization. However, having a witness or notarization can significantly strengthen the enforceability of the document, especially if disputes arise.

All promissory notes are the same. A common misconception is that all promissory notes are identical, regardless of their purpose or the involved parties. The truth is, the details and terms can vary significantly based on the loan amount, repayment schedule, interest rate, and other specific conditions agreed upon by the parties.

Verbal agreements are as binding as written ones. While oral contracts can be enforceable, a written promissory note is far more reliable and easier to enforce in court should any disputes about the loan arise.

Interest rates can be freely determined. Some believe that the parties can set any interest rate they agree on. Connecticut law, however, imposes limits on interest rates to protect borrowers from usury - the practice of charging excessively high interest.

Only the borrower needs to sign. It is a common misconception that only the borrower's signature is required on the promissory note. While the borrower's signature is certainly essential, having the lender sign the document can also be important, especially for clarifying the agreement's validity and the lender's commitment.

A promissory note is only a personal commitment. Some people mistakenly believe that a promissory note is merely a personal promise without legal standing. In reality, a promissory note is a legally binding agreement that obligates the borrower to repay the loan under the agreed-upon terms.

Clearing up these misconceptions is crucial for both lenders and borrowers to understand their rights and obligations fully when entering into a promissory note agreement in Connecticut.

When filling out and using the Connecticut Promissory Note form, there are key considerations to ensure clarity, enforceability, and compliance with state laws. It's critical to approach this document with precision and understanding. Here are some important takeaways:

Properly executed, a promissory note is a powerful legal document that outlines the borrower's promise to repay a loan under specific terms. Attention to detail and adherence to legal requirements are crucial in the drafting and execution process. This ensures that both parties are protected and the agreement stands up in a court of law, should disputes arise.

Georgia Promissory Note - Binds the borrower to a structured financial obligation, ensuring that the lender has a clear avenue for recourse.

Does Promissory Note Need to Be Notarized - It may outline the method of payment, such as through check, bank transfer, or cash, to ensure clarity and compliance.

Loan Note Template - A borrowed sum's repayment agreement, defining the amount, interest, and schedule for payments between a lender and borrower.

Promissory Note Template Utah - The promissory note's flexibility allows it to be tailored to various types of loans and repayment scenarios.